Micron bets $250 billion on US fabs. Why is the company securing future supply?

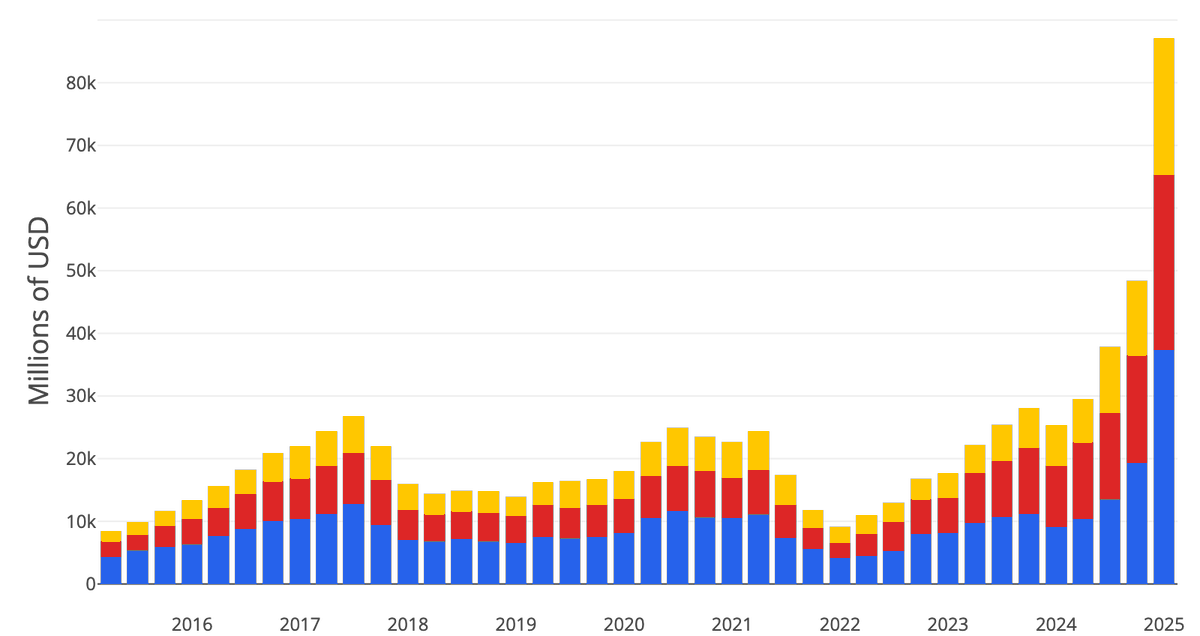

Micron yesterday announced it is raising its US investment plan to over $250 billion by 2035. That’s $50 billion more than it pledged last June. And that June pledge was itself $30 billion higher than originally planned.

In a year, the numbers have jumped by tens of billions three times in a row.

The stock reacted with a jump of over 7%, and year-to-date $MU is up more than 214%. The market simply believes. The question is whether it should.

Memory has a short memory

The memory business is one of the most cyclical in the entire tech sector. Whenever a period of euphoria arrives – be it the PC boom of the 90s, the dot-com fever around 2000, or the smartphone era after 2010 – DRAM and NAND manufacturers launch massive investments in new fabs. Capacity multiplies within a few years.

Then reality sets in, demand slows, but supply stays the same. Chip prices plunge by tens of percent and margins evaporate. Micron has lived through this repeatedly. In 2008 the company was losing money; in 2019 DRAM prices halved and profits vanished almost instantly.

The difference from past cycles is that this time the driver isn’t consumer electronics but data centers for artificial intelligence.

Micron wants to manufacture 40% of its DRAM in the US, and part of the plan includes a new fab in Clay, New York, where the company just poured its first concrete – a quarter ahead of schedule. On top of that, it’s adding $3 billion into the supply chain, of which half a billion goes to a Texas factory of GlobalWafers for silicon wafers, backed by a ten-year supply agreement.

What this means for the valuation

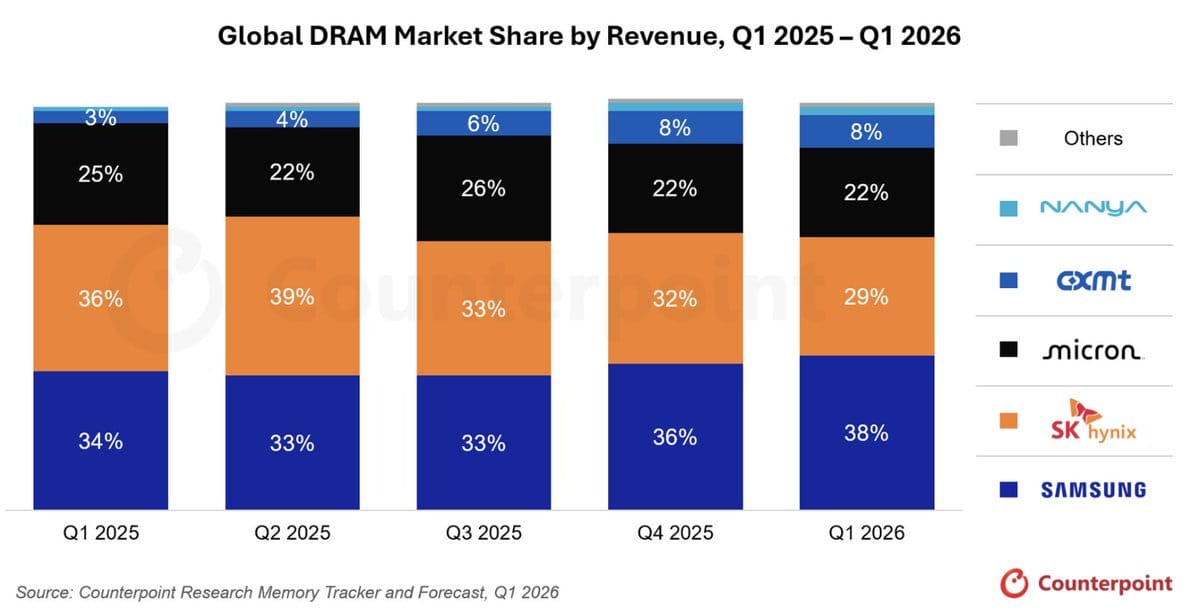

Micron is trading on the AI euphoria wave today, much like Nvidia $NVDA or Broadcom $AVGO. According to the company, customers already pre-booked $22 billion in memory deliveries last year. That’s an extremely strong number and shows that demand for HBM memory for AI accelerators is truly shattering records. Micron is one of the key suppliers to Nvidia, and without its chips, the new generations of AI servers simply couldn’t be built.

But investments worth a quarter of a trillion dollars spread out through 2035 mean enormous capital expenditures that will pressure free cash flow for years. The company is betting that demand for AI memory will grow faster than it can build new capacity. If that proves true, Micron could profit for a long time – high chip prices amid constrained supply are exactly what makes the memory business exceptionally profitable. But if the AI capex cycle cools before this capacity fully ramps up, the classic scenario awaits Micron: new production comes online just as demand is already fading, prices drop, and margins collapse just like in past cycles.

Moreover, the current valuation already embodies a lot of optimism. After a 200%+ surge in a year, the market isn’t pricing Micron as a cyclical commodity company but as a structural winner in AI infrastructure. That’s a big difference in expectations – and a big difference in risk if the reality turns out to be somewhere in between.

Investment thesis

I respect Micron because the company is doing exactly what it should – capitalizing on the historically strongest demand cycle in its industry and securing capacity and raw materials for it.

But I’m cautious about the multiples the stock is trading at today. The market is currently forgiving Micron’s cyclicality because the word “AI” works wonders for multiples across the entire sector. The question I ask myself is whether this growth can justify a valuation that already assumes Micron will never return to the old cyclical downturns. The history of the memory industry says it will; we just don’t know when.

For me, this is the kind of stock where I wouldn’t want to buy after a 7% surge on euphoric news. It makes more sense to wait for the moment when the market starts to doubt, because with cyclical companies, the best entries are always when sentiment is at its worst, not its best.