Trump Declares Ceasefire Dead and Markets Shake It Off | Weekend Intelligence #20

Three words at the NATO summit in Ankara were enough to send oil up five percent and the Dow down 577 points. Trump called the ceasefire with Iran “terminated,” ordered strikes on 90 targets, and in the same breath threatened to halt trade with Spain. A day later, markets reversed, chips rebounded, and SK Hynix raised $26.5 billion in the largest foreign listing in U.S. history at seven times oversubscription. Fed minutes meanwhile revealed a committee split nine to eight, a chair who refuses to give any hints, and a central bank that doesn’t know whether AI investments are an inflation threat or a productivity hope. Let’s look at what really matters.

Bulios Black: Weekend Intelligence is an exclusive analytical report published once a week and available only to Bulios Black members. If you want permanent access to this newsletter, to receive it automatically every weekend morning, and to read the full analytical section including specific scenarios and market implications, you need to become part of Bulios Black.

Fed Minutes: A Divided Committee, a New Chair, and the End of an Era

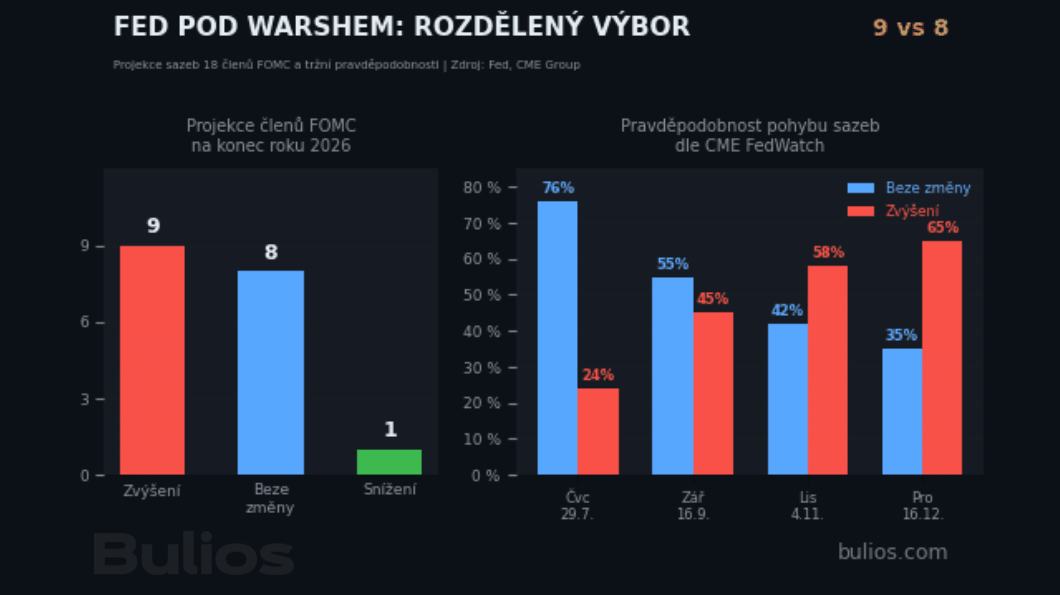

Wednesday’s release of the minutes from the June FOMC meeting, the first under the leadership of Kevin Warsh, confirmed what markets had suspected since June: the committee is split almost exactly down the middle and the chair chose to stay silent. Of the eighteen members who submitted dot-plot rate projections, nine expect at least one hike by the end of 2026. Eight expect no movement. One member expects a cut. Warsh himself became the first chair in history not to submit his own projection and announced the formation of a working group to overhaul the Fed’s entire communication framework, including the dot plot. The committee thereby lost its main navigation tool: an investor can no longer read the direction from the chair’s projection because none exists.

The minutes themselves ran 14 pages, slightly below the usual range, but the critical change was in tone. The statement contained just 130 words, roughly a third of the normal length. Most members explicitly supported shortening communication and removing language that in previous statements had hinted at a move toward easing. Phrases like “the committee is prepared to adjust rates if risks emerge” disappeared and were replaced by nothing. At the press conference after the meeting, Warsh used the sentence “the recent past may not be a template for the future,” which markets take as a signal that the Fed does not want to be bound by its own previous promises. The minutes confirmed this approach: several members noted that they “welcome the opportunity to review the committee’s communication tools and practices.”

Members addressed inflation with unusual frankness. The minutes state that “inflation will remain elevated in the near term and then begin to decline as the effects of tariffs, energy price increases, and other supply disruptions related to the closure of the Strait of Hormuz fade.” At the same time, however, members warned that “risks to the inflation outlook remain tilted to the upside.” The passage on artificial intelligence is interesting: the committee stated that “continued strong demand for AI infrastructure will likely keep pressure on prices of technology products and electricity.” Warsh himself, meanwhile, argued at the Sintra forum that AI will be disinflationary in the long run thanks to productivity gains. This tension between the short-term inflationary impact of AI investments and their long-term benefit is becoming one of the key analytical frameworks that the Fed has yet to resolve.

Markets reacted mildly to the minutes. Equity futures remained in the red, bond yields edged up, and gold fell to $4,075 per ounce. Jeffrey Roach of LPL Financial summed up the mood: “The minutes show considerable ambiguity, indicating several competing views on policy.” The CME FedWatch, after the release, prices the probability of holding rates at the July meeting at 76%, but by December the market assigns roughly a 40% chance of a hike into the 3.75 to 4.00% range. The key date is now July 14, when the June CPI will be released, the last major inflation number before the July FOMC meeting. If it confirms that the energy component of inflation is falling faster than the Fed expected, the hawkish wing of the committee will lose its main argument. If, on the other hand, core inflation stays above 3%, the scenario of a September hike moves from debate into the baseline assumption.

What This Means for Investors

Warsh’s Fed is a different kind of central bank than the one markets have grown used to over the past decade. Fewer words, no hints, no chair’s projection, and a committee split nine to eight. For investors, this means that every single macroeconomic data point, especially inflation and employment, will have a bigger impact on markets than at any time since 2022, because the Fed has stopped telling the market what it will do next.

USA: Dow Surpasses 53,000, but Wednesday’s Trump Bombshell Slams Markets Back

This week began with records. The Dow Jones on Monday broke through the 53,000 mark for the first time and closed at a new all-time high, the fifth thousand-point milestone this year. Defensive sectors, financials, and industrials pulled the index higher, while technology lagged. SpaceX on Monday officially entered the Nasdaq 100 and became the fastest addition to a major index after an IPO in history, just 15 trading days after its debut thanks to a new Nasdaq rule for mega-caps. But the stock fell nearly 7% in its first session as analysts initiated coverage with mixed ratings. Goldman Sachs set a neutral view, while critics noted that passive investors in QQQ now hold a company valued at over 90 times revenue with a loss of $4.28 billion for the first quarter.

Finish the whole article on ASML

And you also unlock fair value and more tools

Black membership: analyses, screener, newsletters and unlimited StockBot.