IBM has long been the backbone of the corporate world — a company that rarely makes headlines but quietly powers the financial, industrial, and public systems that keep economies running. After years of restructuring and spinning off legacy operations, Big Blue is finally showing that its transformation into a hybrid cloud and AI-driven business is gaining traction.

In the third quarter of 2025, IBM accelerated revenue growth, lifted margins across all divisions, and continued to deliver strong free cash flow. Once written off as a fading giant, it’s now re-emerging as a stable growth story rooted in software, data, and enterprise AI — proving that old tech can still teach the market new tricks.

How was the last quarter?

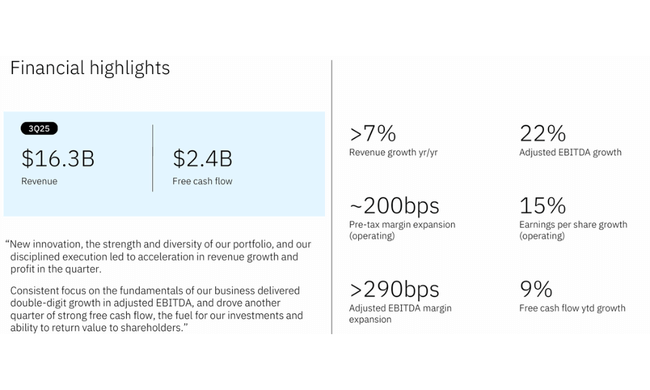

In the third quarter of 2025, IBM $IBM revenue was roughly $16.3 billion, representing 9% year-over-year growth and about 7% growth in constant currency. That's a very respectable pace for such a large, established company, especially with the combination of growth in all major segments. It's not a one-off blip - instead, it looks like the result of a systematic shift by the company towards the areas where the real value is today: software, hybrid cloud, data and AI.

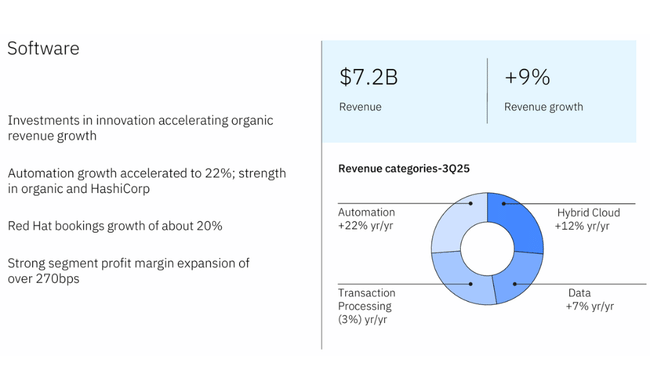

The biggest part of the business is Software with revenues around $7.2 billionwhich grew by 10 %. Hybrid cloud was the driver with Red Hat adding double-digit growth, but automation and data platforms were also very strong. A bit of a drag is traditional transaction processing, which is more mature and declining slightly, but overall the software segment is growing solidly. Consulting has increased revenues to around 5.3 billionwhich means a more modest 3% growthbut this is a segment that closely follows cloud and AI projects - IBM is building long-term relationships here and increasing the stickiness of its technology with large clients.

A pleasant surprise is Infrastructurewhere revenues jumped to $3.6 billionwhich is 17% year-over-year growth. This is mainly due to hybrid infrastructure, led by IBM Z - the new mainframe cycle has delivered more than 60% growth in this segment. For many old-timers, this is proof that "the mainframe is not dead yet" and still has a very specific and hard-to-replace role in the enterprise world. The finance part (IBM Financing) has also played a smaller but growing role and has boosted the overall results.

The margins show that it is not just volume growth, but also quality. Gross margin on a GAAP basis improved to 57,3 %, up more than a point on last year, and on an operating, non-GAAP basis, it climbed to 58,7 %. The operating picture is much more interesting: operating pre-tax margin rose to 18,6 %an improvement of two points.

GAAP net income was impacted by a one-time tax expense due to the new U.S. tax law H.R. 1, so the numbers themselves don't say much here. The bottom line is that at the operating (non-GAAP) level, IBM delivered some $2.5 billion in profits a earnings per share of about $2.65that's roughly 15% year-over-year growth. This aligns well with management's comment that the company achieved double-digit growth in "adjusted EBITDA" and improved profitability across segments.

Outlook

Management is so comfortable with the outlook for 2025 that has raised its full-year guidance. IBM now expects revenue to grow at constant currency by more than 5%with the current exchange rate environment expected to add about 1.5 percentage points of headwinds. That said, the company is playing an open game on a scenario where its growth settles steadily in the mid-single-digit range - a very respectable standard for a blue chip of this type.

Even more important than revenue growth itself for IBM is free cash flow. The company now expects to generate around $14 billion of free cash flowa marked improvement on previous years. In the first nine months of the year, it has already generated about $9.2 billion of operating cash flow a 7.2 billion of free cash flowso the plan doesn't look far-fetched. Strong cash generation is the foundation for two key things: funding investments in cloud and AI and maintaining an attractive dividend policy.

Long-term results

When we look at IBM's evolution over the past four years, we see a company in a long transformation curve. Revenue have gradually shifted from roughly 57.4 billion in 2021 to 62.7 billion in 2024. It's not a dramatic jump, but it is a steady transition from a company that has been stagnant or slightly declining for years to one that can maintain growth in at least the lower single digits. More important than the size of the revenue itself is its structure - today it is heavily dominated by software and consulting related to cloud and AI, whereas before there was a larger share of hardware and low-margin activities.

The improvement at the level of gross profit. This has improved from 31.5 billion in 2021 gradually increased to 35.6 billion in 2024growing faster than revenue. That said, IBM is succeeding in shifting the mix towards more value - more software, more data platforms and more services, where margins have traditionally been significantly higher than infrastructure. At the same time, the cost of sales is falling slightly, which is supporting overall margins.

The story is more complicated for operating costs. In 2022 and 2023, operating costs were virtually flat at gross profit level - the numbers suggest a high proportion of restructuring and one-off items, leading to a zero operating result on the books. Only in 2024 did the picture stabilise: operating expenses had fallen to around 29.5 billion dollarswhich allowed the return of operating profit to 6 billion.

At the level of net profit ...there is significant volatility, mainly due to tax and pension items. In 2021, IBM earned approximately 5.7 billion dollarsand a year later, net income had fallen to 1.6 billion due to one-time costs. 2023 then brought optically exceptionally high profits of around $7.5 billiondriven by tax effects, among other things, and 2024 dropped again to 6 billion. At first glance, this looks choppy, but after adjusting for large one-off items, it is clear that the operating business is rather gradually stabilising and generating solid, predictable profits.

News

IBM has added some important accents to its story in recent months, particularly around AI and the cloud:

- AI business already exceeds the value 9.5 billion dollars, making it clear that this is not a marketing label, but a real, significant source of growth.

- In the segment Software hybrid cloud with Red Hat is thriving, as well as new automation and data platforms that are directly linked to the use of AI in practice.

- Infrastructure is benefiting from the new IBM Z cycle and hybrid infrastructure, which remains the backbone of IT in many critical industries - from banking to government.

- The company has refined and improved full-year outlook on revenue and free cash flow, suggesting that the acceleration seen in the third quarter is not a fluke, but a trend.

- At the same time, IBM continues its long tradition of of regular dividendsby approving another quarterly payout of $1.68 per share.

Shareholder Structure

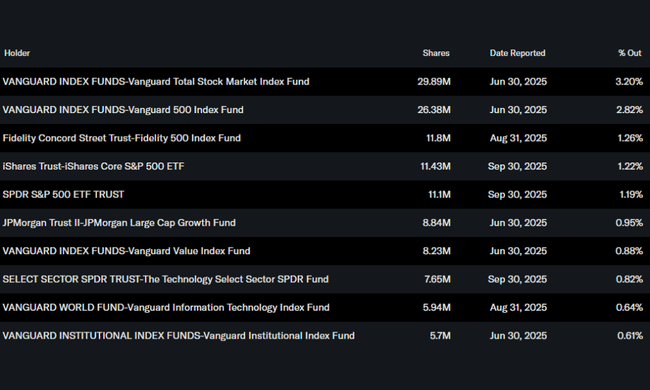

IBM's ownership structure matches the profile of a large, established blue chip. Insiders hold only about 0.1% of the sharesso that they have a decisive say institutional investors with a stake of roughly 64% of the company and the free float. This makes IBM a typical title for large funds and pension managers looking for a combination of stability, dividends and moderate growth.

Traditionally, the largest shareholders have included funds of the group Vanguard. Their Total Stock Market Index Fund holds approximately 3.2% of the stock, while the 500 Index Fund has nearly 2,8 %. It also has a strong position in Fidelity 500 Index Fund a iShares Core S&P 500 ETF. In practice, this means that IBM is closely tied to the performance of the major indices and sentiment toward the entire segment of large U.S. technology and industrial companies.

Analyst expectations

Analysts see IBM's current a combination of a defensive dividend title and a gradually emerging AI player. On one side are stable earnings, robust cash flow and a long-term conservative financial policy that supports an attractive dividend. On the other hand, there is room for above-average growth in selected parts of the portfolio - particularly in software, hybrid cloud and AI solutions for the enterprise sector.

The key questions for the next few years are primarily threefold: whether IBM can sustain sustained revenue growth above five percent, how fast AI projects will grow, and how much it can continue to improve operating margins without reverting to large one-time costs. If the company confirms that the current acceleration is not just a short-term cycle around mainframes and new products, but a long-term trend, IBM may move closer to being perceived as stable dividend title with a bonus "call option" on AI. And that is a combination that is very appealing to long-term investors.