Ford’s latest results show that even century-old automakers can still surprise the market. The company posted the highest quarterly revenue in its history, proving that its core strength — a balanced mix of combustion and commercial vehicles — remains resilient. Yet behind the record numbers lies a more complicated reality: the costly transformation toward electric mobility and software-driven manufacturing.

As tariffs, logistics constraints, and rising costs weigh on the industry, Ford $F finds itself financing its EV ambitions through the profits of its traditional business. The transition won’t be easy, but leadership argues it’s essential to building a leaner, more technology-focused company. For investors, Ford is no longer just a carmaker — it’s becoming a test case for how legacy industries reinvent themselves in the digital age.

How was the last quarter?

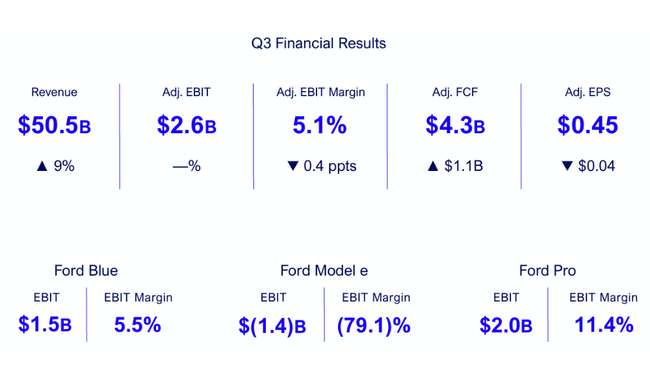

Ford presented results that show its traditional business engine is running at full speed, while the transformation toward electric vehicles remains a costly but necessary journey. The company reported sales of $50.5 billion, up 9% year-over-year. Despite continued pressure from tariffs and higher production costs, Ford was able to maintain a steady operating profit. Net profit was $2.4 billion, while adjusted EBIT was $2.6 billion - both figures already including the negative impact of tariffs of approximately $700 million.

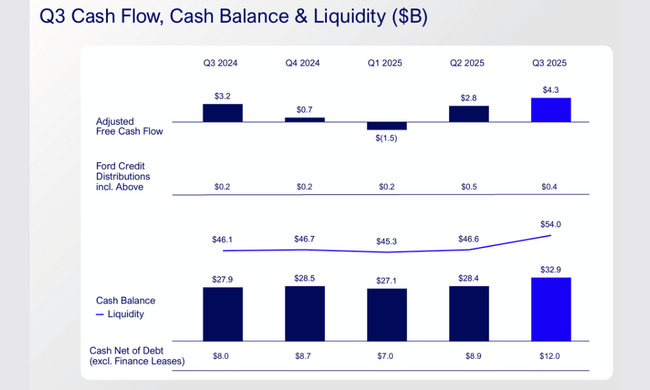

Operating margin narrowed slightly to 5.1%, down four-tenths of a percentage point from the previous year. At the earnings per share level, Ford earned $0.60, with adjusted earnings per share of $0.45. Strong cash flow was a major positive, with operating cash flow of $7.4 billion and free cash flow of $4.3 billion. The company has approximately $33 billion in cash on hand and total liquidity approaching $54 billion, providing ample room for investments, dividends and covering unexpected fluctuations.

The performance of each division reveals the typical contrast between traditional business and new projects. Ford Pro, focused on corporate and fleet customers, remained a key driver. Revenues grew 11% to $17.4 billion and EBIT was $2 billion with a margin of 11.4%. The segment is also expanding its software business, with the number of paid Ford Pro subscriptions up 8% to 818,000, indicating a growing emphasis on higher-margin services.

Ford Blue's Classic division generated $28 billion in revenue and earned $1.5 billion in EBIT, equivalent to a margin of 5.5%. While revenue growth outpaced volume growth, higher inputs and price competition limited margin expansion. In contrast, Ford Model e, the electric vehicle division, remains loss-making. Sales jumped 52% to $1.8 billion, but EBIT remained deep in the red - a loss of $1.4 billion with a margin of nearly -80%. Still, this is progress - a year ago the loss was relatively deeper.

Ford Credit continues to perform a stabilizing function - it earned $631 million pre-tax, up 16% year-over-year. Overall, Ford ended the quarter in solid shape, though the pressure from tariffs and the shift to electric mobility is clearly reflected in the cost structure.

CEO comment

Company boss Jim Farley described the quarter as a testament to the resilience of the traditional business and Ford's ability to respond to market changes. He highlighted that sales exceeded the $50 billion mark, mainly due to the strong performance of Ford Pro and a quality product portfolio. Farley said the company is moving into a new phase - it wants to be faster, more agile and more capital efficient. Getting the timing of investments in next-generation powertrains, partnerships and technology innovation right remains a key direction.

CFO Sherry House added that after adjusting for the impact of tariffs, year-on-year operating profit would even increase. She noted that the goal is to build a higher growth, higher margin and better capital utilisation business over the long term. Ford's transformation, she said, would be based on a combination of great products, software services and a strong brand that bridges traditional and new mobility segments.

Outlook

Ford confirmed that its core business is at the high end of this year's outlook, despite absorbing significant pressure from tariffs and exceptional costs related to the Novelis aluminium plant outage. For the full year 2025, the company expects adjusted EBIT in the range of $6.0 billion to $6.5 billion and free cash flow between $2 billion and $3 billion. Capital expenditures are expected to be approximately 9 billion.

Management believes the Novelis plant fire will be approximately a $1.5 billion to $2.2 billion negative impact on EBIT and $2 billion to $3 billion negative impact on cash flow, primarily in the fourth quarter. However, management also said that it already sees a way to mitigate the impact by at least 1 billion in 2026 through replacement suppliers and restarting some production.

Overall, Ford plans to continue improving efficiency, expanding its electrified model offerings and developing software platforms. The goal is for the Model e to gradually move from the investment phase to the monetization phase and for Ford Pro to become a key source of stable cash flow and margins.

Long-term results

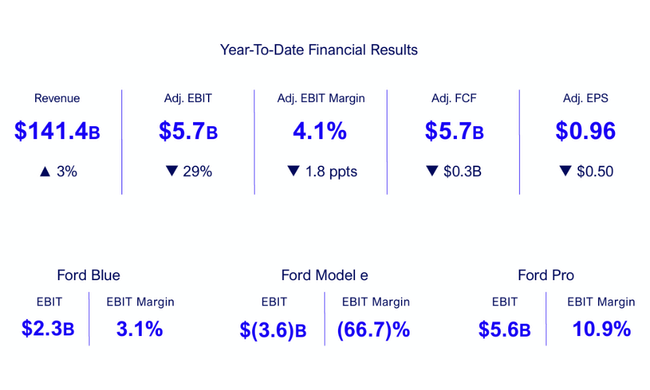

In the long term, Ford shows that the core business has stabilized and sales are gradually increasing. It reached a record $185 billion in 2024, up 5% from the year before. Meanwhile, gross profit jumped more than 64% to 26.6 billion, confirming that the company has managed to improve its product mix and better manage costs after a challenging period of post-covet inflation and intermittent supply.

Operating costs, however, rose significantly, almost doubling to 21.3 billion. This is related to rising spending on research, EV development, software and restructuring. As a result, operating profit fell slightly to $5.2 billion. Still, net profit for 2024 came in at 5.9 billion, up 35% year-on-year, and the company continued its return to profit mode after a loss-making 2022.

Earnings per share were $1.48, while EBITDA topped $14 billion, showing the ability to generate cash despite high capital expenditures. Thus, Ford remains financially stable, with a relatively strong balance sheet and ample room for continued investment in transformation.

News

- The company confirmed the payment of a quarterly dividend of 15 cents per share, payable on December 1.

- Ford Pro continues to expand software - commercial subscriptions grew to 818k accounts.

- Model e launched new electric vehicles for the European market to support volume growth in 2026.

- Ford continues to work on restoring production at aluminum supplier Novelis following a fire at the Oswego plant.

- The company highlighted continued investment in AI, predictive maintenance and fleet digitisation.

Shareholding structure

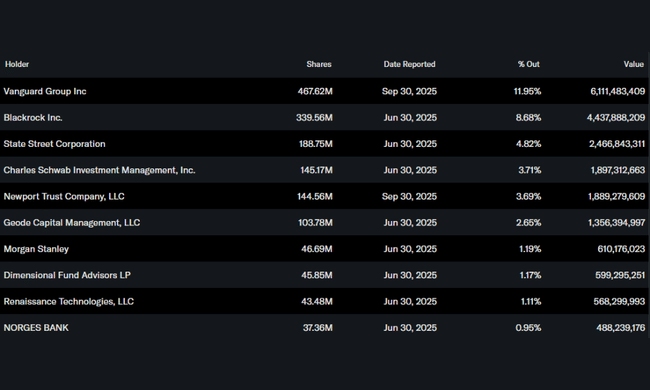

Ford remains a strongly institutionally owned company. Insiders hold just 0.29% of the shares, while institutional investors control nearly two-thirds of the total capital. Vanguard Group is the largest shareholder with nearly 12%, followed by BlackRock (8.7%), State Street (4.8%) and Charles Schwab (3.7%).

This structure provides high stability, but also pressure for a consistent dividend policy, disciplined management and a clear strategic direction in electrification and software. Ford thus remains under the scrutiny of long-term funds, which are particularly looking at return on investment and the company's ability to monetise the transition to new technologies.

Analysts' expectations

Analysts expect Ford to close 2025 near the high end of their projections, with adjusted EBIT of around $6.5 billion. For 2026, the market is pricing in a return to higher margins due to the unwinding of extraordinary effects and higher volumes for electric models. Net income estimates are around $5.5 billion to $6 billion and the dividend yield is expected to remain above 5%.

Key drivers for next year will be the ability to maintain margins in an environment of rate pressures, the speed of recovery from the Novelis issues, and the pace of Model e's transition toward profitability. The market rates Ford as a stable title with defensive qualities and incremental growth potential - if it can turn EV investments into a profitable reality.