Verizon entered the third quarter of 2025 with a singular mission: break out of years of sluggish growth and reposition itself as a true competitor in a rapidly evolving telecom landscape. Under the early leadership of CEO Dan Schulman, the shift is already visible — from customer experience and pricing strategy to operational discipline. Management describes the moment as a “critical inflection point,” one that demands a reset of how Verizon serves, competes, and expands.

The Q3 2025 results offer the first concrete glimpse of that transition. Key business segments are regaining momentum, profitability is improving, and service performance is showing signs of renewed strength. While parts of the portfolio still lag and the pressure from T-Mobile and AT&T remains intense, Verizon is entering the strongest financial footing it has seen in recent quarters. For investors, 2025 is clearly becoming both a rebuilding year and the opening chapter of an ambitious strategic reboot.

How was the last quarter?

The third quarter delivered solid, well-balanced performance across the business. Total revenue rose to $33.8 billion, holding to 1.5% year-over-year growth, which, while not a dramatic shift, shows stabilization after previous weaker years. More fundamental, however, is the growth in profitability - net income jumped to $5.1 billion compared to $3.4 billion last year and EPS increased to $1.17. Operating performance was also stronger, translating into adjusted EBITDA of $12.8 billion.

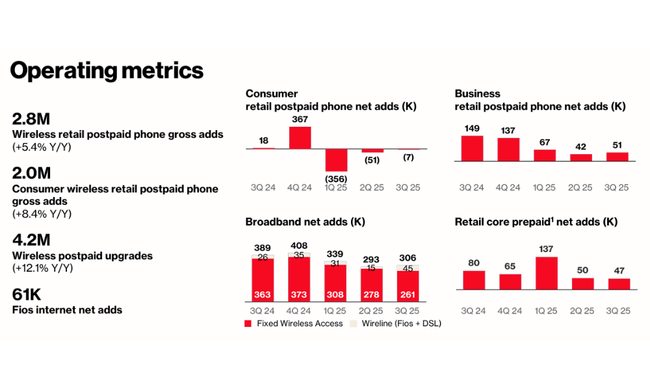

The most important metric is traditionally the wireless segment. Wireless service revenue was $21 billion and grew 2.1% year-over-year, a pace above the competition and also above internal expectations. This was compounded by solid equipment growth (5.2%) and rapid growth in the broader customer base. Verizon $VZ was able to add 306k new broadband users and the fixed wireless access area, with 261k additions, still looks like a strategic move that is starting to deliver dimensional benefits to the company.

The Consumer segment reported revenue growth of 2.9% and a very strong ARPA that exceeded $147. The Business segment is stagnant but still delivered higher operating profit due to better margins and lower acquisition cost burden. Overall, Verizon confirms that the operating side of the business has solid fundamentals and can grow even in a slower telecom cycle.

CEO comment

Dan Schulman laid out a clear trajectory in announcing the results: Verizon is facing a transformation that will not be a cosmetic adjustment, but a fundamental realignment of its entire structure. The new leadership is building on a customer-centric culture and plans to radically simplify the organization, digitally modernize processes and significantly reduce costs. Schulman stressed that the company must first regain its position as a leader and only then build space for further expansion. The key is to restore growth in core services, strengthen customer loyalty and optimise costs in detail across the company.

His tone is direct and ambitious: he says Verizon is at a point where decisive action must be taken without compromise. By all accounts, this marks the beginning of an era in which the telecom giant will once again seek the speed, aggressiveness and innovation that have waned in recent years. The first signs of change are already visible this quarter - and more will follow.

Outlook

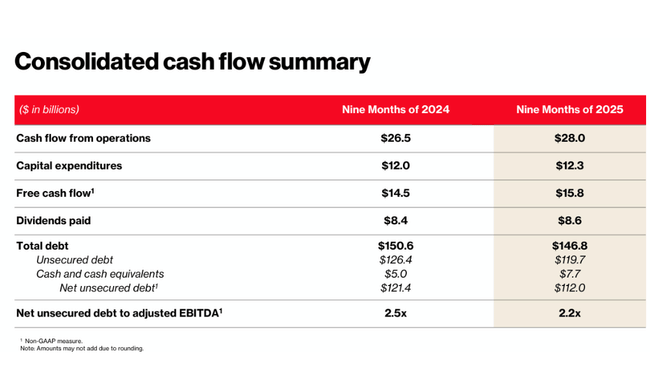

Management confirmed the full-year outlook is unchanged, which the market sees as a signal of confidence in the coming quarters. Verizon expects wireless service revenue growth in the range of 2.0-2.8%, adjusted EBITDA growth of 2.5-3.5%, and adjusted EPS growth of 1-3%. At the same time, robust cash flow generation is a key element of 2025 - operating cash flow is expected to be between $37-39 billion and free cash flow between $19.5-20.5 billion. The company also confirmed an investment plan to help turn improved margins into real growth.

Long-term results

Verizon's long-term performance shows both the resilience and some cyclicality of the telecom industry. Revenues remain stable at around USD134-136 billion per year, with 2024 delivering only modest growth of 0.6%. The more fundamental story, however, is at the profitability level. Gross profit is steadily increasing, but the operating part is crucial, where the company increased operating income by more than 25% in 2024 despite modest revenue growth, offsetting previous weaker years.

Net income is up more than 50% to US$17.5 billion in 2024, mainly due to cost stabilisation and robust wireless performance. EBITDA has been in the US$40-50 billion range for a long time, showing the structural strength of the company to generate cash even in a period of increased investment. As a result, Verizon enters 2026 with healthy operating cash flow, a strong market position, and an improved ability to fund transformation.

News

- CEO Schulman launches major transformation aimed at improving customer experience and reducing costs.

- Broadband segment, including FWA, saw record growth, surpassing 13.2 million users for the first time.

- Fixed wireless services are growing rapidly, approaching 5.4 million active users.

- Verizon continues to reduce debt, which fell from $126.4 billion to $119.7 billion year-over-year.

- The company confirmed capital expenditures in the range of USD 17.5-18.5 billion and continues to optimize its investment cycle.

Shareholder structure

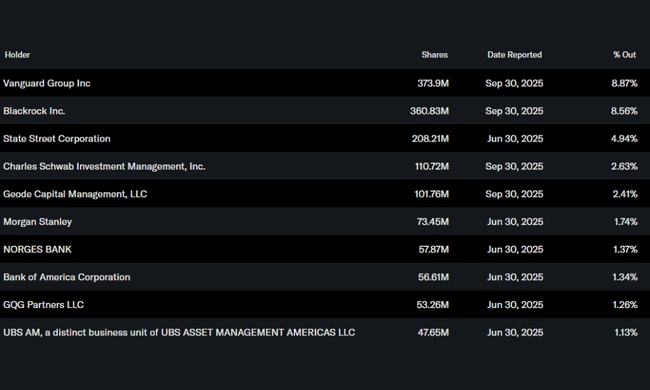

Verizon's ownership structure is typical of a large telecom operator with extensive institutional presence. Insiders hold only about 0.04% of the stock, while institutions control 68.6% of the free float. This creates a stable demand base and supports the stock's low volatility. The largest investors include Vanguard Group with 8.9%, followed by BlackRock with 8.6% and State Street with nearly 5%. These large funds act as long-term price stabilizers and confirm the market's high confidence in Verizon's future strategy.