The third quarter marked a turning point for CVS Health. After years of trying to build a sprawling healthcare empire spanning insurance, retail pharmacies and primary care, the company is pulling back to focus on what it has historically executed best: creating a unified, patient-oriented ecosystem that links pharmacy services with broader care delivery. Following several turbulent quarters defined by restructuring pressure and margin erosion, leadership is now emphasizing stability and disciplined prioritization across its core segments.

A key part of that reset is the company’s frank reassessment of its acquisition history. Several deals that once looked transformative have now resulted in a substantial goodwill impairment, underscoring the mismatch between past ambitions and today’s market reality. While the charge is non-cash, it signals a strategic recalibration: CVS is simplifying its structure, improving transparency and tightening financial oversight. Q3 2025 is the first quarter that shows early signs of this shift beginning to take hold.

How was the last quarter?

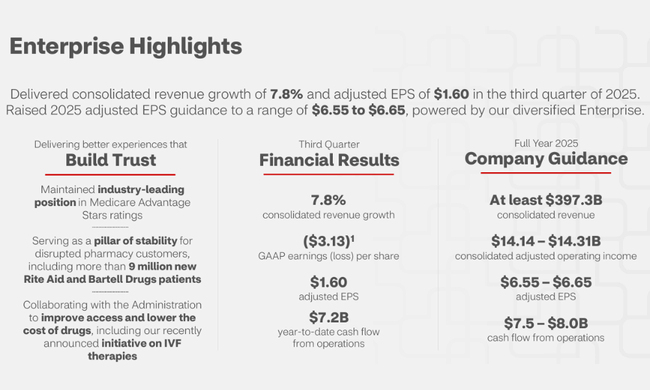

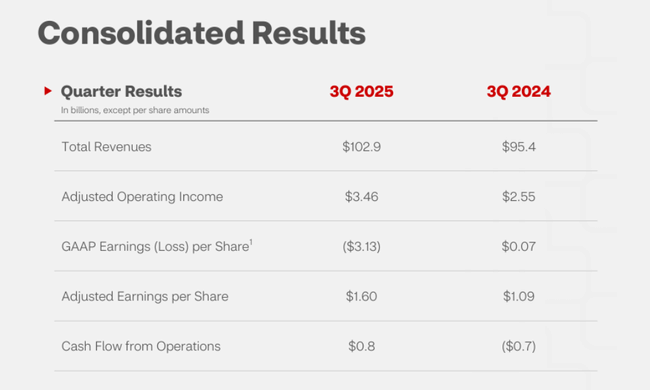

Q3 brought a mixture of two strong but contrasting stories. On an operational level, the company saw very solid revenue growth, which was reflected across all segments. Pharmacy services, health insurance and consumer wellness all reported customer volume growth, margin improvement and improved efficiency. In addition, methodical cash flow strengthening continued, which remains one of the most important reasons investors continue to pay attention to CVS even in challenging times. The strong operating result is underpinned by growing Aetna Medicare Advantage performance and consistently high retention in Caremark, confirming that the core business is healthy.

- Earnings per share: $1.60 adjusted vs. $1.37 expected

- Revenues: $102.9 billion vs. $98.85 billion expected

- The company posted a net loss of $3.99 billion, or $3.13 per share, for the third quarter. That compares with net income of $71 million, or 7 cents per share, for the same period a year ago.

However, the overall picture was significantly impacted by a massive goodwill write-down associated with the Health Care Delivery segment (a $5.7 billion goodwill impairment charge). This is not a current season issue, but a consequence of an earlier global strategy that relied on primary care expansion at a faster pace than was consistent with market realities. Now that CVS is backing away from opening a large number of clinics and reassessing the long-term earnings of this segment, a book value adjustment was necessary. This did not send the company into a loss because of poor performance, but because management set a more conservative view of the future of this part of the business.

From an operational perspective, however, Q3 can be viewed as progress. Improving medical results, stronger pricing in Caremark, and good retail channel performance signal that the rest of the business is performing well. Cash flow also confirmed that despite the accounting loss, the company is moving towards a better financial balance.

CEO comment

David Joyner built his commentary on two main lines: simplification and a return of confidence. He acknowledged the need to restructure and candidly described the issues that have carried over into 2025 - from a complex organisational structure to unmanaged growth in the primary care segment. But he also emphasized that CVS is uniquely positioned because it combines insurance, care, and pharmacy services on a scale unparalleled in the U.S.

Joyner also said the goal is not to maximize the size of the company, but to maximize the quality of the results. That is, to focus on areas where CVS truly generates value - a strong PBM, well-managed health insurance, a growing consumer wellness segment and synergies with its extensive pharmacy network. He believes this is a stronger foundation than the GAAP loss alone suggests.

Outlook

The company adjusted full-year guidance downward for GAAP results only, a direct result of the goodwill write-down. In contrast, everything else has been reaffirmed or increased. CVS now expects higher Adjusted EPS, better operating performance and stronger cash flow than originally planned. Management is betting on stabilization in key segments and an improved outlook in the insurance portfolio.

Also, the ongoing transformation of Health Care Delivery should result in lower costs and a more efficient structure, which is reflected in the updated outlook. The company is thus moving towards a model that can be less capital intensive while better monetizing its large ecosystem.

Long-term results

The company's long-term development shows very dynamic movements across key financial metrics. CVS's revenue has been growing continuously for four years, and the overall shift of roughly $80 billion shows how massively the company has expanded through acquisitions and organic growth. The core pillars - Aetna Insurance, PBM Caremark and CVS's retail network - have been steadily adding volume and holding their own in the U.S. healthcare market.

Brutal transformation is particularly evident at the cost and operating profitability levels. Cost of revenue has risen by more than $80 billion in four years, reflecting both higher drug and healthcare prices and the cost of operating clinical facilities. As a result, the company's overall operating margin has fluctuated significantly. The years 2022 and 2024 delivered strong operating results, while 2023 showed a sharp drop in profitability due to massive investments and a tough insurance environment.

As a result, operating profit ranged from nearly 14 billion in each year to sharp drops below 8 billion. The resulting net numbers were similarly volatile. Although the fodder for profitability has traditionally been Caremark and Aetna, vigorous expansion in care delivery has changed the overall profile of the company and increased the volatility of results. However, 2024 brought another year of improvement, which was borne out in this year's operating metrics.

From an equity investor's perspective, however, the key takeaway is that CVS has had very stable revenues, a high proportion of recurring revenue and a robust customer base over the long term. The problem has not been the demand profile, but the overly broad expansion into capital-intensive segments. So the reorganization the company is now undergoing is not cosmetic - it is a structural return to a model that has the potential to deliver more stable margins and more consistent results.

Shareholding structure

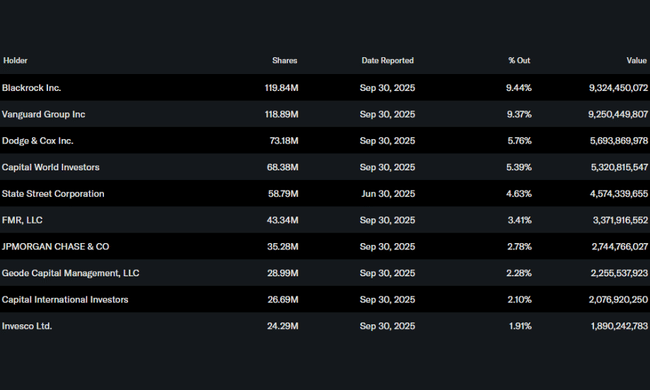

CVS shares have traditionally been held by large institutions, and this stability continues. Institutions hold nearly 90 percent of all shares, reflecting that the healthcare business - despite short-term turbulence - remains attractive to large pension funds and passive strategies over the long term.

Major shareholders include:

- BlackRock with approximately 119 million shares.

- Vanguard with 118 million shares.

- Dodge & Cox with 73 million shares.

- Capital World Investors with approximately 68 million shares.

Insiders hold just under one percent, which is typical for such a large healthcare company and reflects that the ownership structure is firmly anchored among long-term institutional investors.

Analyst expectations

Analysts expect 2025 to be a transitional year, weighed down by the impact of goodwill amortization, but operationally stable. The midpoint of their estimates works with CVS generating steady EPS growth and restoring double-digit operating profitability levels in 2026. Much of the analysts' focus is on management's ability to stabilize the Health Services segment and return Caremark's margins to historically higher levels.

How quickly the company can streamline cost-intensive projects in the Health Services segment will also play a significant role. If stabilization occurs as early as next year, EPS levels could be higher than current guidance suggests.