Meta enters the third quarter with clear evidence that its long-term strategy is gaining traction. Revenue growth remains robust across its core apps, the AI infrastructure build-out is accelerating, and engagement continues to rise in every major market. The company is positioning itself less as a social network and more as a foundational layer of the digital economy — one that spans compute, products, and immersive technologies.

But the headline numbers mask an accounting twist: a large, one-off tax charge that temporarily erased much of the quarter’s operational strength. While the underlying business shows healthy momentum, the distorted net profit forces investors to separate structural performance from short-term noise. The question now is how this tension affects Meta’s ambitious investment cycle, which is about to enter its most capital-intensive phase yet.

How was the last quarter?

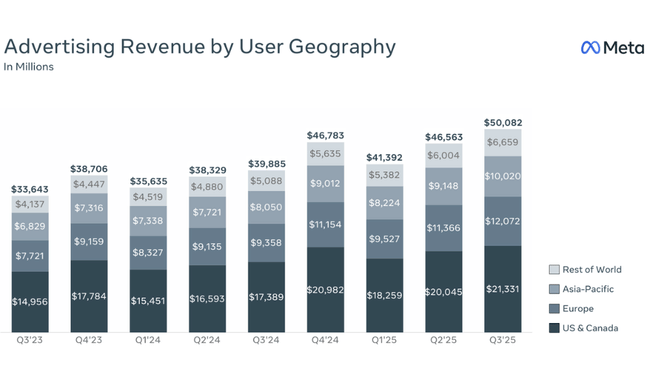

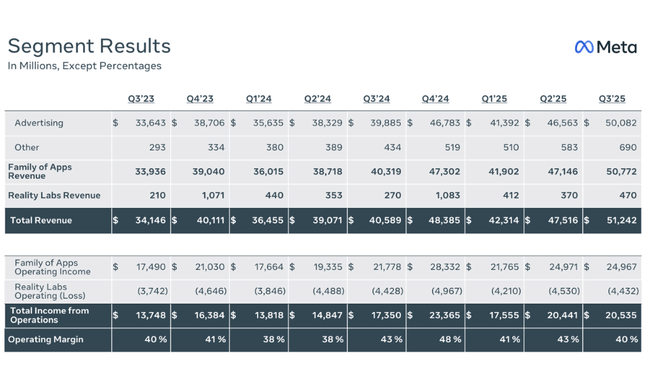

Meta $META delivered one of its most dynamic quarters in years in Q3 2025. Revenue grew 26% year-over-year to $51.24 billion, reflecting both strong demand for ad space and the growing value of AI-driven engagement across Facebook, Instagram, WhatsApp, and the Threads platform. Interestingly, the growth was not driven by a one-off blip, but by a steadier 14% increase in impression volume and a 10% increase in average cost per ad. This suggests that Meta can monetise users more effectively even in an increasingly competitive and regulated environment.

However, the extraordinary tax item associated with the passage of the One Big Beautiful Bill Act, which resulted in a one-time non-cash hit to net income of $15.93 billion, had a major impact on the interpretation of the results. As a result, the company reported net income of only $2.7 billion and EPS of $1.05, despite significantly better results from an operating perspective. If this item is abstracted, net profit would have been $18.64 billion and EPS $7.25 - figures that accurately reflect the strength of the business in the period.

Operating expenses rose 32% to $30.7 billion, reflecting soaring investments in data centers, cloud purchases, an expanding AI team, and continued hardware development within Reality Labs. Capital expenditures reached an extreme $19.37 billion. At the same time, the company generated $30 billion in operating cash flow - a fundamental signal that despite the enormous investment requirements, Meta has the strength to fund expansion internally.

User metrics reaffirmed the platform's robust growth. DAP reached 3.54 billion people, an 8% year-over-year increase, and engagement continues to shift toward formats that Meta effectively monetizes. Add in growing AI glasses revenue, the rapid emergence of Meta Superintelligence Labs, and a still-strong position in the advertising ecosystem, and you get a picture of a company that is in a strategic phase of accelerating growth - while also having to balance high costs and regulatory pressure.

CEO comment

Mark Zuckerberg described the quarter as one of the most important milestones in the company's modern history. He highlighted the rapid emergence of Meta Superintelligence Labs, where he said the company is at the beginning of a cycle that could redefine the capabilities of both consumer and enterprise AI models. He also highlighted the success of AI glasses and the growing adoption of products that connect the real world with digital services. He stressed that if Meta can capture just a fraction of the overall potential of emerging technologies, the company is in for a peak dynamic period in the years ahead.

At the same time, he openly admitted that the expansion of AI infrastructure requires much higher upfront costs than originally anticipated, which translates into expectations for 2026. Meta will aggressively ramp up investment in computing capacity - whether in the form of its own data centers or third-party contracts. Zuckerberg also warned that the regulatory environment, particularly in the EU and the US, could bring additional volatility in the coming quarters. But the outlook remains ambitious and growth-oriented.

Outlook

Meta's CFO expects revenue between $56 billion and $59 billion in the fourth quarter, with the advertising segment continuing to be the main driver. Reality Labs, on the other hand, is expecting a decline, as this time last year it was reporting Quest 3S, which led to a very high comparative base. Capital expenditures for the full year move into the $70-$72 billion range, while total expenses are expected to be $116-$118 billion. The company also notes that it is already planning for significantly higher infrastructure investment in 2026, which means further growth in capital intensity and operating costs.

Despite this, Meta expects strong engagement growth, ad systems modernization and the advent of new AI features to enable noticeable revenue growth in 2026. It also sees significant room for monetizing generative AI in consumer applications and developing new enterprise services based on advanced models.

Long-term results

Meta has had a highly volatile period, which is reflected in the long-term numbers as a combination of extremely fast growth, investment cycles and short-term fluctuations caused by the economic environment or ambitious projects. Revenues in 2024 grew 22% to $164.5 billion, building on an already strong previous growth trend. Over the past four years, the company has increased revenues by roughly $47 billion purely through a combination of increasing engagement and improved efficiency of its advertising systems. The gross profit of $134.3 billion shows that Meta has been able to maintain high margins despite rising infrastructure costs.

Operating costs also reflect a transformational strategy. These have been rising with investment cycles over the long term, and while they will be $65 billion in 2024, their growth rate is significantly lower than in previous years, indicating stabilisation after extensive restructuring. Most striking, however, is the growth in operating profit, which shoots up 48% to $69.4 billion in 2024, a signal of strongly growing monetization efficiencies across the entire family of applications.

Net profit increased 59% to $62.4 billion in 2024, which Meta achieved despite a higher tax burden. Earnings per share increased to $24.61, despite a continued buyback program that reduces the number of shares outstanding. EBITDA was $86.8 billion, clearly demonstrating a combination of high margins, a strong cash-flow profile and robust investment returns outside of the Reality Labs segment, which remains heavily loss-making but strategically critical.

Meta's long-term trajectory shows a company that has the ability to generate massive profits even in an environment of enormous investment, an important signal for investors evaluating long-term growth potential.

News

- Meta Superintelligence Labs' rapid emergence

- Strong growth in AI glasses and continued adoption of new devices

- Advertising system sharply increases efficiency thanks to AI

- Significantly higher capital expenditure in 2026

- Regulatory risks in the EU and US continue to rise

Shareholder structure

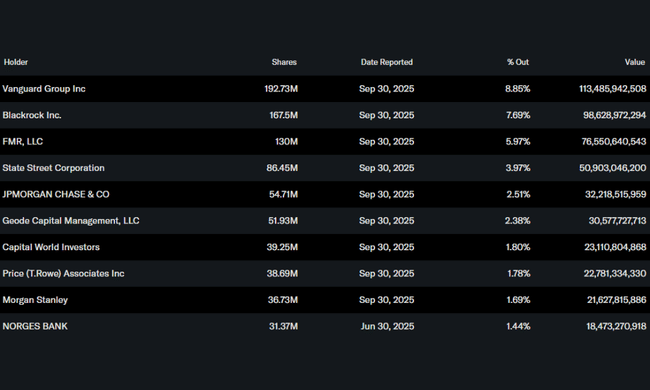

Meta has an extensive institutional ownership base dominated by the largest global asset managers. Approximately 79% of the shares are held by institutions, with the main investors being Vanguard Group with 8.85%, BlackRock with 7.69%, FMR with nearly 6% and State Street with just under 4%. Insider shareholding is roughly 0.06%, which is consistent with the structure of large technology firms where the shares of managers and founders are diluted by the impact of large-scale buybacks over the long term. Overall, this is a very stable ownership mix that maintains low volatility and high institutional confidence.

Analyst expectations

The analyst consensus remains strongly positive. Most analysts see room for further revenue growth in both the advertising segment and AI-native products. Q4 revenue is estimated to exceed $57 billion and analysts expect adjusted EPS to be back on a high growth trajectory as the one-time tax item will not recur. The outlook for the full year 2026 is also robust, with double-digit revenue and earnings growth expected, but also increased capital intensity that investors will need to evaluate carefully.