Warner Bros. Discovery entered the third quarter at a moment when its hybrid media strategy is being tested more než ever. The company continues to juggle the decline of its traditional TV networks with the growing strength of its streaming platforms and film studios, creating a mixed picture that reflects both the challenges and the long-term opportunity ahead. Even as total revenue dipped year over year, momentum in several high-value segments began shifting investor attention toward the company’s medium-term growth prospects.

The Q3 2025 results highlight this contrast clearly: linear TV and advertising remain structural headwinds, while the studio business delivered a stronger-than-expected performance and the streaming division showed improving profitability and renewed subscriber engagement. Together with a meaningful rebound in free cash flow, these trends suggest that WBD is not merely enduring the industry reshuffle — it is laying the groundwork for a return to sustainable growth.

How was the last quarter?

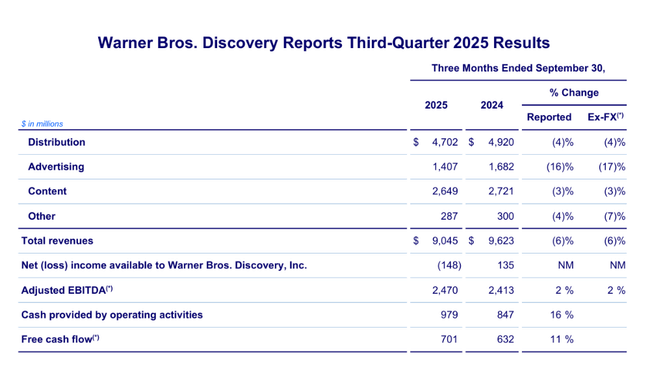

Third quarter revenues were $9.0 billion, down 6% year-over-year, with weakness primarily seen in advertising and traditional linear channels. Advertising revenue and distribution fell 16% and 4%, respectively, reflecting continued declines in cable viewership and weaker demand in key advertising segments. Still, the results were less negative than the market expected, and some investors see a possible bottom in linear erosion.

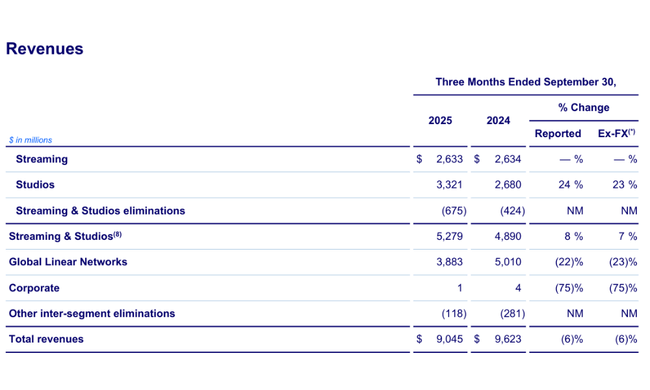

Streaming and studios offer a significantly better picture. Streaming revenue remained steady year-over-year at $2.63 billion, the company increased subscribers by 2.3 million, and managed to combine subscription growth with profitability growth for the first time since the pandemic years. The studios segment delivered the biggest surprise, with revenues up 24% year-over-year thanks to strong film and TV production, which partially erased the one-time negative effects of last year's Olympic sublicense.

At the profitability level, the numbers were even more compelling. Adjusted EBITDA rose 2% to $2.47 billion, despite continued pressure from linear TV. The improvement was underpinned by streaming and studios, which together posted EBITDA growth of 58%. Cash flow also pleased: free cash flow of $701 million was up 11% and the company continued its rapid deleveraging, paying down $1.2 billion of debt in the quarter.

However, overall net income fell into a $148 million loss due to restructuring charges and asset amortization. This is a typical accounting phenomenon for $WBD, while operationally the company is generating solid profitability.

- Don't overlook: Netflix wants to buy HBO Max from Warner Bros.

CEO Commentary

In particular, management highlighted the company's strategic successes in streaming and studios. According to the CEO David Zaslav the growth in streaming profitability is "fundamental confirmation that the model is moving into a mature phase" where it is no longer about maximising subscriber volume, but about monetising through advertising, higher tariffs and cost optimisation. Zaslav also highlighted the performance of the studios, which are once again becoming one of the engines of growth thanks to a better pipeline of movies and TV productions.

On the other hand, management openly admits that linear media will continue to be a source of pressure. The company is therefore accelerating a reorganization to cut costs, simplify the structure and allow for a faster shift of capital toward faster-growing divisions. Zaslav reiterated the need to reduce debt, which he calls "the number one strategic priority" and which should allow the firm greater flexibility in the years ahead.

Outlook

Warner Bros. Discovery $WBD continues to position itself as a hybrid media player, combining the production power of Hollywood studios with global streaming. The company expects streaming margins to continue to grow in the coming quarters while studios benefit from a strong film calendar and stabilizing TV production.

A key question mark is the rate of erosion of linear TV. WBD plans to mitigate this impact through further savings, contract restructuring and greater integration of content between streaming and traditional distribution. The company also announces continued debt reduction to be a key pillar of its improved financial position in 2026.

Long-term results

The long-term numbers show WBD's media transformation in full view. While 2021 was still a period of strong profitability, the massive acquisition of WarnerMedia dramatically increased costs, depreciation and debt. The years 2022 to 2024 were marked by the scale of the integration and high restructuring costs - and also by deep losses caused by the accelerating decline in linear revenues.

Revenues in 2024 were $39.3 billion, down nearly 5% from 2023. While gross margins remained relatively stable, operating expenses rose 44%, resulting in an operating loss of over $10 billion. At the same time, EBITDA fell dramatically from $22.4 billion to $11.6 billion. These results reflect the cost pressures of integration, along with pressure on traditional segments.

It is important to emphasize, however, that WBD has already passed the worst phase of its transformation. The latest quarterly data shows cost reductions, studio growth, streaming stabilization and improving cash flow. Longer term, the key remains the pace of debt reduction - if the company can reduce leverage to 2.5x EBITDA, it will open the way for a return to strategic flexibility.

News

During the quarter, the company grew its streaming subscriber base to 128 million, continued to reorganize its linear business, and paid down $1.2 billion of debt. Studios benefited from a more successful movie season and strong production is expected to continue in 2026. WBD also stepped up cost optimization, which is already delivering positive cash flow results.

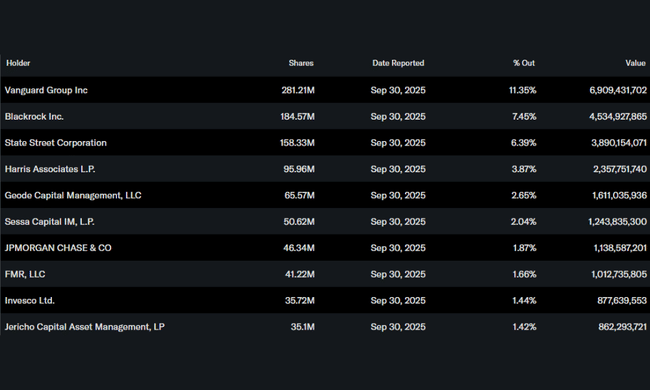

Shareholding structure

Institutional investors hold approximately 73.6% of the shares. The largest shareholders are:

- Vanguard Group - 11,35 %

- BlackRock - 7,45 %

- State Street - 6,39 %

- Harris Associates - 3,87 %

Insiders own roughly 5.95% of the company, which is a relatively high share among media companies.

Analysts' expectations

According to Wells Fargo'smost recent report dated October 31, 2025, analyst Steven Cahall reiterates a Buy rating on WBD Overweight and a $16 price target . Cahall argues primarily:

- Stabilization of streaming with growing EBITDA.

- a strong recovery in trials

- continued deleveraging

- the potential to restructure the linear segment