Occidental entered Q3 2025 at a decisive moment in its multi-year transformation, and the latest results confirm a business that is gaining strength across all operating lines. Production exceeded management’s own guidance, operating cash flow moved higher, and debt reduction accelerated for the fourth consecutive quarter. The company also executed one of its most meaningful strategic pivots in recent years by moving forward with the divestiture of OxyChem, a shift designed to concentrate capital on oil, gas and emerging low-carbon technologies — areas that now form the backbone of its long-term competitiveness.

Taken together, the quarter paints a picture of a company that has regained operational clarity and financial discipline. Occidental is not only generating solid free cash flow at current commodity prices, but is also rebuilding balance-sheet flexibility at a speed that could soon allow for a materially larger capital-return program. With debt down by more than a billion dollars in just three months, the company is steadily approaching a new phase of the cycle — one in which strategic reinvestment and shareholder distributions can grow in tandem.

How was the last quarter?

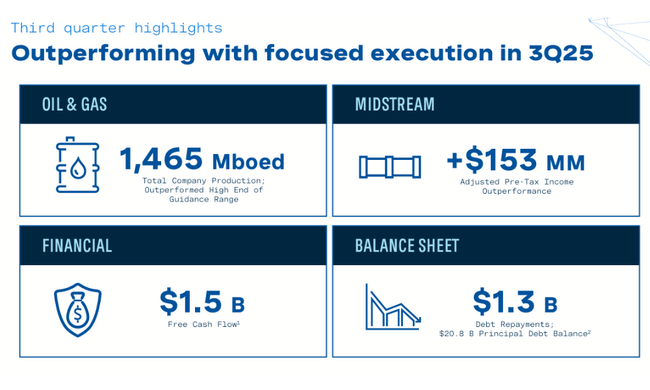

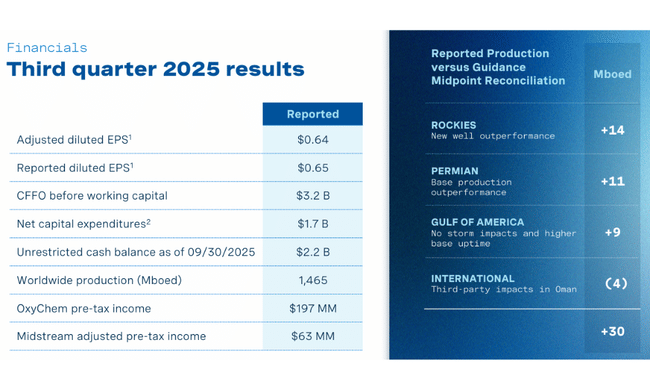

Occidental $OXY entered the third quarter of 2025 in very good shape and the results ended up exceeding most expectations, especially at the level of operations and cash flow. The company reported operating cash flow and operating cash flow of $2.8 billion and $3.2 billion, respectively, before working capital changes, signaling robust performance of key upstream assets as well as continued investment discipline. Capex reached $1.8 billion, and with $39 million of contributions from non-controlling interests, the company generated $1.5 billion of free cash flow before working capital - the resulting FCF thus confirmed Occidental's ability to generate cash even in an environment of relatively stable but not extremely high commodity prices.

The operating side was also very strong. Global production averaged 1,465 Mboed, beating the high end of guidance. Permian remains the dominant pillar of the business with an average production of 800 Mboed, while Rockies & Other Domestic brought in 288 Mboed, Gulf of America 139 Mboed and the International segment 238 Mboed. It was the combination of higher production volumes and slightly better pricing that helped the Oil & Gas segment to a pretax profit of $1.3 billion. Realized oil prices rose 2% to $64.78/bbl, while domestic realized gas prices strengthened 11% to $1.48/Mcf. A persistent headwind was weaker NGL prices, which fell 5% quarter-on-quarter.

Midstream and marketing also beat guidance, although they posted lower earnings than in the previous quarter due to lower Waha-Gulf spreads and higher costs associated with increasing activity in low-carbon projects. Pre-tax profit was $93 million and WES equity income was $156 million. On the other hand, OxyChem was a weak spot, with earnings falling to $197 million due to weaker prices and volumes across the portfolio, albeit partially offset by lower input costs.

At the overall profitability level, the firm reported net income of $661 million ($0.65 per share) and adjusted earnings of $649 million ($0.64 per share). Occidental also continued its aggressive deleveraging, paying down $1.3 billion in the quarter and pushing total debt to $20.8 billion. This move, along with the sale of OxyChem, which management called a transformational milestone, further strengthens financial flexibility and allows the company to increase returns to shareholders.

CEO commentary

CEO Vicki Hollub highlighted that the third quarter is a testament to the exceptional operating performance, disciplined investments and strength of the upstream portfolio. She said Occidental outperformed targets in both the oil and gas segments while also outperforming in midstream and marketing. A key point is The sale of OxyChemwhich provides the company with capital to further reduce debt, strengthen returns to shareholders and accelerate investment in its highest-return segments. This confirms management's strategic shift towards a company focused primarily on upstream, complemented by low-carbon technologies capable of delivering a steady stream of new opportunities.

Outlook

Occidental enters the next quarters with a resilient production base, relatively stable price realizations and strong capital discipline. Management expects core upstream to continue to be a key source of cash flow growth, supported by efficiencies at Permian as well as continued stability in international assets. The weaker environment in petrochemicals should remain transitory, while midstream will be more sensitive to price spread structures, but still contributing stable results continuing to be complemented by WES dividends.

The company also reaffirms its long-term priority to reduce debt - with room to continue to gradually shift capital allocations towards share buybacks and dividend increases once the $20.8bn debt target is reached. Strategically, Occidental will continue to focus on diversifying its upstream portfolio and developing low-carbon solutions, including DAC projects, which Hollub also highlighted.

Long-term results

Occidental's long-term financial performance confirms the cyclical nature of the oil sector, but also demonstrates the company's ability to offset volatility through cost management and portfolio optimization. Revenue in 2024 was $27.1 billion, down 4.35% year-on-year, following a weaker 2023, when revenue fell 21.85%. However, these results reflect lower oil prices and normalisation after an exceptionally strong year in 2022, when Occidental increased revenues by almost 40%. The main changes were also reflected in margins, with gross profit of $9.6 billion in 2024 virtually flat, indicating successful cost control even with lower commodity prices.

Operating profit fell to $6 billion, down 8% year-on-year, while net profit fell 35% to $3 billion. The results thus remain well below the extremely strong levels of 2022, when net profit exceeded $13 billion. EBITDA fell to $12.7 billion in 2024, a 12% decline, but still a solid figure that gives the company comfort in managing debt. The EPS movement follows the movement in net income - $2.44 per share in 2024 implies a 37% year-on-year decline, but these are figures fully explained by the energy price cycle.

Long-term results thus confirm that Occidental, while not immune to the commodity price downturn, can maintain a healthy balance sheet, high levels of operating cash flow and reduce debt in a cyclical environment, which remains a key strategic objective.

News

The most significant event of the quarter was the announced sale of the OxyChem division, which management describes as a major step in the company's transformation. This transaction will allow the company to further strengthen its balance sheet, accelerate debt repayment and better direct capital to the highest return segments, primarily upstream and low-carbon technologies. Occidental has also continued its extensive deleveraging program, repaying $1.3 billion during Q3 2025 alone, a significant step toward its strategic goal of reducing debt to levels that enable greater shareholder returns. The company also highlighted growing activity in low-carbon projects, which translated into higher costs in the midstream and marketing segments.

Shareholding structure

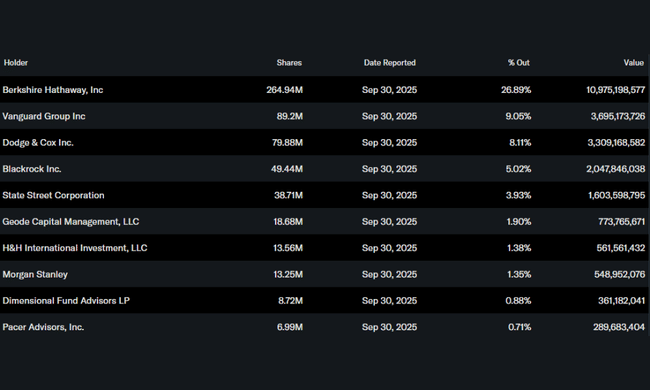

Occidental has a highly concentrated shareholder structure, with Berkshire Hathaway dominating with nearly 27% of all shares, and has long supported the company's strategy of focusing on upstream, cash returns and disciplined investment. The institution holds over 51% of all shares and more than 70% of the free float, indicating high interest from professional investors. The largest institutional shareholders include Vanguard Group (9.05%), Dodge & Cox (8.11%) and BlackRock (5.02%). In total, more than 1,500 institutions hold Occidental stock, confirming the company's firm footing in the portfolios of long-term investors.

Analysts' expectations

Shares of Occidental Petroleum have come under pressure in recent months due to weakening oil prices and waning confidence across the energy sector. The title now trades at roughly $41 per share, marking a roughly 20 percent decline over the past twelve months, at a time when earnings outlooks have been gradually lowered. Still, some analysts expect some room for growth, backed by solid margins, gradual deleveraging and a disciplined approach to investment. At the same time, Occidental is expanding its carbon capture business through its 1PointFive subsidiary and continuing its long-term efforts to strengthen its balance sheet, showing a desire to balance its traditional oil business with new opportunities in low-carbon technologies.

Wall Street estimates suggest a more moderate outlookreflecting investors' overall caution towards energy titles. The average analyst price target of around $51 implies roughly 20 percent potential over the next twelve months, although the range of projections is wide - from $38 to $63. At the same time, the consensus indicates that Occidental remains more of a defensive headline than a growth story, as revenues are expected to decline slightly through 2027, operating margins are expected to stagnate, and valuations are below long-term averages. According to models based on analyst estimates, the stock could reach about $43 in 2027, implying only a minimal annual return. For investors, this underscores the company's character as a stable energy player focused on cash, dividends and debt reduction, not dynamic growth.