Snowflake continues to prove that demand for modern data platforms has not peaked, even as the cloud market matures and enterprise budgets remain selective. In the third quarter of fiscal 2025, the company demonstrated that usage-driven analytics, AI-ready data architectures, and vendor neutrality remain compelling value propositions for large organizations navigating increasingly complex data environments.

At the same time, the quarter reinforced a familiar tension in Snowflake’s story. While revenue growth remains strong and customer engagement continues to deepen, operating costs stay elevated as the company prioritizes product expansion, AI integration, and ecosystem development. For investors, the key debate is no longer whether Snowflake can grow — but how efficiently that growth can be converted into durable margins over the next phase of the cycle.

How was the last quarter?

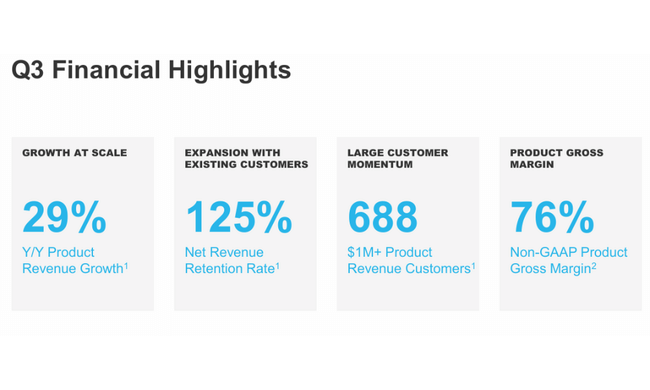

Snowflake reported revenue of $1.21 billion in the third quarter of fiscal 2026, representing 29% year-over-year growth. Product revenue remains a key metric, reaching $1.16 billion and also growing at a 29% rate. This confirms that the core of the business - the data platform itself - remains the main driver of the results.

A very important signal of the quality of the growth is the retention rate of revenue from existing customers, which reached 125%. In other words, existing clients are, on average, increasing their spend by a quarter a year without the company having to aggressively chase new customers. The number of clients with annual product sales exceeding $1 million rose to 688, indicating Snowflake $SNOW's growing position in large organizations.

From a profitability perspective, the improving operating structure is evident. Gross margin on product sales on a non-GAAP basis is around 76% and the company reported a positive operating result on an adjusted basis. Free cash flow exceeded $110 million, confirming that Snowflake is gradually moving from a growth phase to a more mature model with an emphasis on cash flow.

CEO commentary

CEO Sridhar Ramaswamy in his comments, highlighted that Snowflake is becoming a cornerstone of customers' data and AI strategies. He paid particular attention to the rapid adoption of the product Snowflake Intelligencewhich, according to management, has seen the fastest ramp-up in the company's history.

Management is also highlighting strategic partnerships with AI model providers, cloud services and application platforms. The goal is not just to provide a repository of data, but to create an environment where companies can instantly translate data into decisions, automation and real business value.

Outlook

For the fourth fiscal quarter, Snowflake expects product revenue in the range of $1.195 billion to $1.200 billion, representing additional year-over-year growth of approximately 27%. At the same time, the company expects continued improvement in operating margin and steady free cash flow generation.

At the full fiscal year 2026 level, management has reaffirmed product revenue expectations of around $4.45 billion, with a target product gross margin of approximately 75% and an operating margin approaching 9%. This suggests that Snowflake is no longer just a "future story" but is gradually becoming a structurally profitable platform.

Long-term results

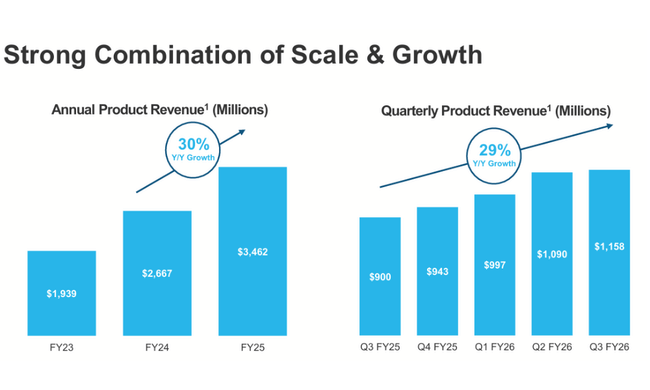

Looking at the last few years, it is clear that Snowflake is undergoing extremely rapid expansion. Revenues have grown from just under $600 million in 2021 to over $2.8 billion in 2024, and the growth rate remains above average even after this expansion. Gross profit is growing even faster than revenue itself, demonstrating the very strong operating leverage of the business.

At the same time, it is evident that the company is still investing massively in operations, development and acquisitions. While the operating loss is relatively stable year-on-year, Snowflake remains in a phase where it prioritises long-term platform building over short-term accounting profitability. EBITDA is gradually improving, indicating a tipping point that could be pivotal to the company's investment story in the years ahead.

Shareholder structure

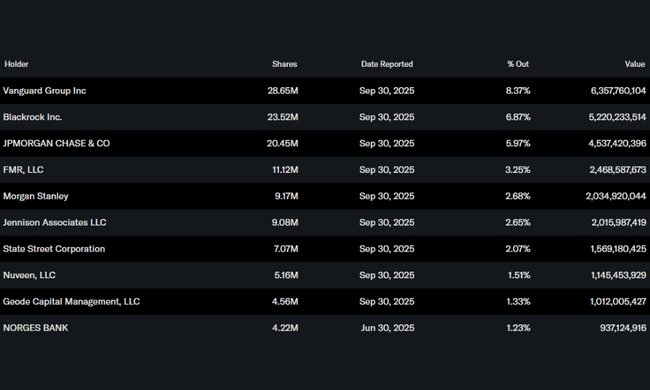

Snowflake's shareholder structure confirms strong institutional trust. Approximately 74% of shares are held by institutional investors, with Vanguard, BlackRock and JPMorgan among the largest. Relatively low insider ownership is typical for companies at this stage of development and does not indicate a structural problem, especially with such a strong institutional backing.

Analyst expectations

Analysts agree that Snowflake is among the key long-term bets for the development of the data economy and artificial intelligence. Expectations are primarily focused on continued spending growth from existing customers, monetization of AI tools, and incremental margin improvement. Target prices are generally well above current levels, with valuation pressure remaining the main risk should growth slow.