Salesforce is no longer trying to prove that it can grow. That question has effectively been settled. What Q3 FY2026 shows instead is a company focused on extracting durable value from its scale — tightening cost discipline, expanding margins, and converting revenue into consistent free cash flow. The narrative has shifted from expansion to execution.

Artificial intelligence is undergoing a similar transition inside the company. Once positioned mainly as a strategic vision, AI is now embedded into the product stack in ways that customers are actively paying for. This marks an important inflection point: Salesforce’s AI strategy is moving from optional enhancement to revenue-driving infrastructure, reinforcing a more mature and resilient business model.

How was the last quarter?

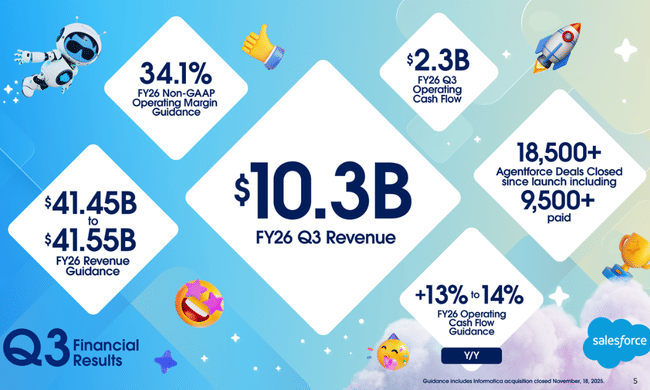

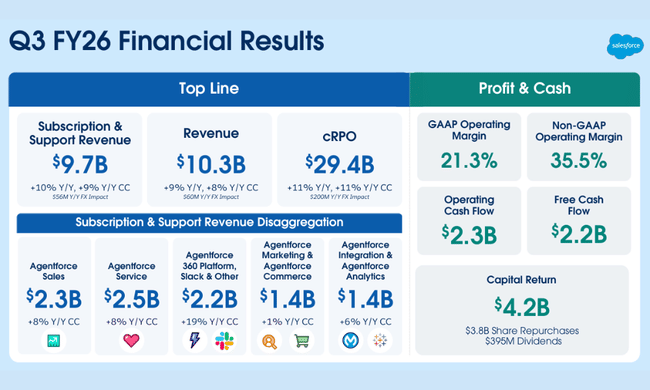

The third quarter of fiscal year 2026 was one of the strongest for Salesforce in years, clearly showing that the company can combine steady revenue growth with significant improvements in profitability and cash flow. Total revenue reached $10.3 billion, up 9% year-over-year, with the key subscription and support segment growing to $9.7 billion, up 10% year-over-year. This growth was primarily driven by continued adoption of cloud solutions, expansion with existing customers and growing demand for AI products.

Customer commitments are a very strong signal going forward. Current Remaining Performance Obligation (cRPO) rose to $29.4 billion, up 11% year-on-year, while total RPO climbed to $59.5 billion, also up 12%. These figures confirm a robust pipeline of future revenues and high revenue visibility for the next few years.

Profitability moved significantly higher. GAAP operating margin reached 21.3%, while non-GAAP operating margin rose to 35.5%, the result of management's long-term push for operational efficiency, cost optimization and better monetization of the software portfolio. Operating cash flow was $2.3 billion, up 17% year-over-year, and free cash flow was $2.2 billion, up 22% year-over-year.

Salesforce $CRM also aggressively returned capital to shareholders. During the quarter, the company repaid and repurchased shares totaling $4.2 billion, of which $3.8 billion was attributable to share repurchases and $395 million to dividends. This underscores management's confidence in the long-term cash generation and stability of the business.

Management commentary

Chief Executive Officer Marc Benioff in his comments, emphasized that the third quarter results confirm the soundness of the strategic turnaround that Salesforce has initiated in recent years. According to him, the company is now on a much firmer footing than ever before, combining steady growth with high operational efficiency and strong cash generation. He sees the results as proof that Salesforce can grow in a more challenging macroeconomic environment without having to revert to aggressive cost increases.

Benioff has repeatedly emphasized the role of artificial intelligence and the data platform as a key driver of the next phase of growth. He said AI at Salesforce is moving from the experimental phase into real business, where customers are seeing tangible benefits in productivity, automation and better use of data. It is the deep integration of AI into core products - CRM, data platform and analytics tools - that management believes will enable the firm to increase the value of contracts with existing clients, not just chase new customers at the cost of margin pressure.

He also devoted a significant portion of his comments to internal changes in the firm's operations. He stressed that the emphasis on operational discipline, a simpler management structure and clear prioritisation of investments is not a short-term measure, but a permanent part of the company's culture. Salesforce, he said, has moved to a stage where it is able to deliver high margins over the long term while investing in innovation without compromising financial stability.

Outlook

Salesforce's outlook remains cautiously constructive. The company expects revenue growth to continue to be more in the single digits, but with an increasing focus on margins and cash flow. The key takeaway for investors is that management is making it clear that a return to aggressive "growth at any cost" is not on the agenda.

The next few quarters will therefore be all about whether AI functions can be translated into actual customer budget items and whether cost discipline can be maintained with continued investment. If so, Salesforce may gradually move into the category of technology companies that are seen as steady cash-flow machines rather than growth experiments.

Long-term results

A look at the long-term numbers confirms that Salesforce has moved from a fast-growing but cost-intensive company to a highly profitable software leader with significant operating leverage. The company's annual revenue has been steadily increasing in recent years, and for fiscal 2026, management now expects total revenue to be in the range of $41.45 billion to $41.55 billion, which equates to roughly 9% to 10% year-over-year growth. Importantly, growth is still largely organic and underpinned by subscriptions rather than one-off items.

The fundamental structural change in recent years has been the dramatic improvement in margins. Whereas just a few years ago operating margins were well below 20%, today Salesforce is targeting long-term non-GAAP operating margins of around 34% and GAAP margins of over 20%. This shift is the result of cloud model scalability, increased automation, product consolidation and more disciplined cost management.

The company's long-term ability to generate cash is also a strength. Both operating and free cash flow are growing faster than revenue itself, and Salesforce now expects year-over-year cash flow growth for the full fiscal year 2026 in the range of 13% to 14%. This gives the company room to not only invest in AI, data platforms, and new acquisition integration, but also to increase long-term return on capital for shareholders through buybacks and dividends.

Over the long term, Salesforce profiles itself as a combination of a stable enterprise software player and a growth AI platform. High levels of recurring revenue, strong contract visibility, growing margins and robust cash flow give the company a very solid foundation for the years ahead - even in a slowing global economy.

News

The most visible news of the quarter is the de facto transition of AI from the pilot project phase to actual deployment with customers. Salesforce significantly expanded commercial use of the platform during the quarter Agentforcewhich enables companies to deploy autonomous AI agents directly into sales, customer support and marketing processes. For the first time, management openly communicated that Agentforce is no longer an add-on to existing licenses, but a standalone layer that increases the value of contracts and extends their length. This is particularly important in terms of future AI monetization, which is starting to be reflected in the order structure.

Another concrete shift has occurred with Data Cloudwhich became the centerpiece of the company's overall AI strategy this quarter. Salesforce has now enabled customers to connect structured CRM data with external data sources in real time and use that data instantly in AI models. This has practical implications, especially for large enterprise clients, who are able to integrate AI into their day-to-day operations without having to build their own data infrastructure. Management highlighted that Data Cloud is one of the fastest growing products in the portfolio today and a key consideration in renewing and expanding contracts.

There has also been significant innovation in the areas of productivity and collaboration. Salesforce has further deepened the integration of AI capabilities into Slack, expanding the use of AI assistants to summarize communications, automate tasks, and find information across corporate data. This is no longer just about improving the user experience, but an effort to increase users' daily activity and strengthen Slack's ties to other Salesforce products. This is key to the long-term strategy, as Slack is meant to act as an entry interface to the entire platform.

Shareholder structure

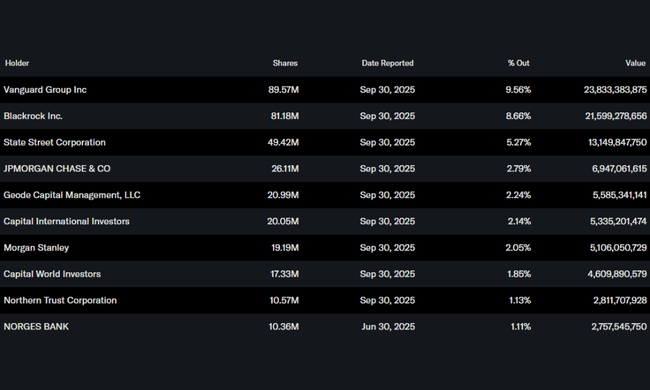

Salesforce's ownership structure is highly institutional, which is typical for a company of this size and importance. The vast majority of shares are held by large asset managers and index funds, while insider ownership remains relatively low. This implies greater stock stability, but also sensitivity to broader market movements and changes in the capital allocation of large funds.

Analyst expectations

Analyst consensus views the current results as confirmation that Salesforce has successfully completed the transition to a more profitable phase. Some analysts have maintained a buy recommendation following the results release and are working with price targets that imply further upside potential, underpinned primarily by a combination of stable sales, growing margins and strong cash flow. A key theme going into the next few quarters remains the company's ability to turn AI from a competitive advantage into a sustainable long-term revenue source.