Semiconductor markets may rise and fall, but some companies sit above the cycle rather than inside it. Synopsys closed fiscal Q4 2025 with results that reinforce its role as structural infrastructure for the chip industry, not just another vendor exposed to demand swings. While hardware manufacturers wrestle with volatility, Synopsys continues to benefit from its position at the very beginning of the value chain, where design decisions are made years before chips reach production.

For investors, this positioning matters more than headline growth rates. Deep integration into customers’ workflows, high switching costs, and mission-critical software give Synopsys pricing power and earnings visibility that few semiconductor-related firms can match. In an environment shaped by export controls and geopolitical friction, that resilience increasingly defines its long-term investment appeal.

How was the last quarter?

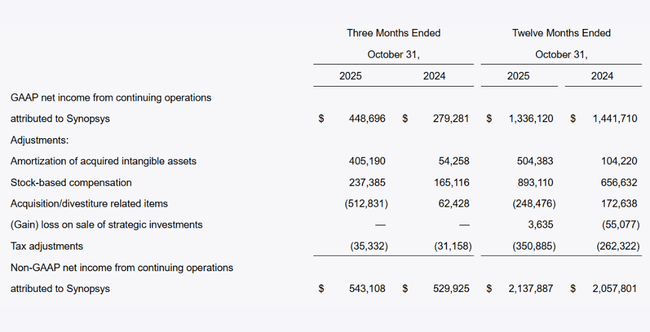

Synopsys $SNPS achieved revenue of $2.26 billion in the fourth fiscal quarter of 2025, beating the high end of its own guidance. A significant portion of the growth was driven by the contribution of the Ansys acquisition, which has already made a significant impact on results in the early months of integration. The company thus confirmed that the integration is proceeding smoothly and without any visible disruption to operations.

At the profitability level, the company also delivered a very solid performance. Earnings per share on a non-GAAP basis beat expectations, reflecting a combination of revenue growth and good cost discipline. Operating margins remain strong, which is a major advantage for a high value-added software company.

The development of backlog, i.e. contracted orders for the future, is also an important signal. This has reached approximately USD 11.4 billion, giving the company very good visibility of future revenues and reducing its sensitivity to short-term fluctuations in demand for new chips.

CEO commentary

CEO Sassine Ghazi said that fiscal 2025 was a watershed year for Synopsys as it moved the company from being a leader in chip design towards a broader platform covering the entire process from design to system level. He stressed that the goal for the period ahead is sustainable growth and incremental margin improvement, not aggressive expansion at any cost.

CFO Shelagh Glaser highlighted in particular the strength of the backlog and the expectation of another record year in 2026. She said the firm has the financial flexibility to manage the Ansys integration while continuing to invest in the development of new tools.

Outlook

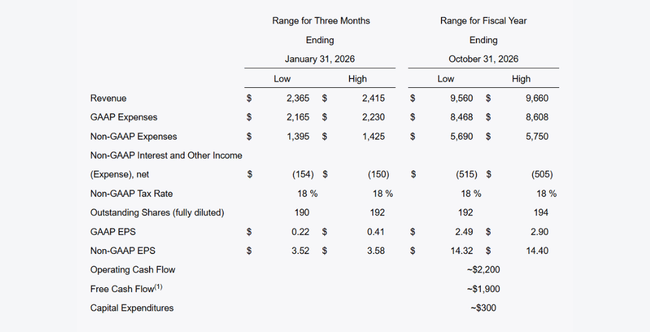

For fiscal year 2026, Synopsys expects another record year in revenue, at approximately $9.6 billion at the midpoint of the outlook. This growth already fully incorporates the contribution of Ansys, while anticipating the divestment of some non-core businesses, indicating a focus on key segments with the highest added value.

The company also anticipates continued strong cash flow, with free cash flow expected to be around USD 1.9 billion. This gives Synopsys room for both further strategic moves and a return of capital to shareholders.

Long-term results

A long-term view of the performance shows a company with a clear upward trend. Revenues have increased steadily in recent years and the growth rate has gradually accelerated, especially in the last fiscal year. Synopsys has been able to grow even during periods when parts of the semiconductor market have been stagnant, confirming the resilience of its business model.

Gross profit has been growing along with sales for a long time, showing that the company maintains a strong pricing position and is not forced to discount margins. Operating profit remains stable and is growing over the longer term, even as the company continuously increases investment in the development and expansion of its product portfolio.

Net profit shows fluctuations between years, but the overall trend is upwards. Earnings per share have been increasing over the long term, with the number of shares outstanding remaining relatively stable. EBITDA is gradually increasing, confirming the company's ability to generate cash and fund its growth without significant debt.

From a debt perspective, Synopsys is a conservatively managed company. It does not have the character of a highly leveraged company and has sufficient cash flow to cover operations and investments, which is a significant advantage in the technology sector.

News

The biggest strategic development is the continued integration of Ansys, which significantly expands Synopsys' offering towards system simulation and complex engineering. The company has also completed the divestment of part of its software integrity business, cleaning up its structure and focusing on key areas of highest long-term value.

Shareholding structure

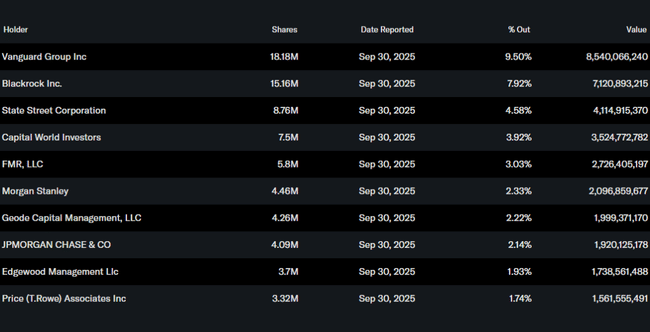

Synopsys' shareholder structure is strongly institutional. More than 93% of the shares are held by institutional investors, indicating high long-term capital confidence. Vanguard Group, BlackRock and State Street are the largest shareholders. Insider holdings are minimal, which is typical for a firm of this size and nature.

Analyst expectations

Analysts view Synopsys as one of the best bets for long-term growth in the semiconductor industry without direct exposure to its cyclicality. The company is praised for its steady growth, high margins and strong position in chip design, where it has very limited competition. The successful integration of Ansys and the ability to further expand the offering towards system solutions remains a key theme for the coming years.