The logistics sector is entering 2026 under far more complex conditions than in recent years. Trade disruptions, shifting geopolitical alignments, and persistent cost pressures are exposing which operators are structurally strong and which were primarily beneficiaries of a favorable cycle. Against this backdrop, FedEx is deep into a transformation designed to fundamentally alter how its network generates profit.

The second fiscal quarter matters less as a snapshot and more as proof of execution. Rising earnings, an improved outlook, and the approaching separation of the Freight business together signal whether cost discipline and network optimisation are translating into sustainable value. For investors, this quarter helps define how FedEx should be valued once the transformation moves from promise to permanence.

How was the last quarter?

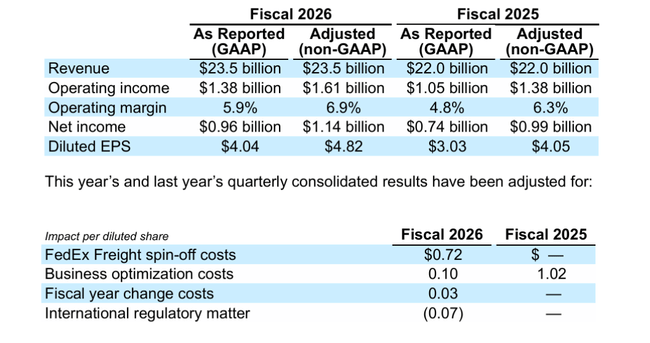

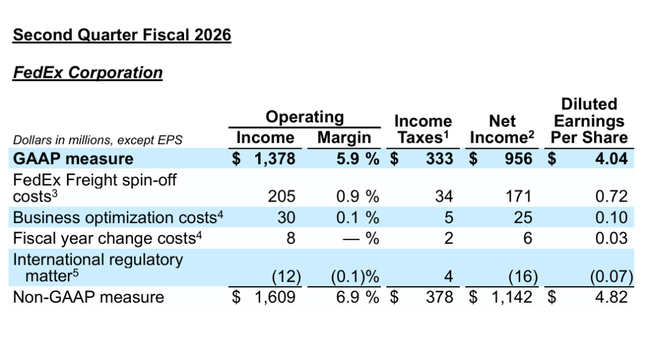

FedEx $FDX delivered year-over-year improvement across key metrics in the second fiscal quarter of 2026, despite a difficult external environment. Revenue was $23.5 billion, a solid increase from $22.0 billion in the same period last year. More importantly, however, is the improvement in profitability: operating profit on an adjusted basis rose to US$1.61 billion and operating margin moved to 6.9%, up from 6.3% a year ago.

Net income on an adjusted basis was $1.14 billion and adjusted earnings per share were $4.82, a significant shift from $4.05 a year ago. This growth was driven by a combination of higher revenue from US domestic shipments, stronger margins on International Priority packages and continued structural savings from the transformation program. Conversely, negative impacts came primarily from global trade policy, higher labor costs and increased external freight costs.

From a segmental perspective, two dynamics were clearly separated. The Core Express and Parcel business benefited from network optimisation and higher revenue per shipment, while FedEx Freight experienced a decline in operating profit due to weaker volumes and one-off costs related to spin-off preparations. However, these costs of USD 152 million are seen by the market as transitory and not structurally detrimental to the group's long-term potential.

Management commentary

In his comments, CEO Raj Subramaniam stressed that the second quarter confirms the workability of the chosen strategy. He believes that FedEx can simultaneously grow, improve efficiency and invest in the long-term transformation of the network, even in an environment of increased volatility. Particularly significant is the ability to improve revenue per shipment without aggressively increasing volumes, which signals a qualitative shift in the business.

At the same time, management openly acknowledges that the environment remains challenging in the short term. Wage pressures, the impact of regulatory changes and uncertainty in international trade will persist in the quarters ahead. That is why management believes it is critical to complete the separation of FedEx Freight and allow both companies to independently optimize their capital structure and strategic priorities.

Outlook

After a strong second quarter, FedEx raised its full-year outlook for fiscal 2026. It now expects revenue growth of 5-6% year-over-year, up from its previous range of 4-6%. Adjusted earnings per share before accounting adjustments for pension plans was raised to $14.80-16.00, while after adjusting for costs related to the Freight spin-off and other one-time items, the firm now targets $17.80-19.00.

At the same time, FedEx lowered its expected pension contributions to $275 million and reaffirmed a $4.5 billion capital spending plan, with an emphasis on automation, fleet upgrades and network efficiency improvements. A key structural highlight of the outlook remains the FedEx Freight separation, which is scheduled to be completed on 1 June 2026 and is set to fundamentally change the profile of the Group.

Long-term results

Looking at a longer time series, it is clear that FedEx is going through a period of stabilisation after several years of pressure on revenues. Total annual revenues have been in the range of US$87-93 billion for the past four years, with fiscal 2025 delivering modest growth to US$87.9 billion. However, the cost structure has improved significantly, particularly at the cost of revenue level, which has fallen by almost 6% year-on-year.

Gross profit grew by more than 22% in 2025, confirming that network transformation and a better service mix are starting to work. Operating profit may have declined year-on-year, but the long-term trend points to stable EBIT in the USD 5-6 billion range. Also important is the systematic decline in the number of shares outstanding, which supports earnings per share growth even in an environment of stagnant revenues.

Shareholder structure

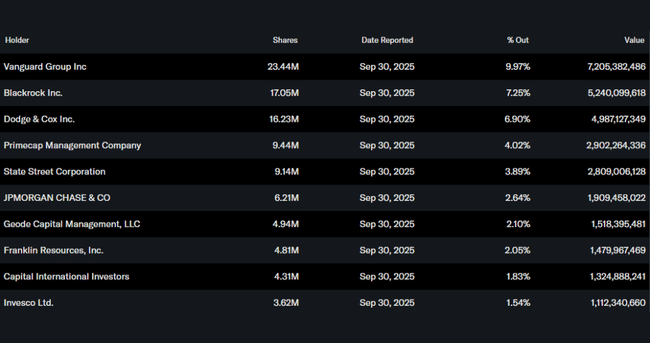

FedEx has a very strong institutional base, with more than 80% of its shares held by institutional investors. The largest shareholders are Vanguard, BlackRock and Dodge & Cox, signaling the long-term confidence of traditional asset managers in the company's transformational story. The relatively high insider stake also suggests an alignment of management interests with shareholders.

Analyst expectations

Analysts currently agree that the key catalyst for FedEx stock in 2026 will not be volume growth alone, but the completion of the FedEx Freight separation and visible margin improvement in the core package business. A number of investment houses expect that post-spin-off, the market will start to view FedEx as an "asset-light" logistics platform with higher returns on capital, rather than a conglomerate with a heavy capital profile.

In the short term, analysts expect results to fluctuate depending on the global business environment, but over the medium term, operating margins are expected to gradually return towards higher single digits. This could mean a significant increase in free cash flow with stable sales, creating room for further share buybacks and an attractive return for shareholders.