The consumer sector is one of the most sensitive segments to changes in consumer behaviour, pricing pressures and brand investments. After several years of heightened uncertainty associated with pandemics, commodity price volatility and increased competition, many large food companies are struggling to balance long-term growth strategies with short-term performance.

General Mills is one of those companies investing in its future growth, even if it means accepting pressures on profitability in the short term. These investments are focused on restoring organic growth, product innovation, and solidifying distribution channels, which are key to long-term competitiveness and margins in the packaged goods segment today.

How was the last quarter?

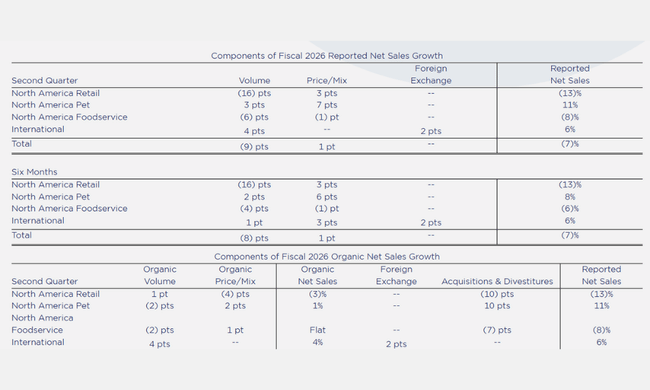

In the second fiscal quarter of 2026, net sales $GIS were $4.9 billion, down 7% year-over-year. However, it remains important to distinguish between organic sales and overall numbers impacted by structural changes in the portfolio: net organic sales were only 1% lower, reflecting actual market demand excluding the effects of divestitures and acquisitions.

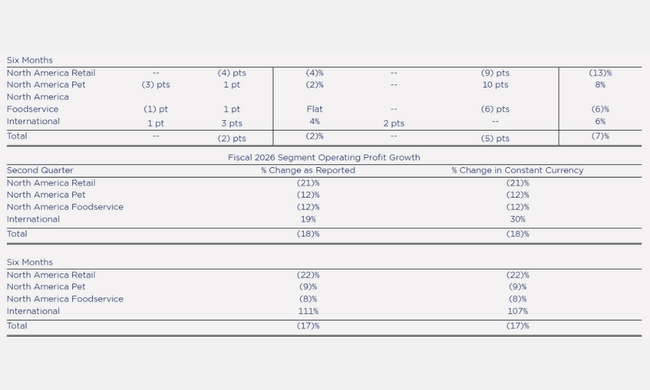

Profitability faced significant pressure. Gross margin decreased by 210 basis points to 34.8% of sales, impacted by higher input costs and the adverse effects of market changes. Operating profit fell 32% to USD 728 million and operating margin fell 560 bps to 15.0%. Even after adjusting for one-off items (e.g. restructuring costs), adjusted earnings remained lower, with adjusted operating profit down 20% to USD 848 million and operating margin down to 17.4%.

Net profit was $413 million, down 48%, and earnings per share fell 45% to $0.78. Adjusted for one-time items, adjusted EPS declined 21% to $1.10. This decline was the result of lower operating performance, lower joint venture income and a higher effective tax rate, partially offset by fewer shares outstanding.

Management commentary

CEO Jeff Harmening commented that the team continued to execute its growth strategy well in a challenging environment, particularly through its investment in the "remarkability framework" - a comprehensive initiative aimed at restoring organic growth through product innovation, stronger marketing and omnichannel distribution. Management also confirmed that the investments have begun to positively translate into revenue recovery in certain categories, particularly in the North American retail channels.

Harmening also highlighted that the firm is reaffirming its full-year guidance for FY2026, which implies confidence in the strength of the strategy despite short-term declines in profitability. This stance is in line with the company's ambition to prioritise long-term performance and market positioning over short-term financial results.

Outlook

The company expects the transitional investment phase to end and the price/mix ratio to improve due to stronger performance in the second half of the year and the following fiscal. This should support improved margins and net income without the need to raise price levels above a sustainable level for consumers.

Long-term results

A longer-term view shows that General Mills is on a relatively stable, albeit slightly downward, sales trajectory. Total sales for 2025 are approximately $19.49 billion, down nearly 2% from 2024. This decline is not dramatic and is within the expected fluctuations of the packaged goods segment, which traditionally responds to changes in raw material prices, consumer behavior, and competition.

The company's gross profit declined nearly 3% over the same period, driven by higher input costs as well as changes in product mix. Operating profit fell by around 4% and net profit fell by more than 8%. Earnings per share (EPS) fell by more than 5%, partly reflecting the investment strategy and portfolio changes within the divestments.

But over the long term, the company continues to generate stable cash flow and maintain a relatively strong balance sheet. EBITDA and EBIT show minor fluctuations and indicate that despite short-term fluctuations, the business remains able to fund investments, dividends and potential share buybacks.

Shareholding structure

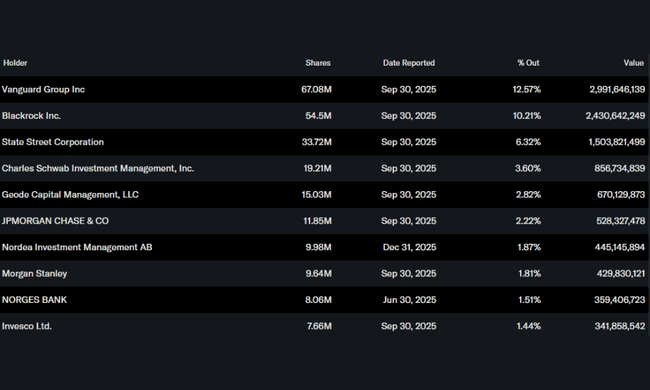

General Mills has a strong institutional investor base. Roughly 86% of all shares are held by institutions, with the largest stakes held by Vanguard (12.57%), BlackRock (10.21%), State Street (6.32%) and Charles Schwab Investment Management (3.60%).

This institutional concentration of ownership often means that investors evaluate a company more through the lens of long-term stability than short-term fluctuations, and prefer a strategy that can deliver stable returns and protection against cyclical fluctuations in the future.

Analyst expectations

Analysts approach Nike with cautious optimism, with consensus for FY2026 indicating that the market expects a gradual improvement in organic revenue growth and stabilization of margins as investments in the brand begin to generate results. Many ratings remain at Buy/Overweight, with average target prices above the market, indicating that the market still believes in medium-term growth. However, some analysts warn that without a clear acceleration in growth in key segments, sentiment may be cautious, especially if global economic uncertainty persists.