Citigroup closed 2025 still facing investor skepticism. Despite years of restructuring, asset sales, and simplification, returns on equity lagged peers, leaving the stock framed as a turnaround story rather than a performance compounder.

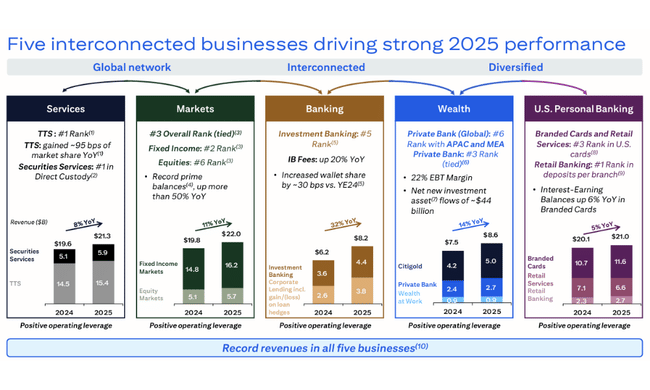

The fourth quarter begins to change that framing. Growth across Services, Markets, Banking, and Wealth suggests the core engine is strengthening, even as headline results remain distorted by one-off items. Combined with a $17.6 billion capital return, the message is that Citi is moving closer to a phase where execution—not restructuring—defines the investment case.

How was the last quarter?

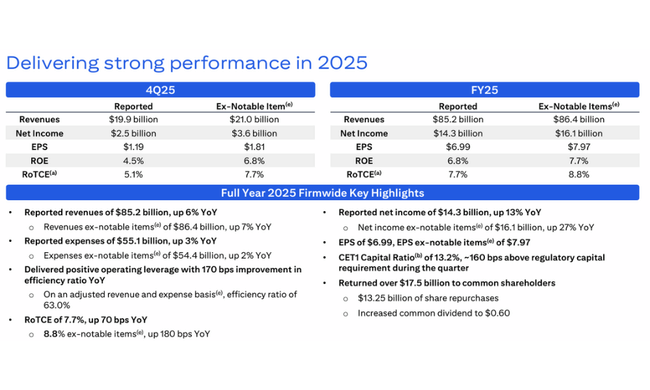

Citigroup $C posted net income of $2.5 billion in the fourth quarter of 2025, equivalent to earnings per share of $1.19. On the face of it, this is a year-over-year decline from $2.9 billion in the same period of 2024, but the key is the adjustment for a significant one-time item related to the planned sale of Citibank's Russian AO. Excluding this item, net income was $3.6 billion and adjusted EPS was $1.81, which significantly changes the interpretation of the results.

Revenue was $19.9 billion, up 2% year-over-year, but adjusted for the Russian item, revenue grew 8%. The Banking, Services, U.S. Personal Banking and Wealth segments were the main drivers. Net interest income grew 14% year-on-year, while non-interest income on a reported basis declined significantly due to one-off effects. Operating expenses increased 6% to $13.8 billion, primarily due to higher personnel costs, technology investments and legal expenses, which continue to pressure efficiency.

The provision for credit losses was $2.2 billion, down year-on-year. Net credit losses were lower, particularly in the U.S. Personal Banking segment, indicating stabilization in the consumer portfolio. The loan book as a whole grew, with average loans reaching $737 billion, while average deposits increased 8% year-over-year to about $1.4 trillion.

CEO commentary

CEO Jane Fraser described 2025 as a period of "significant progress" and highlighted that all major business lines achieved record revenues and positive operating leverage. Her comments indicate that management views 2025 as a transition phase in which the results of long-term investments are beginning to materialise.

Fraser also highlighted the return of capital to shareholders, which reached $17.6 billion in 2025, of which approximately $13 billion was in the form of share buybacks. This move is key to restoring investor confidence as it signals that the bank is no longer in purely defensive mode and can combine transformation with capital distribution.

Outlook

Citigroup enters 2026 with a clearly articulated goal of achieving a return on tangible common equity (RoTCE) of 10-11%. This would represent a significant improvement on the 8.8% achieved in 2025, adjusted for one-off items. Management expects Services and Markets to be the main drivers of growth, benefiting from a global client base and higher transaction activity.

At the same time, the outlook remains contingent on the ability to keep costs under control and further simplify the bank's structure. Citigroup still has lower efficiency than its main competitors, and it is operating leverage that will be the deciding factor in whether the targets can be achieved.

Long-term results

A long-term view of Citigroup's performance shows a bank that has gone through a significantly volatile period. Total revenues have grown from just under $80 billion in 2021 to over $170 billion in 2024, with the biggest jump coming in 2022 as interest rates rise. Since then, there has been a noticeable effort to stabilize the revenue base and reduce reliance on cyclical factors.

However, operating profit has been at much lower levels in recent years than before the pandemic. While it was nearly $27.5 billion in 2021, it declined significantly in 2022 and 2023 and only started to pick up towards $17 billion in 2024. Net profit shows a similar picture - after falling in the restructuring years, it is up more than 37% year-on-year in 2024, but still remains below historical highs.

A positive element of the long-term trend is the systematic reduction in the number of shares outstanding, which helps stabilize earnings per share even in periods of weaker profitability. At the same time, tangible book value per share is increasing, reaching $97.06 at the end of 2025. Thus, over the long term, Citigroup is showing improving capital discipline, although operating performance has not yet fully caught up with its major U.S. peers.

Shareholder structure

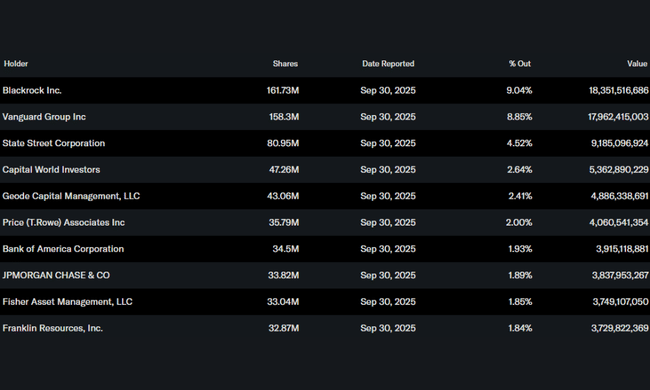

Citigroup's shareholder structure is heavily institutional, with more than 80% of shares held by institutional investors. The largest are BlackRock, Vanguard and State Street. The low proportion of insiders suggests a management-driven model rather than a founder-driven structure, which is typical for a global banking group of this type.

Analyst expectations

The analyst consensus views Citigroup as a title with high potential but also with elevated risk. The key factor remains the ability to meet 2026 ROE targets. If the bank manages to approach the 10-11% RoTCE threshold, valuation may be revised towards book value.

On the other hand, analysts caution that any slowdown in the global economy, rising credit losses or other one-off costs could slow this process significantly. Thus, Citigroup remains primarily betting on the successful completion of the transformation.