By the end of 2025, TSMC was no longer merely riding a cyclical recovery in semiconductors. The company has become a strategic choke point for global computing power, where advanced manufacturing, geopolitical priorities, and technological sovereignty increasingly intersect. That context elevates each earnings report beyond standard quarterly performance.

The fourth quarter underscored more than volume growth. It tested TSMC’s ability to translate leadership in advanced nodes into superior margins and earnings quality. Investors focused not only on growth rates, but on revenue mix, profitability, and early signals for 2026—key indicators of how durable this advantage may be.

What was the last quarter like?

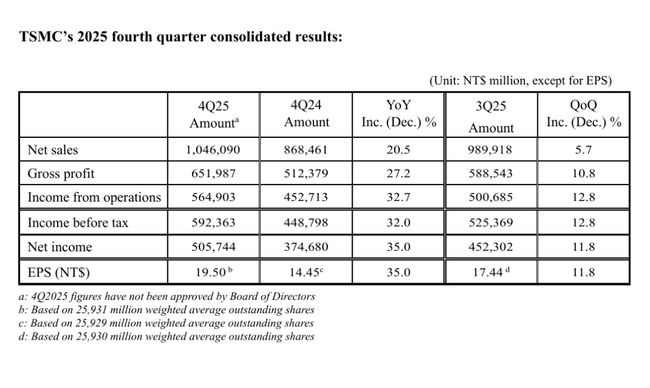

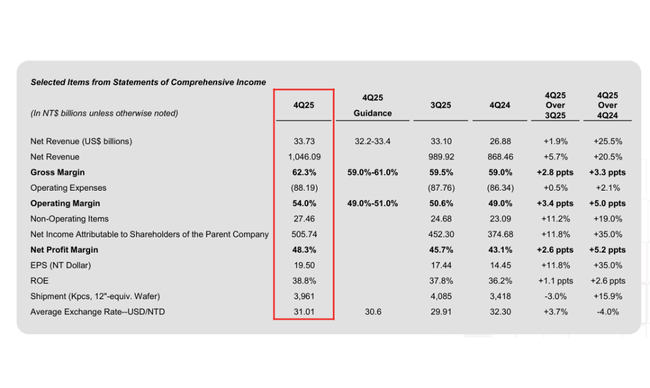

TSMC $TSM reported consolidated revenue of 1.046 billion Taiwan dollars in the fourth quarter of 2025, representing a year-on-year growth of 20.5% and a quarter-on-quarter improvement of 5.7%. The significant acceleration was mainly driven by continued strong demand for the most advanced manufacturing nodes, particularly from customers focused on AI accelerators, data centers and high-end mobile chips. In dollar terms, sales reached $33.7 billion, confirming that growth was not simply a currency effect, but a reflection of real volume expansion and pricing power.

The company's profitability reached an extraordinary level at the end of the year. Net profit rose 35% year-on-year to TWD 505.7 billion, with earnings per share reaching TWD 19.50. Gross margin moved to 62.3%, operating margin to 54.0% and net margin to 48.3%, clearly showing that TSMC can grow not only in volume but also with very high operating efficiency. Such high margins are rather exceptional in the capital-intensive semiconductor industry and confirm the company's structural advantage.

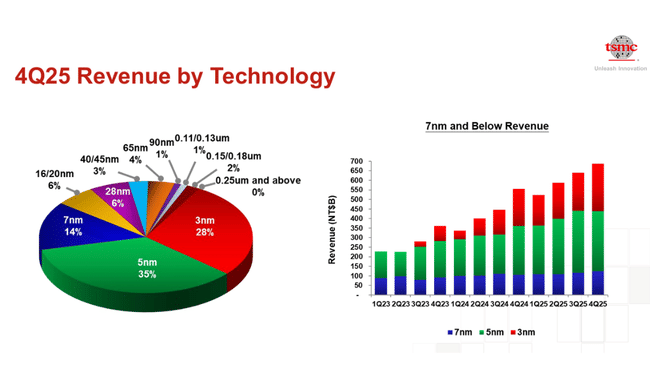

The technology mix of revenues was also an important element of the results. Three-nanometer processes already accounted for 28% of total wafer revenues, five nanometers accounted for 35% and seven nanometers 14%. Overall, advanced technologies defined as 7 nm and better accounted for 77% of wafer revenues. This means that TSMC is increasingly exiting lower-margin legacy nodes and moving towards high-value orders where it has a virtually unassailable position.

Management commentary

In his comments, CFO Wendell Huang highlighted that the fourth quarter performance was clearly underpinned by strong demand for the most advanced manufacturing technologies. He also confirmed that this trend is expected to continue into early 2026. Management is implicitly suggesting that the current demand is not a short-term blip, but part of a broader structural shift towards compute-intensive applications.

Management also pointed to the high visibility of lead-edge process orders, which puts the firm in a relatively comfortable position for production and capital expenditure planning. This is particularly key in an environment where most competitors are still struggling with the return on investment in the latest technologies.

Outlook

For the first quarter of 2026, TSMC expects revenue in the range of $34.6 billion to $35.8 billion, which would represent further quarter-on-quarter growth. Gross margin is expected to be between 63% and 65% and operating margin between 54% and 56%, levels that confirm continued operating leverage. These projections suggest that the company enters the new year with very strong momentum.

At the same time, management announced a 2026 capital budget of $52 billion to $56 billion. This confirms an aggressive investment strategy focused on expanding capacity at the most advanced nodes, but also suggests that TSMC is confident of recouping these investments through long-term contracts with strategic customers.

Long-term results

A look at the long-term trend shows that 2024 represented a turning point for TSMC. Total sales grew nearly 34% year-on-year to 2.89 trillion Taiwan dollars, while net profit increased 36% to 1.16 trillion. This growth followed a weaker 2023, when the company faced a temporary cooling in demand, and confirmed TSMC's ability to adapt quickly to changes in the cycle.

More importantly, the development of operating profitability. Operating profit grew by more than 43% and EBITDA by more than 30% in 2024, showing that revenue growth was not offset by a disproportionate increase in costs. The cost base did grow, but at a significantly slower rate than revenue, confirming strong operational discipline and efficient use of capital.

Over the long term, it is evident that TSMC has been able to maintain a stable number of shares outstanding, which means that earnings per share growth is driven primarily by actual improvements in performance, not financial adjustments. This factor is crucial for long-term investors as it increases confidence in the quality of reported results.

News

The most significant event of the quarter was the further strengthening of the share of three-nanometer production, which is becoming the main driver of margins. At the same time, the company continues to prepare for the next generation of manufacturing processes, which should maintain its technological edge in the coming years. The 2026 capital budget indicates that capacity expansion remains a key strategic priority.

Shareholding structure

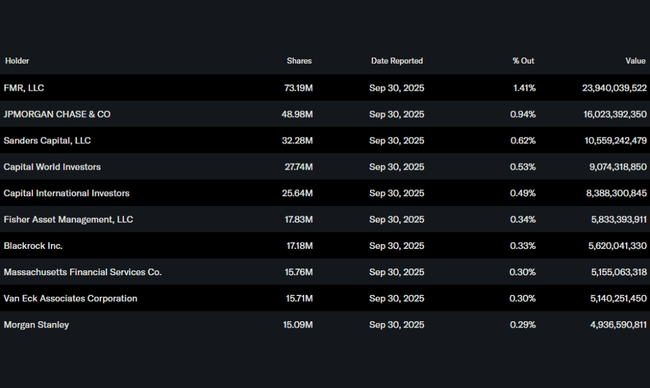

TSMC's shareholding structure remains stable and relatively conservative. Institutional investors hold approximately 16% of the shares, with FMR, JPMorgan Chase and Capital World Investors among the largest. The low share of insiders underscores the firm's character as a widely held global leader whose stock serves as long-term exposure to a technology megatrend rather than a speculative title.

Analyst expectations

The analyst consensus is shifting towards continued growth in 2026 following the results, with the combination of strong demand for AI chips, high order visibility and TSMC's ability to maintain margins at historically high levels being key drivers. At the same time, analysts point out that it is the technological dominance in 3nm and future 2nm processes that creates a barrier to entry that competitors are struggling to catch up to.

Part of the market, however, remains cautious due to high capital expenditure and geopolitical risks. Still, the prevailing view is that TSMC remains a key "must have" title for investors who want long-term exposure to the growth of computing power and artificial intelligence.