For much of the past decade, Wells Fargo has been viewed as a bank in recovery rather than expansion. Regulatory constraints, balance-sheet conservatism, and internal remediation dominated the narrative, leaving little room for growth ambitions in the eyes of investors.

That narrative is now evolving. With key restrictions lifted and governance normalized, the bank is gradually shifting from fixing legacy issues to actively deploying capital. The fourth quarter of 2025 should therefore be read less as a standalone earnings report and more as confirmation that Wells Fargo is re-entering the cycle as a fully functioning growth-oriented institution.

How was the last quarter?

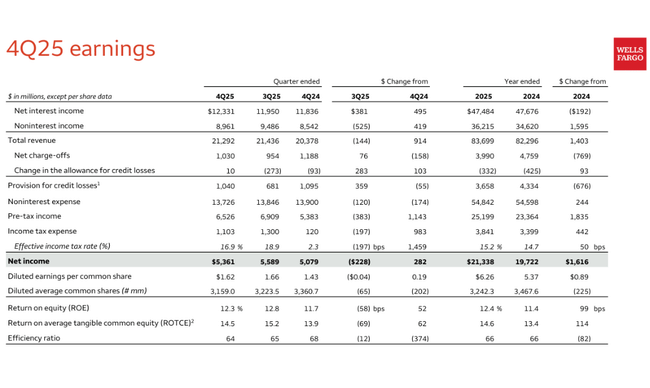

Wells Fargo $WFC reported net income of $5.4 billion for the fourth quarter of 2025, which equates to earnings per share of $1.62. This is a year-over-year improvement from $5.1 billion and $1.43 per share in Q4 2024. Adjusted for a one-time severance item of $612 million, earnings would have been $5.8 billion and $1.76 per share, respectively, confirming the bank's solid operating performance.

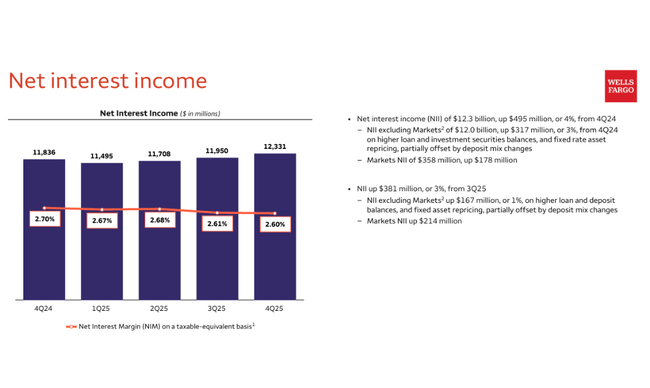

Total revenues increased 4% year-on-year to USD 21.3 billion. Net interest income reached USD 12.3 billion, up 4% year-on-year, mainly due to loan growth, improved trading performance and the revaluation of fixed interest assets. Non-interest income increased 5%, with positive contributions primarily from higher asset management fees, card fees and mortgage banking income. In contrast, venture capital and investment results were weaker than in the previous year.

On the cost side, discipline is evident. Non-interest expenses declined 1% year-on-year to $13.7 billion, reflecting lower regulatory costs and ongoing efficiency measures. The bank's efficiency ratio improved, with the efficiency ratio falling to 64% from 68% in Q4 2024. The provision for loan losses was $1.04 billion, slightly lower than a year ago, with the quality of the loan portfolio remaining stable.

The bank's balance sheet also confirms a return to growth. Average lending reached USD 956 billion, up 5% year-on-year. Deposits rose to USD 1.38 trillion, up 2% year-on-year. CET1's capital adequacy ratio reached 10.6%, which, while a slight decline from the previous year, still provides ample scope for returning capital to shareholders.

CEO commentary

CEO Charlie Scharf called 2025 a watershed year, largely due to the Fed's removal of the long-term cap on balance sheet size and the completion of several key regulatory actions. He said that Wells Fargo has managed to achieve its ROTCE target return on tangible equity of 15% and the bank has now set a more ambitious medium-term target of 17-18%.

Scharf highlighted that year-on-year earnings per share grew 17%, fee income grew 5% and net loan losses fell 16%. At the same time, the bank returned $23 billion to shareholders in 2025, including $18 billion in buybacks, and increased the dividend by 13%. Management said it was able to fund significant infrastructure investment and growth by reducing its cost base over the long term, which has fallen by $15 billion cumulatively over the past five years.

Outlook

The outlook to 2026 is openly growth-oriented for the first time in a long time. Bank management expects that the removal of regulatory restrictions will enable more dynamic credit expansion, particularly in commercial and investment banking. Growth is also expected to continue in consumer lending, where higher credit card activity and a return to growth in auto financing are positive signs.

At the same time, the Bank expects further efficiency improvements, although the pace of cost reduction will not be as strong as in previous years. A key objective remains to move ROE towards the levels of the largest US banks, with management openly communicating an ambition to get to a ROTCE in the 17-18% range within a few years.

Long-term results

The long-term numbers show that Wells Fargo has had a very volatile period, but one from which it is gradually stabilizing. Total revenue in 2024 is $125.4 billion, up 8.7% year-over-year. A year earlier, they grew by as much as 38%, but this was partly driven by one-off factors and the return of interest margins after a sharp rise in rates.

Operating profit in 2024 was $23.4 billion, up 8% year-on-year, while net profit reached $19.7 billion. Profitability is therefore improving more slowly than revenues, reflecting both cost pressures and conservative provisioning. Still, there is a clear trend towards normalisation - after a significant fall in 2022, EPS has gradually returned to US$5.43 in 2024, up from US$3.17 in 2022.

An important structural factor is the long-term reduction in share count. The average number of shares has fallen from over 4 billion in 2021 to around 3.43 billion in 2024, significantly supporting earnings per share growth and return on capital. EBITDA is nearly $31 billion in 2024, confirming the bank's solid ability to generate cash even in more challenging periods.

Shareholding structure

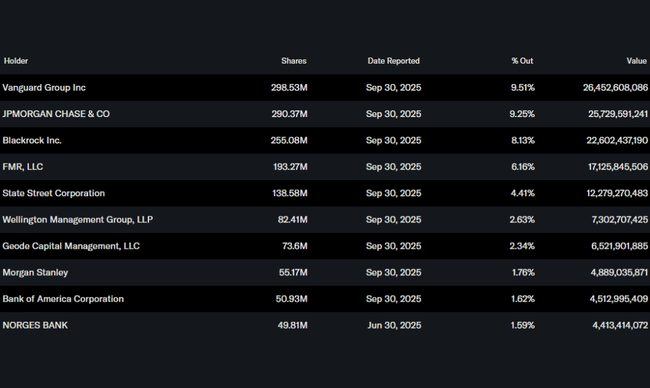

Wells Fargo's shareholder structure remains highly institutional. Approximately 79% of shares are held by institutional investors, while the share of insiders is negligible. The largest shareholder is Vanguard Group with 9.5%, followed by JPMorgan Chase with 9.3% and BlackRock with 8.1%. Fidelity also holds a significant stake through FMR. This structure confirms that the title is seen as a long-term position for large institutional investors rather than a speculative bet.

Analyst expectations

Analysts agree that 2026 should be the first full year of growth for Wells Fargo after a long period of retrenchment. Earnings per share growth is expected to continue, driven by a combination of credit expansion, stable interest margins and aggressive share buybacks. The consensus expects further improvement in return on capital and a gradual convergence to the performance of the largest US banks.

Analysts' price targets are currently mostly above current market prices, with more optimistic scenarios assuming that the market will begin to value Wells Fargo as a growth bank rather than a restructuring story. The macroeconomic slowdown and credit quality developments remain key risks, but the baseline scenario assumes a relatively stable environment and continued improvement in fundamentals.