Netflix entered the final quarter of 2025 in excellent operating shape. Subscriber growth, steady price increases, and a rapidly scaling ad-supported tier have reshaped the business into a more diversified and cash-generative platform. From a fundamentals perspective, margins and free cash flow were firmly under control.

The market reaction tells a different story. Investors looked past the quarterly beat and focused on strategy—specifically the proposed acquisition of Warner Bros. Discovery. The sell-off reflects concern that a bold strategic pivot could dilute execution quality and introduce balance-sheet risk at a time when Netflix’s standalone model was already delivering.

How was the last quarter?

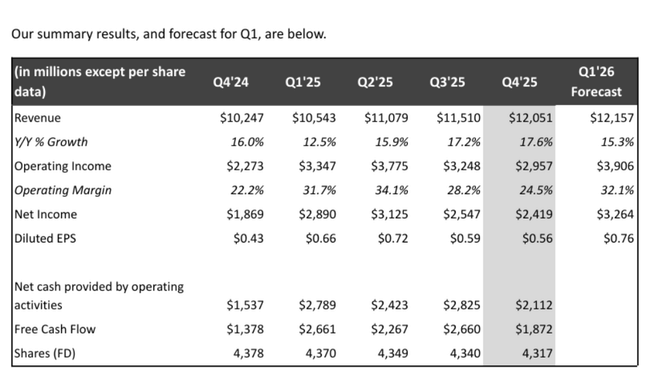

The fourth quarter of 2025 confirmed that Netflix's core $NFLX business remains in very good shape. Revenue grew 18% year-over-year to $12.1 billion, which was slightly above the company's original guidance. The main driver was the combined effect of growth in paid memberships, pricing adjustments in key regions and rapidly growing advertising revenue. Netflix broke through the 325 million paid accounts mark during the quarter, confirming its global scale as well as its still-solid acquisition capability.

Operating profit in the fourth quarter was approximately $3.25 billion, up 30% year-over-year. The operating margin moved to around 25%, higher than the company itself had originally anticipated. Net income was about $2.4 billion and diluted earnings per share were $0.56, up over 30% year-over-year. Operating cash flow was also a positive surprise, with free cash flow for the quarter reaching nearly $1.9 billion.

In the second half of 2025, while total hours watched grew just 2%, viewership of owned original titles grew 9%. This confirms that Netflix is still able to create content that generates a deeper user relationship with the platform and has higher long-term value than the licensed catalog.

Full Year 2025 Results

Full year numbers show a very consistent picture. Revenues for 2025 reached $45.2 billion, representing year-over-year growth of 16% and 17%, respectively, when adjusted for currency effects. Operating margin rose to 29.5%, up nearly three percentage points from 2024. Netflix has thus clearly confirmed that it can combine growth with profitability expansion.

The development of the advertising segment was a significant positive. Advertising revenues grew more than 2.5-fold and exceeded $1.5 billion. While still a smaller portion of total revenues, the momentum of this segment is critical to the long-term investment story as it allows for further monetization of the user base without the need for aggressive price increases.

For the full year, Netflix generated free cash flow of $9.5 billion, a significant year-over-year increase. The company also continued to repurchase its own shares, buying back $2.1 billion worth of stock in the fourth quarter alone.

Outlook for 2026

The outlook for 2026 remains very solid in terms of operating metrics. Management expects revenue in the range of $50.7 billion to $51.7 billion, implying year-over-year growth of 12% to 14%. Operating margin should further increase to approximately 31.5%, despite the inclusion of approximately $275 million of acquisition-related costs associated with Warner Bros.

The advertising business is expected to roughly double revenues in 2026, making it one of the fastest growing segments of the entire company. Free cash flow should approach the $11 billion mark, confirming Netflix's strong ability to fund both content investments and potential strategic acquisitions.

The acquisition of Warner Bros. Discovery - a key turning point

This is where we get to the main reason for the negative market reaction. Netflix announced that the acquisition of Warner Bros. Discovery will be executed as an all-cash transaction with a price of $27.75 per WBD share. The overall size of the transaction is extraordinary and requires massive financing, including bridge loans of over $40 billion.

From a strategy perspective, the merger makes sense - Netflix would acquire a vast catalog of IP, movie and series studios, and HBO Max as a strong brand. But from an investor perspective, there is a growing risk of debt, short-term cash flow pressure and potential deterioration in capital discipline. Thus, at any given time, the market has begun to discount risk more than it has priced in the strategic potential itself.

Long-term results: model change over time

Looking at the last four years, Netflix's evolution has been markedly uneven but strategically very consistent. Between 2021 and 2024, revenues grew from approximately $29.7 billion to nearly $39 billion. However, the key difference between the years was not growth per se, but profitability.

2022 was a weaker period, with growth slowing and operating profit declining due to heavy investment in content and pressure on margins. In 2023, the company stabilized, but it was not until 2024 that the company made a significant breakthrough - operating profit grew by more than 20% and net profit increased by around 60%. Then in 2025, Netflix accelerated the trend further, with operating profit up nearly 50% and net profit up more than 60%.

A fundamental change is the revenue structure. Netflix has shifted from a "growth at any cost" model to a highly profitable media platform that can generate stable and growing cash flow. It is this change that makes the market today more sensitive to any decision that could disrupt this discipline - including large acquisitions.

Shareholder structure

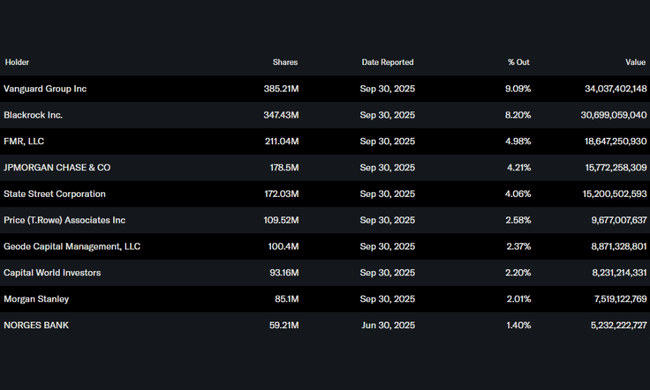

Netflix's shareholder structure remains distinctly institutional. Approximately 80% of the shares are held by institutional investors, which increases the sensitivity of the share price to changes in the firm's strategy and risk profile. The largest shareholders are Vanguard, BlackRock, Fidelity, JPMorgan, and State Street, long-term oriented investors that emphasize capital discipline and return on investment.

Analyst expectations

The analyst consensus shifted to a more cautious plane following the results. While most analysts are positive on operating performance, margin expansion and cash flow strength, they caution about the increased financial risk associated with the Warner Bros. acquisition. Target prices have begun to diverge more widely, with more optimistic scenarios working with significant long-term synergies from the acquisition, but more conservative analysts discounting higher debt and integration uncertainty.