Johnson & Johnson entered the final quarter of 2025 as one of the healthcare sector’s most dependable defensive names. A balanced mix of innovative medicines and MedTech, combined with conservative financial management, set expectations for a steady, uneventful close to the year.

That same stability, however, raises the bar. The fourth-quarter results did not point to any fundamental deterioration, but higher costs, margin pressure, and one-off effects shifted investor attention away from the headline outlook. The market reaction reflects not fear of a broken business, but heightened sensitivity to risks that could temper performance in 2026.

How was the last quarter?

In the fourth quarter of 2025, Johnson & Johnson $JNJ continued its solid operating performance across segments, but results were impacted by several external and internal factors. Management has previously noted the fading effects of the return of rights to SIMPONI, SIMPONI ARIA and REMICADE, which were fully realized in the fourth quarter of 2024, but the comparative base remains challenging.

The macroeconomic environment remained mixed. Higher interest rates increased the cost of funding short-term debt instruments, while the benefit from higher interest income on cash was not sufficient to fully offset them. Customs duties also remain a significant factor, where the company has previously indicated a negative impact of approximately $200 million per year, solely within the MedTech segment. This pressure is further reflected in the cost structure in the results.

Johnson & Johnson | Q4 2025 - key numbers

Revenue: $24.6 billion (above expectations; consensus ~$24.16 billion; +9% YoY)

Adjusted EPS: $2.46 (in line with expectations; not beating consensus)

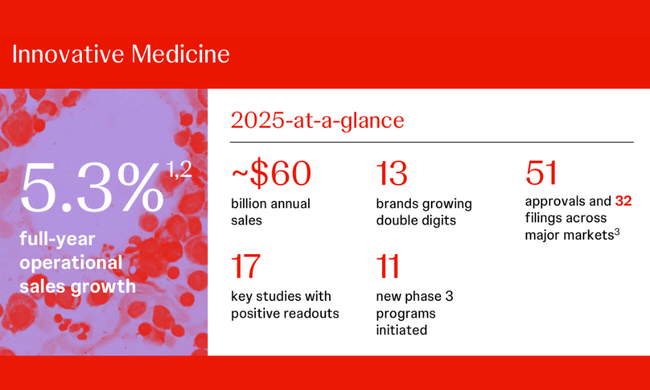

Innovative Medicine: $15.8 billion (above expectations; consensus estimate ~$15.45 billion; YoY ~+6%)

MedTech: $8.8 billion (above expectations; estimate ~$8.67 billion; YoY ~+6%)

Outlook

Johnson & Johnson unveiled a 2026 outlook that, on the face of it, is significantly better than what Wall Street was counting on. Management expects operating sales in the range of $99.5 billion to $100.5 billion, above market consensus, and adjusted earnings per share of $11.43 to $11.63, in line with most analysts' expectations. This is all the more significant as the company has already factored into its forecast the negative impact of hundreds of millions of dollars arising from the deal it struck with the Donald Trump administration to lower US drug prices in exchange for tariff exemptions.

Still, the stock weakened after the results. Indeed, the market did not just focus on the outlook numbers themselves, but also on several risks that remain in play. The biggest attention was drawn by another significant drop in sales of the key drug Stelara, which fell more than analysts expected, due to the emergence of biosimilar competition. While management emphasizes that the rest of the pharmaceutical portfolio is growing at double-digit rates and can more than offset this shortfall, investors view the accelerating erosion of Stelara as a structural change that increases pressure to maintain growth rates in the years ahead.

Management Commentary

During the quarter, management repeatedly emphasized that the company's core strategy remains unchanged - a focus on innovation, disciplined capital allocation and sustainable growth. At the same time, management acknowledged that 2026 will be a transition period, particularly due to a combination of higher investment, regulatory processes and acquisition costs.

There was also a clear message that short-term margin pressures are not structural in nature, but a combination of temporary factors - from tariffs to higher clinical development costs to one-off impacts related to M&A activity. Yet it was this uncertainty about the pace of cost base normalisation that was perceived negatively by the market.

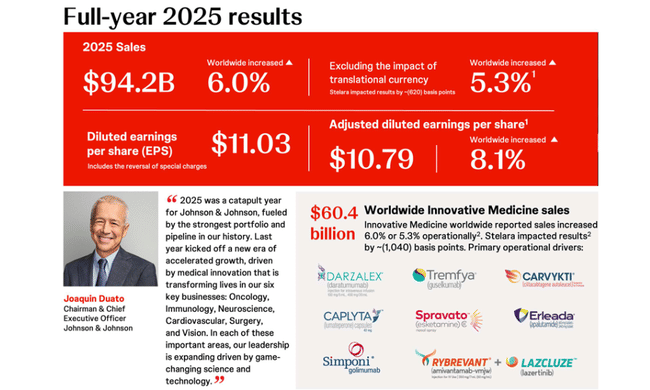

CEO Joaquín Duato described 2025 as a watershed year, likening it to a "catapult" that would propel Johnson & Johnson into a new phase of accelerated growth. This shift, he said, is being driven by the strongest portfolio and research pipeline in the company's history and, above all, by medical innovations that are having a real impact on patients' lives. Duato emphasized that in all six of the company's core business areas - oncology, immunology, neuroscience, cardiovascular medicine, surgery and vision care - the company is strengthening its leadership position. This development, he said, is the result of breakthrough science and technology that is creating a solid foundation for continued growth in the years ahead.

Long-term results

Looking at the long-term trend, Johnson & Johnson remains a company with relatively stable revenues but a significantly fluctuating profit profile. Revenues grow from $78.7 billion in 2021 to $88.8 billion in 2024, representing cumulative growth but not an accelerating trend. Growth rates were mostly in the low single-digit percent range, with a peak in 2023.

Gross profit has been growing over the long term, but momentum is slowing. Gross margin has remained relatively stable, confirming the strength of the portfolio and pricing policy, but also suggesting limited scope for further expansion without structural changes. Operating costs have risen significantly, by more than 11% in 2024, leading to a year-on-year decline in operating profit of more than 5%. It is this mismatch between revenue growth and faster cost growth that is one of the main signals of concern to investors.

Net profit showed a significant decline in 2024, down almost 60% from an exceptionally strong 2023, driven by one-off factors. EPS is therefore fluctuating sharply, reducing the predictability of returns for shareholders. On the positive side, the number of shares outstanding has been declining over the long term, confirming the continued return of capital to shareholders and partially cushioning the impact of weaker profitability.

News and key themes of the quarter

Highlights included the acquisition of Halda Therapeutics. The transaction is strategically important in terms of the long-term pipeline, but in the short-term will deliver earnings dilution of approximately $0.15 per share in 2026. This information was one of the factors that investors factored in negatively after the results.

Regulatory and legal issues surrounding baby powder remain in the background, but continue to pose reputational and financial risk. In the area of innovative medicine, the company has presented a number of positive clinical data, but most of these have an impact in the medium term rather than immediately on results.

Shareholding structure

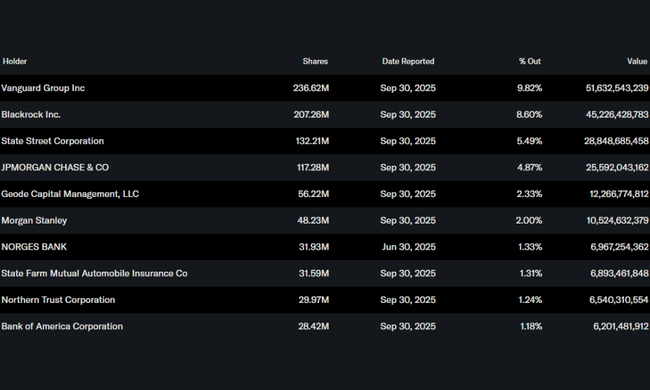

Johnson & Johnson's shareholder structure is a typical example of institutional stability. More than three-quarters of the shares are held by institutional investors, giving the company a conservative ownership base over the long term. The Vanguard Group and BlackRock play a dominant role, which reduces the risk of sudden capital swings but increases sensitivity to changes in index weights and macro sentiment.

Analyst expectations

Analysts have mostly made subtle adjustments to their outlooks following the results, rather than dramatic changes to their recommendations. Consensus continues to expect modest revenue growth in 2026, but with margin pressure and lower earnings per share growth. It was this shift in expectations - rather than the Q4 numbers themselves - that was the main reason for the stock's post-earnings decline.

Summary: why the stock fell

Johnson & Johnson stock fell after earnings not because of weak business, but because of a combination of higher costs, EPS dilution in 2026, uncertainty around the macro, and the lack of a clear catalyst for growth acceleration. For long-term investors, the title remains a stable pillar of the portfolio, but in the short term the market is making it clear that it expects more than just stability.

Other reasons for the decline:

Stelara (an immunologicalbiologic) is falling faster than expected

- and this is a structural problem, not a one-off thing.Legal risks (talc) came back on the table on the day of the results.

Regulatory and political uncertainty (pricing agreements, tariffs, margin pressure).

Stocks were relatively high ahead of results → typical "good news, sell the fact".