Procter & Gamble has long been treated as a benchmark for stability in global consumer staples. That status comes with a higher bar: investors expect predictability, margin discipline, and resilient cash generation across cycles. The second quarter of fiscal 2026 suggests those foundations remain intact—but also highlights where the model is being tested.

Revenue held up and guidance was reaffirmed, yet the quality of growth is shifting. Pricing continues to do the heavy lifting while volumes soften, signaling that FY2026 may be less about expansion and more about protecting profitability in an increasingly constrained environment.

How was the last quarter?

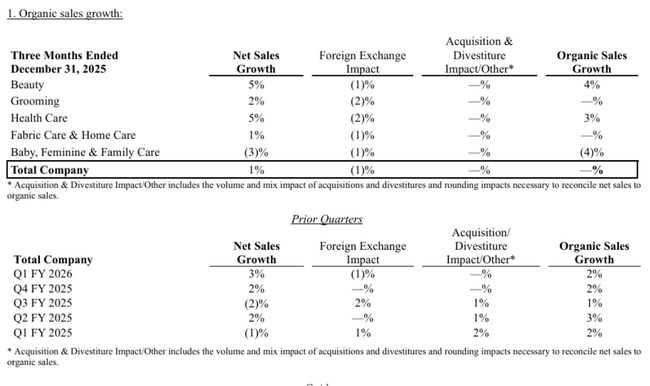

P&G $PG -reported sales of $22.2 billion in the second fiscal quarter of 2026, up 1% year-over-year. However, organic sales were flat - a 1% price increase was fully offset by a 1% decline in volumes, while product mix had a neutral impact. This is a key signal, as the company has for several years been primarily based on the pricing power of its brands rather than demand growth.

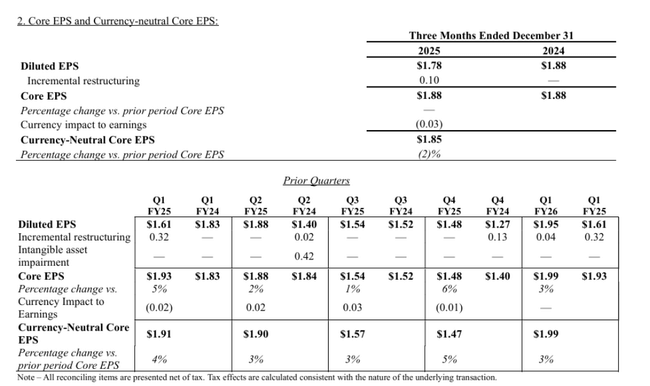

At the profitability level, cost pressures and restructuring were evident. GAAP EPS declined to $1.78, down 5% YoY, primarily due to higher restructuring costs. Core EPS was $1.88 and remained unchanged year-over-year, meaning that even after adjusting, the company failed to grow profitably. Currency-adjusted core EPS even fell 2% to $1.85.

Margins were the weakest point of the results. Reported gross margin was down 120 basis points, core gross margin was down 50 basis points and on a currency-neutral basis it was down 30 basis points. Productive savings delivered a positive effect of 160 bps and price increases of a further 50 bps, but these benefits were outweighed by negative factors: unfavourable mix (120 bps), higher product reinvestment (60 bps) and, most notably, tariff-related costs (60 bps). Operating margin fell even more significantly - reported 200bps and core 70bps.

From a cash flow perspective, P&G remains very strong. Operating cash flow was US$5.0bn, net income was US$4.3bn and adjusted free cash flow productivity was 88%. The company also returned US$4.8bn to shareholders, US$2.5bn of which was in the form of dividends and US$2.3bn through share buybacks, confirming that return of capital remains a pillar of the investment thesis.

CEO commentary

In his comments, CEO Shailesh Jejurikar highlighted that the results kept the company within full year guidance despite the challenging consumer and geopolitical environment. He also expressed confidence in improved results in the second half of the fiscal. This tone is typical of P&G - calm, defensive and focused on long-term stability. For investors, however, it is an implicit admission that the first half of 2026 is burdened with pressures that the company has not yet been able to fully offset.

Outlook

P&G kept its revenue outlook for fiscal 2026 unchanged. Total revenue is expected to grow 1% to 5%, with organic growth in the range of "in-line" to +4%. The change came at the GAAP earnings level: the firm lowered its expected GAAP EPS growth to 1% to 6% from the previous range of 3% to 9%, due to higher-than-expected restructuring charges. Core EPS guidance remains unchanged at $6.83 to $7.09, with a midpoint of $6.96, corresponding to roughly 2% growth.

Macro assumptions show why the market is reacting cautiously. P&G expects commodities to be roughly neutral for the full year, currency rates should deliver a positive impact of around $200m after tax, but tariffs represent a negative impact of around $400m after tax. The company expects a further roughly USD 250 million after-tax impact from the combined pressure of higher interest costs and the effective tax rate. The total negative impact of these factors is approximately $0.19 per share, which explains why sentiment remains restrained even with the maintenance of guidance.

Long-term results

A look at the trend of the last four fiscal years shows a company that has maintained stability but is gradually losing momentum. Revenues grew from $80.2 billion in fiscal 2022 to $84.3 billion in 2025, a cumulative growth of roughly 5% over three years. However, the pace of growth is slowing - while revenues grew by around 2-2.5% in 2022 and 2023, they will only grow by 0.3% in 2025.

Gross profit has been around $43 billion for a long time, with gross margin stagnating in the last year. On the positive side, the company was able to significantly reduce operating expenses in 2025 - operating expenses fell by 8%, which helped boost operating profit by more than 10% to USD 20.5bn. However, this effect is rather one-off and does not address the structural problem of low volume growth.

Net profit and EPS grew only moderately over the long term. Diluted EPS increased from USD 5.81 in 2022 to USD 6.51 in 2025, corresponding to an average annual growth of around 4%. Moreover, this growth was partly driven by changes in share count and financial optimisation, rather than a significant improvement in operating performance. EBITDA fell by more than 9% in 2025, a warning sign that the company's operating leverage is starting to work in the opposite direction.

News

The most notable news this quarter is an update to GAAP EPS guidance due to higher restructuring costs that the company now expects throughout fiscal 2026. Additionally, P&G explicitly quantified the impact of tariffs at approximately $400 million after-tax, a significant pressure on gross margins in particular. Continued strong cash returns to shareholders remain positive news, with the company planning to pay out approximately $10 billion in dividends and repurchase approximately $5 billion in stock in 2026.

Shareholder structure

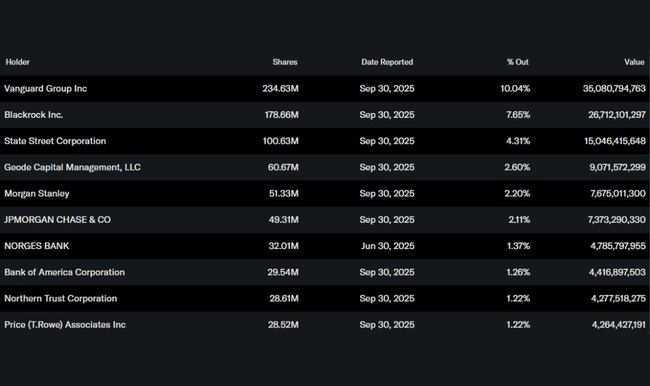

P&G's shareholder structure confirms its character as a typical institutional defensive. Approximately 70% of the shares are held by institutional investors, with Vanguard, BlackRock and State Street being the largest shareholders. This profile typically implies lower volatility, a high emphasis on dividend stability, and less tolerance for long-term deterioration in margins or growth trajectory. Insider ownership is minimal, further underscoring the institutional nature of the title.

Analyst expectations

The analyst consensus expects P&G to remain primarily a defensive title with low single-digit earnings growth in 2026. Maintaining core EPS guidance was received neutrally, while lowering GAAP EPS guidance due to restructuring and clearly naming the impact of tariffs contributed to a more cautious market tone. Analysts agree that the key theme for the next quarter will not be revenue growth, but the ability to stabilize margins and stem volume declines without further price increases.