Intel closed 2025 with results that avoided outright disappointment but failed to deliver the reassurance investors were looking for at this stage of the turnaround. Several key metrics came in better than feared, and management continues to emphasize progress on Intel 18A, manufacturing execution, and the expanding role of AI across the portfolio.

The sell-off tells a different story. The market reaction was not about the quarter itself, but about the path forward. A cautious outlook for early 2026, ongoing margin pressure, and continued GAAP losses reinforced the reality that Intel’s transformation is expensive, slow, and still fragile. The strategy may be credible—but patience is wearing thin.

How was the last quarter?

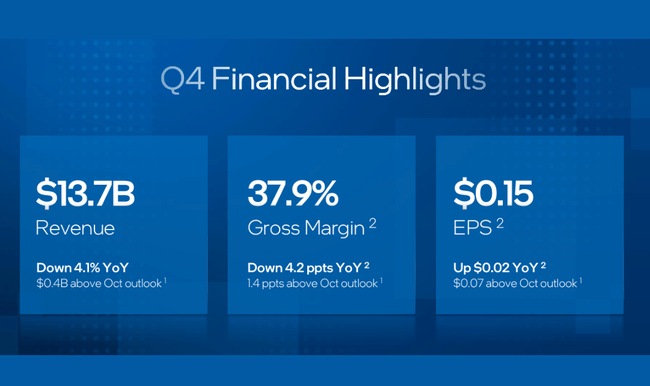

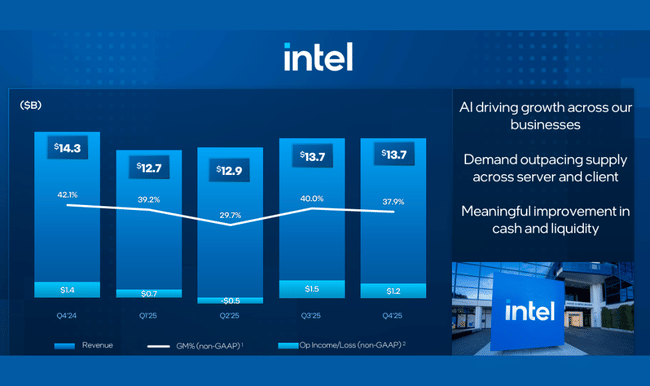

Intel $INTC ended 2025 with a quarter that looks like "stabilization after the storm" on a headline level, but beneath the surface you can see that the company is still teetering between restructuring, margin pressure, and transitioning to a new manufacturing and product cycle. In the fourth quarter, Intel posted revenue of $13.7 billion, down 4% year-over-year. But at the same time, management points out that internal expectations were better - according to CFO Zinsner, Intel beat its own expectations in revenue, gross margin and earnings per share, despite across-the-board outages and supply chain strains.

Profitability remains straddled between GAAP and adjusted numbers. GAAP EPS came in at $-0.12, while non-GAAP EPS came in at $-0.15, up 15% year-over-year on an adjusted basis from $-0.13. Non-GAAP net income attributable to Intel rose to $0.8 billion, up 35% year-over-year, but GAAP results were again a loss, with a net loss of $0.6 billion. Margin pressure was the key issue for the quarter: GAAP gross margin fell from 39.2% to 36.1%, non-GAAP even from 42.1% to 37.9%, a sharp drop of 4.2 percentage points. At the expense level, on the other hand, Intel continues to show discipline: R&D and MG&A fell 14% year-on-year to $4.4 billion (GAAP) and $4.0 billion (non-GAAP). While GAAP operating margin rose to 4.2% y-o-y from 2.9%, we see a slight deterioration in non-GAAP operating margin from 9.6% to 8.8%, showing that cost cuts cannot yet fully offset gross margin pressure.

From a cash perspective, the quarter was solid - Intel generated $4.3 billion of operating cash flow, which is important given that the company is in the midst of a massive investment cycle in factories and new process nodes. At the same time, however, it is important to perceive that the Q1 outlook suggests that supply availability will be the weakest link in the short term and may temporarily hamper demand monetization.

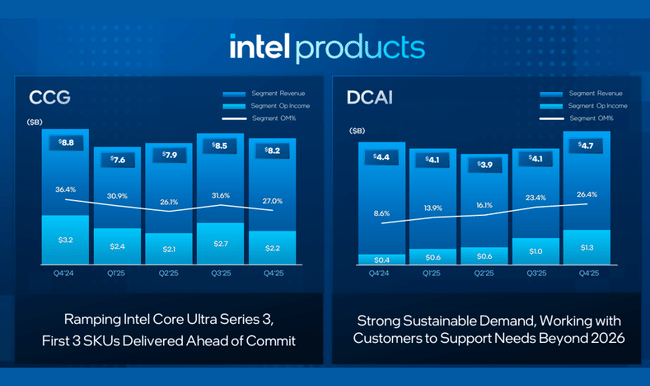

Segment-wise, the picture was significantly mixed and for investors this is one of the most important signals of the quarter. Client Computing Group (CCG), the traditional PC business, earned $8.2 billion, down 7% year-over-year, and $32.2 billion for the full year, down -3%. In contrast, Data Center and AI (DCAI) is growing: $4.7 billion in the quarter represents +9% YoY and the full year $16.9 billion represents +5%. This confirms that Intel may be losing momentum in the traditional PC segment, but datacenter demand and AI infrastructure are keeping the company afloat. In addition, Intel Foundry posted $4.5 billion in Q4 revenue (+4%) and $17.8 billion for the year (+3%), which is a positive signal for the "new Intel" strategy - just be reminded that Foundry revenue includes significant internal intersegment transactions that are subsequently eliminated, so the net impact on consolidated revenue should be read with caution.

CEO commentary

CEO Lip-Bu Tan builds Intel's investment story ever more clearly around a single thesis: in the AI era, CPUs are not losing relevance, on the contrary, their role in the ecosystem is getting stronger because AI computing is not just about GPUs, but about the entire compute stack, workload orchestration, edge inferencing and compatibility with the widely deployed x86 world. Tan called Q4 a solid end to the year and highlighted the progress of the company's transformation. He highlighted the first products on Intel 18A, the most advanced manufacturing process being developed and produced in the US, as a key milestone and said the company is aggressively ramping up capacity to meet strong demand. From a corporate governance perspective, Tan reiterated three priorities that investors will track as KPIs in their own right: improving execution, returning to engineering excellence, and monetizing AI opportunities across the business.

CFO David Zinsner added two important interpretations. First, he said Intel beat internal expectations in revenue, margin and EPS, which should be evidence that restructuring and cost discipline are starting to work. But secondly, he openly admitted that supply will be the lowest in Q1 and only from Q2 onwards the situation should visibly improve. This is relevant not only operationally, but also psychologically for the market: it tells investors that in the short term Intel may be losing opportunities even if demand fundamentally holds.

Outlook

The outlook for the first quarter of 2026 is the main reason why the results may appear ambivalent even if Q4 turned out "above expectations". Intel expects revenue of $11.7 billion to $12.7 billion, a sequential decline from Q4 ($13.7 billion), and that is always uncomfortable at the sentiment level, especially when the market wants to see a turnaround. Gross margins are expected to fall further: GAAP to 32.3% and non-GAAP to 34.5%, a clear signal that margin pressure continues early in the year. GAAP EPS is expected to be $-0.21, while non-GAAP EPS is expected to be $-0.00. Practically speaking, this means that while Intel is showing signs of stabilizing at the non-GAAP level, it cannot return to a sustainable profit mode in the short term, despite significant cuts in R&D and administrative expenses.

From an investment perspective, it is important that management frames Q1 as a "bottoming out of supply" - that is, not a collapse in demand, but a temporary curtailment of production. If this interpretation is correct, and Q2 brings a visible improvement in chip and product availability, then the outlook may quickly tip in subsequent quarters. However, if the supply problem drags on, it will be toxic for Intel, as margins are already bearing the cost of the investment cycle and a delay in monetization would negatively leverage the entire P&L.

Long-term results

The long-term numbers show how dramatically Intel has changed in recent years - and why the market continues to react sensitively to any indication of whether the turnaround is actually happening. Revenues fell from $79.0 billion in 2021 to $63.1 billion in 2022 and further to $54.2 billion in 2023. 2024 brought only a slight decline to $53.1 billion, or -2.1%, technically a stabilization but still at a level that is a third lower than four years ago. From a top-line perspective, this means that Intel has not yet shown a compelling growth engine to offset the structural loss in parts of its traditional segments.

Gross profit has fallen even more sharply. In 2021, Intel generated $43.8 billion in gross profit, in 2022 already $26.9 billion and in 2024 only $17.3 billion. This is a direct result of a combination of lower sales, a worse product mix and higher manufacturing costs during the investment cycle. In addition, the cost base has grown significantly in 2024: operating expenses jumped to USD 29.0 billion, up +34% YoY, and this is one of the main reasons for the giant GAAP loss. Operating profit stood at $19.5 billion in 2021, fell to $2.3 billion in 2022, and broke even to a giant loss of -$11.7 billion in 2024.

Net income and EPS are even more telling. Intel had net profit of $19.9 billion and EPS of $4.89 in 2021. In 2022, net profit fell to $8.0 billion and EPS to $1.95. In 2023, earnings fell further to $1.7 billion and EPS to $0.40. In 2024, Intel reported a net loss of -$18.8 billion and EPS of $4.38. This is an extreme break that reminds investors that even though the company is now presenting a "new Intel", a return to a sustainable profit profile is not yet confirmed.

The EBITDA trend is also interesting and shows how hard the operating economics have changed for the company. EBITDA has fallen from $33.9 billion in 2021 to $21.3 billion in 2022, then to $11.2 billion in 2023 and then to just $1.2 billion in 2024. In other words, Intel has nearly erased its historical "cash machine" profile in the last three years, which is why the market today needs to see not only technology milestones, but also evidence of a return of margins and operating leverage.

News

Among the most important news of the quarter is the launch of Intel Core Ultra Series 3, which Intel is showcasing as the first AI PC platform built on Intel 18A and manufactured in the US. The company expects more than 200 designs from manufacturers across the premium and mainstream segments, which should be a testament to the breadth of adoption. Another major announcement is a collaboration with Cisco on a platform for distributed AI workloads at the edge, built on the Xeon 6 SoC, reinforcing the narrative that AI will not just be in datacenters, but very much "near data." Intel has also centralized the datacenter and AI business under Kevork Kechichian to improve coordination of CPU, GPU and platform strategy.

On the foundry side, Intel is launching the 18A ramp into high-volume manufacturing in Arizona and Oregon, while highlighting a collaboration with ASML on High NA EUV to be the technology pathway to future nodes. On the corporate front, it's worth noting the strengthening of leadership (CIO, government affairs, marketing) as well as the completed sale of $5 billion of Intel stock to NVIDIA to strengthen balance sheet and strategic flexibility. The market will read this move in two ways: as a financial injection and strategic link, but also as a signal that Intel still needs to strengthen its capital position in the midst of a costly transformation.

Shareholding structure

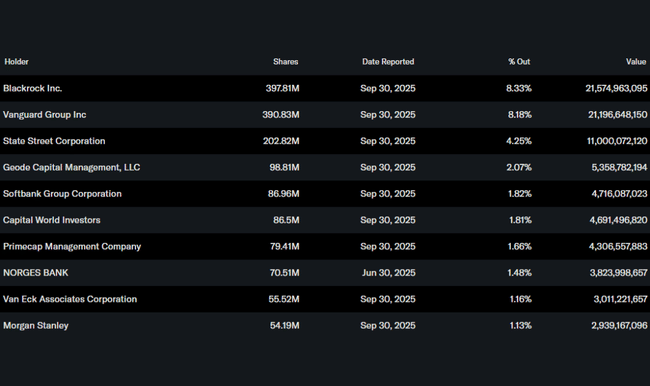

Intel remains the quintessential institutional title: around 63.7% of shares are held by institutions, with BlackRock and Vanguard being the largest shareholders, both around 8.2%-8.3%, followed by State Street (4.25%) and Geode. Insider ownership is low (1.89%), which is not unusual for a firm of this size, but it also means the investment story is based more on execution and market confidence than "skin in the game" leadership.

Analyst expectations

Intel beat its own internal expectations in Q4 on revenue, margin and EPS, which usually helps short-term sentiment. But the key takeaway is that the company also offered weak Q1 guidance: revenue of $11.7-12.7 billion, non-GAAP EPS of $0.00 and non-GAAP gross margin of 34.5%. In practice, this means that analyst expectations for the first half of 2026 are likely to be cautious, with the main question being whether there will be a visible improvement in Q2 after the "supply bottom" in Q1 and whether operating leverage will start to return. For Intel, the market typically does not reward technology milestones on their own unless they are accompanied by margin improvement and a sustainable earnings trajectory.