For the world’s largest luxury group, 2025 marked a clear shift from the exceptional momentum of recent years. Geopolitical uncertainty, weaker consumer sentiment in Europe, and a pronounced slowdown in China contrasted with a more resilient U.S. market. Luxury has moved from broad-based expansion to a phase where growth is selective, pricing discipline matters more, and margin protection becomes central.

The fourth-quarter results reflect that transition. LVMH remains highly profitable and cash generative, yet the group is facing its first broad-based revenue decline in years alongside mounting pressure on key segment margins. The market reaction is therefore cautious—not because the business is broken, but because the era of effortless luxury growth is over.

What was the last quarter and full year of 2025 like?

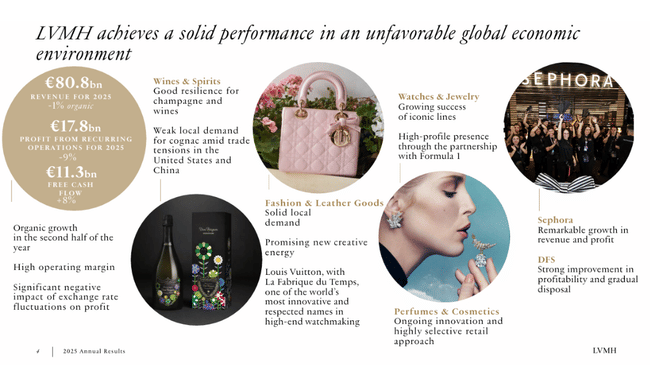

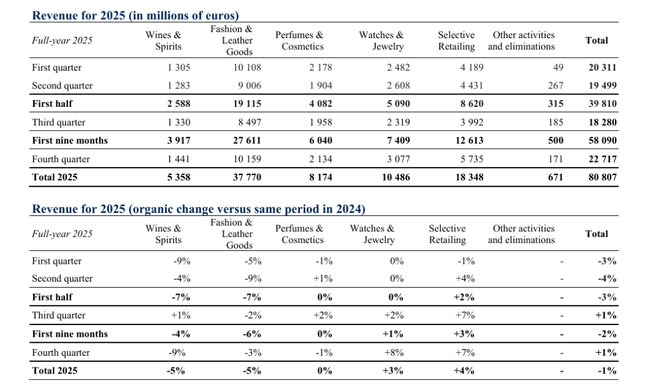

LVMH $MC.PA achieved sales of €80.8 billion in 2025, down five per cent year-on-year, with an organic decline of one per cent. The fourth quarter alone delivered organic growth of one percent, a stabilization from the third quarter but not a return to previous momentum.

Operating profit from ordinary activities came in at €17.8 billion, down nine percent, and operating margin declined to 22 percent. Currency movements and weaker volumes in the segments with the highest historical profitability had a significant impact here. Net profit attributable to the Group was €10.9 billion, down thirteen percent from 2024.

The positive side of the results is cash flow. Operating free cash flow rose eight percent to €11.3 billion, while net financial debt fell 26 percent to €6.9 billion. This confirms that LVMH can generate cash and strengthen its balance sheet quickly even in a worse cycle.

Performance of individual segments

The Fashion & Leather Goods segment, which has long been the Group's main source of profitability, recorded sales of €37.8 billion, down five percent organically. Operating profit decreased by thirteen percent to €13.2 billion, yet the segment maintained an exceptionally high operating margin of 35 percent. The weaker performance was mainly related to the normalisation of demand after an extremely strong 2024, particularly in Japan, where the weak yen helped at the time.

Wines & Spirits was the weakest link in the portfolio. Sales fell organically by five percent and operating profit fell 25 percent to €1.0 billion. The biggest pressure came from the cognac category, where trade barriers and weaker demand in China and the US had a negative impact.

In contrast, Selective Retailing was one of the clear winners of the year. Revenues there grew organically by four percent and operating profit jumped 28 percent to €1.78 billion, mainly due to the continued expansion of Sephora. The segment's margin increased to 9.7 percent, a significant structural shift.

Perfumes & Cosmetics remained stable at the sales level but managed to increase operating profit by eight percent thanks to product innovation, while Watches & Jewelry posted organic growth of three percent but a slight decline in profitability due to higher network development costs.

Management comment

In his comments, Bernard Arnault stressed that 2025 was all about resilience and long-term strategy, not about maximising short-term growth. He said the group was sustained by local customer loyalty, brand strength and the ability to create unique retail and cultural experiences.

At the same time, management openly acknowledges that the environment remains uncertain and that 2026 will not be about aggressive expansion, but about tight cost control, margin protection and further strengthening brand exclusivity. This is a clear shift in tone from 2021-2023.

Long-term results: a return from the peak of the cycle

Looking at the last four years, it is clear that LVMH has entered a normalisation phase after extremely strong growth. Revenues rose from €64.2 billion in 2021 to €86.2 billion in 2023 before falling slightly to €84.7 billion in 2024.

Operating profit peaked at €22.6 billion in 2023, while it fell to €18.9 billion in 2024, corresponding to a decline in margins from around 26 percent to around 22 percent. EBITDA followed a similar trend, declining from €28.6 billion in 2023 to €22.3 billion in 2024.

Net profit increased from €12.0 billion to €15.2 billion between 2021 and 2023, but fell to €12.6 billion in 2024. Earnings per share decreased from €30.3 in 2023 to €25.1 in 2024, confirming that profitability, while normalizing, remains at very high historical levels.

Shareholding structure

LVMH remains a strongly family-controlled group, with almost 50 percent of the shares held by insider structures linked to the Arnault family. Institutional investors hold approximately 18 percent of the shares, with the free float amounting to approximately 36 percent. This implies high management stability, but also lower sensitivity to short-term market pressure.

Outlook for 2026

Management remains cautiously optimistic. It does not expect a return to double-digit growth, but relies on improving trends in Asia, the continued strength of Sephora and the stabilization of Fashion & Leather Goods. Margin protection, selective expansion and further brand strengthening remain priorities.

Dividend policy remains generous, with a dividend of €13 per share to be paid for 2025, confirming management's confidence in its long-term ability to generate cash.

Analyst expectations and target prices

Analyst reaction following the 2025 results has been cautious and significantly less clear-cut than in previous years. The consensus view is that LVMH remains the best-performing asset in the luxury sector, but there is also a growing view that 2026 will be a transitional year and that a return to higher growth may take longer than the market initially expects.

Morgan Stanley maintained its Overweight recommendation following the results, but lowered expectations for near-term momentum. In its commentary, it highlights that while the core Fashion & Leather Goods segment is still generating an operating margin of around 35%, volume growth remains weak and primarily dependent on local demand in the US. The target price, according to their latest estimate, is in the €820-850 range, implying medium-term rather than rapid growth potential.

Goldman Sachs is more conservative and points to a structural change in consumer behaviour in China. According to the bank, Chinese demand is unlikely to return to the pace of 2021-2023 and the luxury sector is entering a longer phase of normalisation. Goldman Sachs maintains aNeutral stance with a target price of around €780, citing margin pressure and weaker operating leverage with low organic growth as the main risks.