Meta’s recent performance confirms that the core business has regained its footing. Advertising is once again scaling efficiently, margins remain exceptionally high, and the company is operating from a position of financial strength rather than recovery. In isolation, these are precisely the conditions investors usually reward. Yet markets rarely react to numbers in isolation, especially when the narrative has already shifted toward what comes next.

The focus has moved decisively from earnings generation to capital allocation. Meta’s ambition to build the next phase of AI-driven platforms introduces a new layer of uncertainty, not about execution capability, but about cost and timing. With infrastructure spending set to rise sharply, the central tension is whether profitability growth can keep pace with the scale of investment. The business looks strong, but the valuation debate increasingly lives in the future rather than the present.

How was the last quarter?

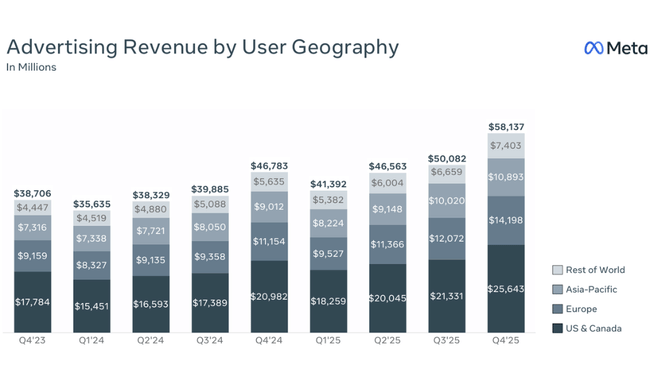

Meta $META ended 2025 with a very strong quarter. Q4 revenue reached $59.9 billion, up 24% year-over-year, confirming the continued recovery of the advertising market as well as Meta's ability to increase the monetization of its platform. The growth was not only driven by volumes, but also by price - ad impressions grew 18% YoY, while average cost per ad increased by 6%, which together creates a very healthy mix.

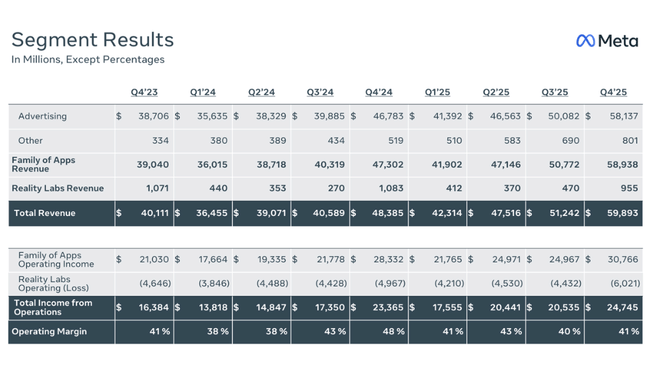

On an operating level, the company reported operating income of $24.7 billion, up +24% YoY, and an operating margin of 41%, among the highest in the technology sector. Net income came in at $22.8 billion, +30% YoY, and EPS rose to $8.88 (+9% YoY). The lower EPS growth rate versus net income is related to tax items and the comparative base.

For clarity, the key Q4 highlights can be summarized as follows:

Revenue: USD 59.9 billion, +24% YoY

Operating income: USD 24.7 billion, +24% YoY

Operating margin: 41%

Net profit: USD 22.8 billion, +30% YoY

EPS: USD 8.88, +9% YoY

Ad impressions: +18% YoY

Average price per ad: +6% YoY

Family DAP: $3.58 billion, +7% YoY

From a cash flow perspective, the quarter was also very strong. Operating cash flow was USD 36.2bn, while free cash flow was USD 14.1bn, despite high investments. Capex in Q4 was USD 22.1 billion, which clearly shows that Meta is already in the full phase of a massive AI infrastructure build-out.

CEO commentary

In his comments, Mark Zuckerberg called 2025 a very strong year in terms of performance, while openly defining the next strategic shift towards "personal superintelligence". It is clear from his words that Meta is no longer content with optimizing its advertising business, but wants to become one of the major global players in advanced AI.

Zuckerberg also hinted that 2026 will be a year of intense investment, not maximizing short-term profit. This tone is key to understanding the market's reaction - investors hear a clear vision, but they also know that the path to fulfilling it will be capital intensive.

Outlook

The outlook for 2026 is a major point of investor debate. Meta expects Q1 2026 revenues in the range of US$53.5-56.5bn, with currency rates expected to be roughly 4% positive for year-on-year growth. At the same time, however, the firm is announcing total costs for the full year 2026 of US$162-169bn, a significant increase from 2025.

More importantly, the capex outlook of USD 115-135bn signals a massive acceleration in investments in AI infrastructure, data centres and Meta Superintelligence Labs. While management expects operating profit in 2026 to be higher than in 2025, the market is concerned that the pace of profitability growth may not match the pace of investment growth in the short term.

Long-term results

A long-term view of Meta's results shows an exceptionally strong transformation of the company over the past four years. Revenues have grown from US$116.6bn in 2022 to US$201.0bn in 2025, equivalent to more than 70% cumulative growth. Meanwhile, the growth rate remains steadily above 20% even for a company this large, which is exceptional in the advertising business.

Gross profit grew at a similar rate, reaching USD 164.8 billion, while cost of sales increased in a relatively controlled manner. However, the key factor was operating expenses, which jumped 25% YoY to US$81.5bn in 2025. This increase is largely driven by investments in AI, R&D and infrastructure and represents a fundamental change from the extremely disciplined post-2022 period.

Despite this, operating income grew to US$83.3bn (+20% YoY) and EBITDA reached US$104.5bn, confirming that the core advertising business is generating huge amounts of cash. However, there is a notable break at the net income level - net income is down slightly by 3% in 2025, and EPS is also down by around 2%, although operating performance remains strong. This is mainly due to tax changes and high investment, not a deterioration in the core business.

The long-term numbers thus show a company that is extremely profitable, but also entering a new investment phase where some short-term profitability is being sacrificed in favor of a strategic position in AI.

News

Meta continued to expand AI capabilities across its platforms during the quarter and is preparing to launch additional versions of less personalised advertising in Europe in response to regulatory pressure. At the same time, the firm highlighted ongoing legal and regulatory risks in the EU and US, including litigation relating to the protection of minors, which may have extreme financial implications.

Shareholding structure

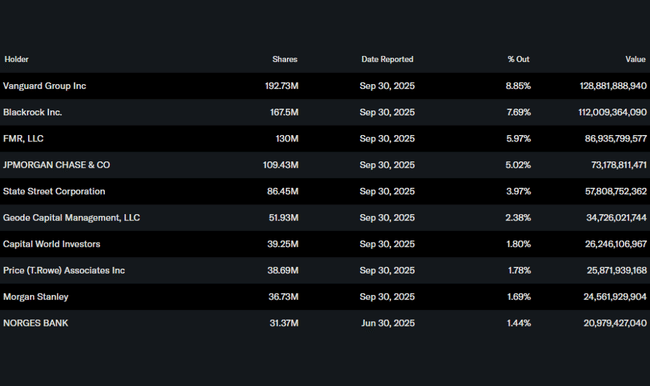

The shareholding structure remains strongly institutional, with the institution holding approximately 79% of the shares. The largest shareholders include Vanguard (8.9%), BlackRock (7.7%), FMR (6.0%) and JPMorgan (5.0%). A low insider stake has been the long-standing standard at Meta, offset by the founder's controlling role.

Analyst expectations

Analyst reaction following the results has been mixed. Most appreciate the continued strength of the advertising business, the growth of the user base and the high operating margin. At the same time, however, there is growing caution due to the extremely high capex in 2026 and the uncertain return on investment in superintelligence. So consensus remains positive in the long term, but in the short term the market is reacting nervously - not because of what Meta has earned, but because of how much it will have to invest to maintain that position.