Altria's fourth-quarter and full-year 2025 results confirmed that the company remains one of the most stable players in the U.S. nicotine products market. Even in an environment of declining conventional cigarette volumes, Altria is able to generate robust earnings, increase adjusted earnings per share, and return massive amounts of capital to shareholders. It is this combination of predictability, pricing power and dividend policy that has long been at the heart of the investment story.

But at the same time, the results and outlook for 2026 show the limits of this model. Profitability growth remains in the low single-digit percentages, quarterly sales figures are rather weaker, and the main positive impulses come from cost optimisation, tax factors and share buybacks, not from business expansion. The market thus sees Altria primarily as a defensive dividend title, not a growth stock.

How was the last quarter?

The fourth quarter of 2025 presented a mixed picture. Net sales came in at $5.85 billion, down 2.1% year-over-year. Adjusted for excise taxes, revenue net of excise taxes was $5.08 billion, -0.5% YoY. Thus, revenues continue the long-term trend of slight decline, which is the structural nature of the US tobacco market.

GAAP profitability was impacted by the comparative base. Reported diluted EPS in Q4 was $0.66, down 63% YoY, but this decline is primarily due to one-time items in the prior year. More relevant from an operating performance perspective is adjusted diluted EPS, which came in at $1.30, indicating year-over-year stability.

The tax rate declined significantly in the quarter. The adjusted tax rate was 22.8%, compared to a significantly higher rate in Q4 2024, which positively supported net income. Again, however, it should be stressed that this is a factor that cannot be automatically extrapolated into the future.

Q4 2025 summary in points:

Net revenues: USD 5.85 billion(-2.1% YoY)

Revenues net of excise taxes: USD 5.08 billion(-0.5% YoY)

Adjusted diluted EPS: USD 1.30 (stable YoY)

Reported diluted EPS: USD 0.66(-63% YoY, impact of one-off items)

Adjusted tax rate: 22.8%

Thus, the quarter reaffirmed that short-term fluctuations in GAAP earnings levels are not key for Altria $MO; the ability to steadily generate adjusted earnings and cash is critical.

Full year 2025: stability despite earnings pressure

For the full year 2025, Altria reported net revenues of $23.28 billion, down 3.1% year-over-year. Adjusted for excise taxes, revenue net of excise taxes was USD 20.14bn, -1.5% YoY. Thus, the decline in volumes of traditional tobacco products continues but is partly offset by price increases and product mix.

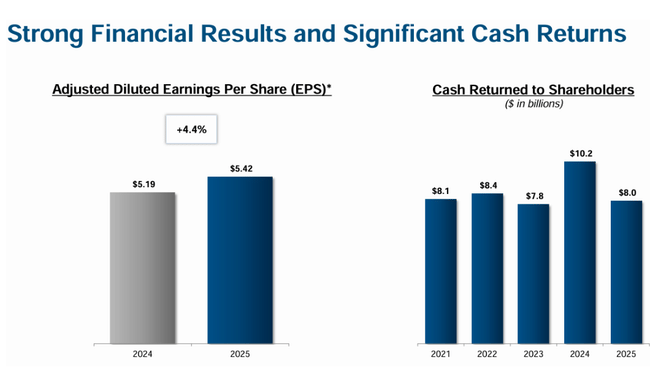

Profitability remained very strong. Adjusted diluted EPS for 2025 was $5.42, up 4.4% YoY. This is the key number of the entire report, as it shows that Altria is able to grow earnings per share even in a declining revenue environment thanks to pricing power, cost discipline, and share repurchases.

CEO commentary

CEO Billy Gifford called 2025 a year of continued momentum. His comments highlighted a combination of strong financial performance, advances in smokeless products and strong returns of capital to shareholders. Management openly asserts that near-term growth will not be driven by volumes, but by efficiency and strategic portfolio realignment.

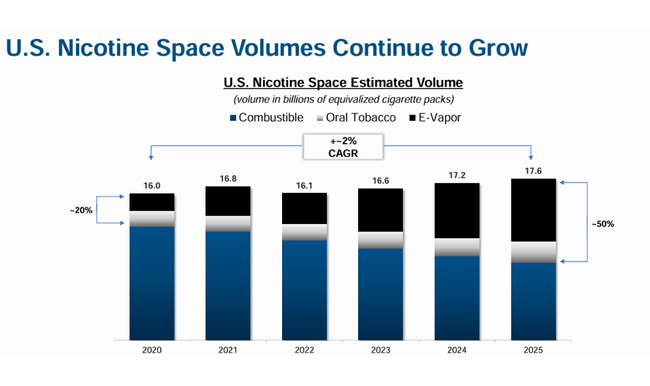

The comments indicate that Altria's management is focused on the long-term transition to "smoke-free" products, particularly in the oral nicotine space, while being cognizant of the regulatory and competitive risks in the e-vaping segment. Management's tone is realistic and conservative, which is key for this type of company.

Outlook for 2026

The outlook for 2026 is one of the most important points of the entire report. Altria expects adjusted diluted EPS in the range of $5.56-$5.72, which corresponds to 2.5%-5.5% year-over-year growth from a base of $5.42 in 2025. Management also notes that earnings growth will be weighted more heavily into the second half of the year due to, among other things, a gradual increase in cigarette import and export activity.

Guidance further assumes:

Adjusted effective tax rate: 22.5-23.5%

Capex: EUR 300-375 million. USD 30000

Depreciation and amortisation: approximately USD 225 million. USD 250 USD

Outlook assumes continued investment in contract manufacturing, smokeless product development and regulatory preparation. It also explicitly includes the assumption that NJOY ACE will not return to the market in 2026, limiting the potential for faster expansion in e-vaping.

Long-term performance

The long-term numbers illustrate the essence of Altria's investment story very well. Revenue declined slightly between 2021 and 2024, from US$21.1bn to US$20.4bn, confirming the structural pressure on volumes. At the same time, however, gross profit remained stable at around US$14.3bn, reflecting the firm's exceptional pricing power.

Operating income stood at USD 11.2 billion in 2024, only slightly below the previous years. In contrast, net income grew significantly, from US$2.5bn in 2021 to US$11.3bn in 2024, driven by a combination of cost optimisation, tax factors and financial structure.

EPS grew from US$1.34 in 2021 to US$6.54 in 2024, with a significant role played by a decline in the number of shares outstanding as a result of systematic share buybacks. EBITDA also grew over the long term, reaching US$15.1bn in 2024, confirming an exceptionally high operating margin.

Cash flow and return on capital

Return of capital to shareholders remains a key pillar of the strategy. In 2025 Altria:

paid dividends of USD 7.0 billion

Repurchased shares for USD 1.0 billion

In total, it returned approximately USD 8 billion to shareholders

In Q4, the company repurchased 4.8 million shares at an average price of USD 59.56. It still has USD 1bn available until the end of 2026 under the approved buyback program.

Shareholder structure

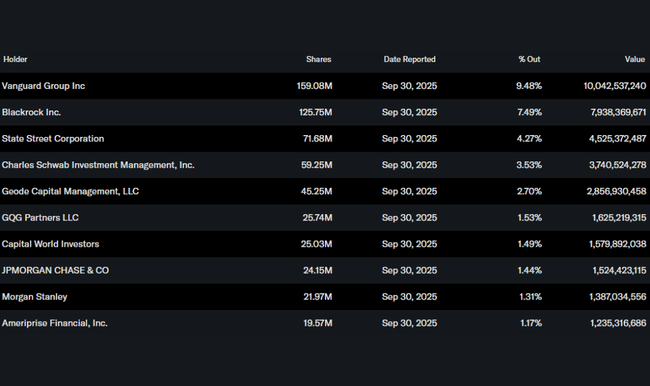

The shareholder structure is predominantly institutional, with the institution holding approximately 63% of the shares. The largest shareholders are Vanguard (9.5%), BlackRock (7.5%), and State Street (4.3%). Insider ownership is minimal, which has been the long-term standard for Altria.

Analyst expectations

Analyst consensus remains moderately positive. Altria is viewed as a highly predictable dividend title with low growth but very strong cash flow. Analysts appreciate the company's ability to grow adjusted EPS even in an environment of declining revenues, but also note regulatory risks, uncertainty around e-vaping, and limited long-term growth potential.