In a softer commodity price environment, headline profits often lose their signaling power. What matters more is whether an energy major can keep cash generation stable while expanding its production base. Chevron’s latest performance points precisely in that direction. Operational execution reached new highs even as macro conditions worked against margins, suggesting the cycle has shifted from price dependency to asset-driven resilience.

The strategic focus now lies beyond quarterly earnings. Integration progress, project ramp-ups, and reserve replacement are reshaping the long-term profile of the business. Investors are watching whether this combination of volume growth and capital discipline can persist through different price regimes. The underlying question is not how Chevron performs in a strong oil market, but how durable its cash engine remains when conditions are less forgiving.

How was the last quarter?

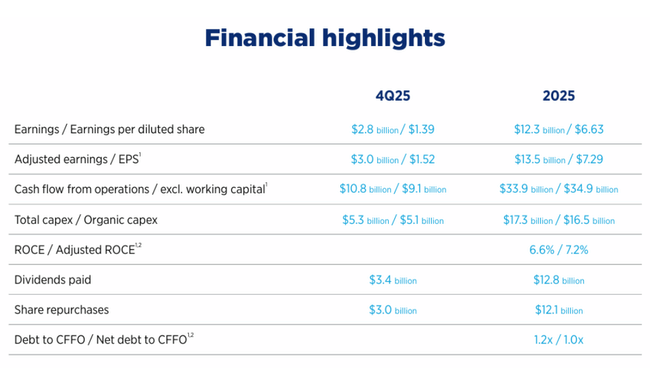

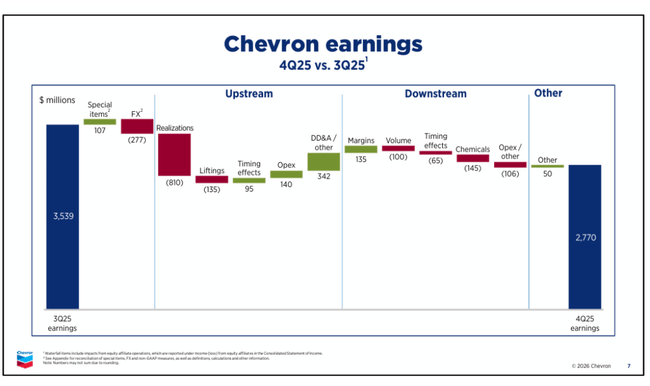

Chevron reported net income of $2.8 billion in the fourth quarter of 2025, which equates to earnings of $1.39 per share. Adjusted earnings were $3.0 billion, or $1.52 per share, down year-over-year primarily due to lower realized oil prices, negative currency effects and one-time costs associated with pension settlements. However, operating numbers remained very strong.

Operating cash flow was $10.8 billion, while adjusted free cash flow was $4.2 billion. Even with weaker commodity prices, Chevron is generating cash that allows it to fund investments, reduce debt and return capital to shareholders. ROCE was 5.4% in the quarter, reflecting cyclical price pressure rather than a structural efficiency issue.

In terms of segments, upstream remains the key driver. Total production reached 4.0 million barrels of oil equivalent per day, up more than 20% year-on-year, with the Hess acquisition and projects in the Permian Basin and Gulf of Mexico contributing a significant portion of the growth. Downstream was stable, with improved refining margins partially offsetting upstream pressure.

CEO commentary

CEO Mike Wirth called 2025 one of the most significant years in the company's history. He emphasized that Chevron was able to successfully integrate Hess, launch key projects and reorganize the company to be more resilient to commodity price fluctuations. He said the combination of record production, structural savings and discipline in capital spending led to the highest operating cash flow ever at comparable oil prices.

Outlook

For 2026, Chevron expects continued strong production and further efficiency gains. The company is targeting further structural cost reductions, with a savings program to reach $3-4 billion annually by the end of 2026. Capital expenditures remain under control, although they will be increased due to investments in new projects and energy infrastructure.

From a shareholder perspective, the confirmation of the dividend policy is key. Chevron raised its quarterly dividend by 4% to $1.78 per share and is heading for its 39th consecutive year of dividend growth. At the same time, the company is continuing its extensive share repurchases, which supports long-term earnings per share growth even with fluctuating oil prices.

Long-term results

A look at 2021-2024 clearly shows the cyclical nature of Chevron's business, but also its ability to adapt quickly. The company's revenues peaked at more than $235 billion in 2022 due to extremely high energy prices, while 2023 and 2024 saw a normalisation towards around $195 billion. However, this decline has not been accompanied by a collapse in profitability.

Net income in 2024 was $17.7 billion, down from a record year in 2022 but still well above the long-term average before the energy crisis. EPS was around $9.7 in 2024, showing that even with lower oil prices, Chevron remains a highly profitable company. Another important factor is the declining share count due to buybacks, which has supported EPS over the long term.

Operationally, Chevron has significantly improved reserve replacement. It has achieved a 158% reserve replacement ratio in 2025, which means the company can not only produce but also successfully recover its reserves, thanks largely to the Hess acquisition and new discoveries in the Permian Basin, Guyana, and Australia. EBITDA has remained at very high levels over the long term, although it is sensitive to the price cycle.

News

The year 2025 was an exceptionally busy one for Chevron with strategic milestones. The company completed the acquisition of Hess and achieved projected synergies of $1 billion. The Future Growth Project was launched in Kazakhstan, while several deepwater fields reached first production in the Gulf of Mexico. There was also a major breakthrough in Guyana, where Chevron started production from the Yellowtail field and approved further investments.

In addition to traditional energy, Chevron has entered the US lithium sector, investing in renewable fuels and announcing projects to support the energy needs of US data centres. These moves demonstrate an effort to diversify future sources of cash flow without abandoning the core oil and gas business.

Shareholding structure

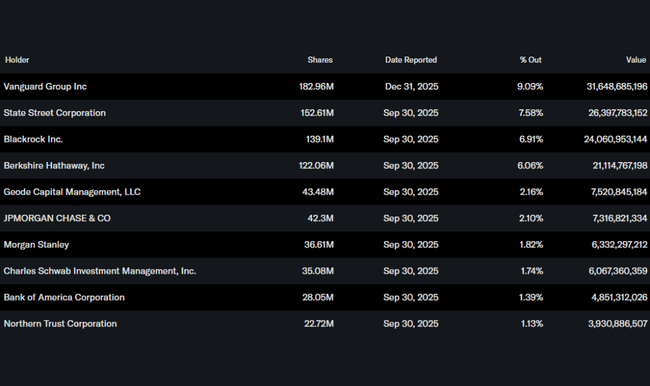

Chevron has a very stable institutional base. Approximately 68% of the shares are held by institutions, with Vanguard, State Street, BlackRock and Berkshire Hathaway among the largest shareholders. The presence of Berkshire Hathaway has long reinforced the perception of Chevron as a quality dividend title with disciplined capital management.

Analyst expectations

Analysts view Chevron as one of the highest quality "large-cap" energy companies. In the short term, they note the sensitivity of earnings to oil prices, but in the long term they appreciate the combination of a strong balance sheet, record production, high reserve replacement and consistent dividend growth. The investment thesis thus rests less on oil price speculation and more on a steady ability to generate cash across the cycle.