The opening quarter of fiscal 2026 places Disney firmly in a transition phase rather than a clean inflection. Core engines are working: the Experiences segment continues to deliver resilient growth, while streaming moves closer to sustainable profitability. On the surface, the business is doing what investors have been asking for.

The market reaction reflects timing rather than direction. Elevated content and sports-rights costs, combined with residual pressure in linear media, weigh on near-term earnings momentum. This quarter looks less like a payoff and more like a consolidation step, as management openly points to a stronger second half. The tension lies in patience: whether investors are willing to wait for the operating leverage that is still ahead.

How was the last quarter?

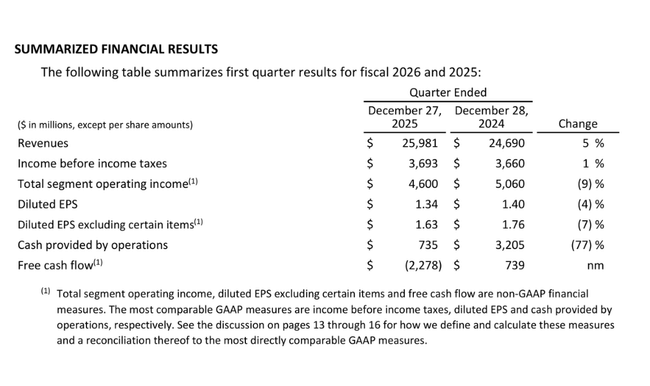

Disney $DIS revenue in Q1 FY2026 grew 5% year-over-year to $26.0 billion. Growth was driven primarily by the Experiences segment and a solid Entertainment performance, while the Sports segment delivered only a modest increase in revenue. Pre-tax profit was $3.7 billion, remaining roughly in line with last year, but total segment operating profit fell 9% to $4.6 billion.

Earnings per share saw a slight deterioration. Diluted EPS came in at $1.34 compared to $1.40 in the prior year, while adjusted EPS fell to $1.63 from $1.76. This decline is an important signal that despite revenue growth, Disney is facing margin pressure in the short term.

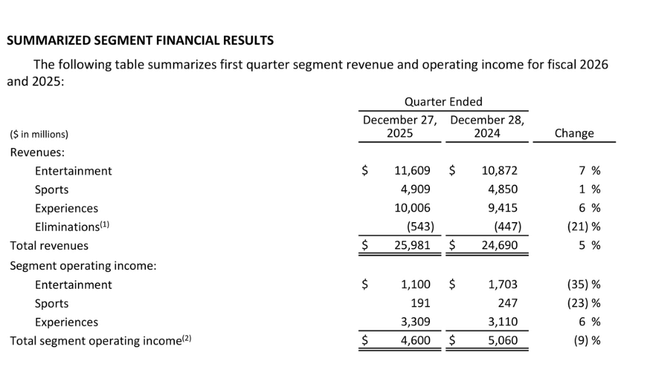

A detailed look at the segments explains the structure of the results. Entertainment grew revenue by 7%, but segment operating profit fell 35% to $1.1 billion. The main reason was higher production and marketing costs, which outweighed the positive effect of higher subscription fees and strong theatrical performance of titles such as Zootopia 2 and Avatar: Fire and Ash.

Conversely, the streaming portion of SVOD is becoming one of the most positive elements of the results. SVOD revenue grew 11% and operating profit increased $189 million to $450 million, for an 8.4% margin. This clearly confirms that the transformation of Disney+ and Hulu towards a sustainable business is starting to bear fruit.

The Sports segment reported an operating profit of $191 million, down 23% year-on-year. The negative impact of the temporary suspension of distribution on YouTube TV, which reduced operating profit by approximately $110 million, as well as the increase in sports rights costs, was significant here.

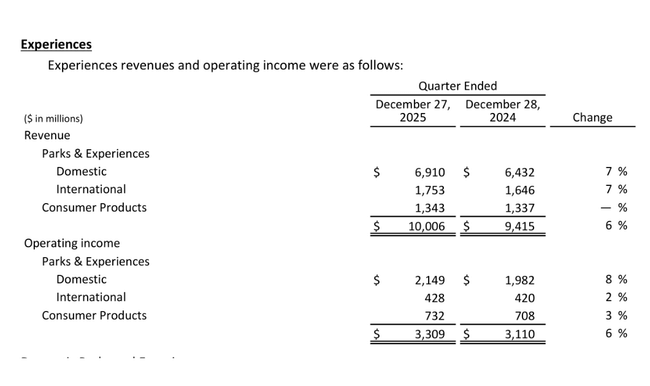

Experiences remains the strongest pillar. The segment achieved record quarterly revenues of $10.0 billion and operating profit of $3.3 billion. Home Parks saw attendance growth of 1% and per capita spending increased 4%, confirming the pricing strength of the brand even in a more challenging macroeconomic environment.

CEO commentary

Robert A. Iger assessed the start of the fiscal year positively, highlighting in particular Disney's ability to generate value across its entire brand ecosystem. He pointed to an exceptionally strong box office in calendar year 2025, with several titles ranking among the billion-dollar hits, and the fact that these franchises are generating secondary revenue in parks, merchandising and streaming.

Iger also hinted that the last three years of restructuring and more disciplined cost management are starting to be seen, particularly in streaming. He said Disney is now better prepared to manage the business with a long-term horizon, although short-term fluctuations in some segments remain a reality.

Outlook

Management's outlook is considerably more optimistic than the first quarter results themselves. For Q2 FY2026, Disney expects segment operating profit in Entertainment to be comparable to last year, with SVOD expected to achieve an operating profit of approximately $500 million, an improvement of approximately $200 million year-over-year.

Sports is expected to face an operating profit decline of roughly $100 million in the second quarter due to higher rights costs, while Experiences should see modest profitability growth despite headwinds from lower international attendance and new project costs.

Full-year guidance for fiscal 2026 is built for acceleration in the second half. Disney expects double-digit segment operating profit growth in Entertainment, SVOD margin around 10%, low single-digit profitability growth in Sports and high single-digit growth in Experiences. Adjusted EPS is expected to grow at a double-digit rate year-over-year, and operating cash flow is expected to reach about $19 billion. Management is also confirming a $7 billion share buyback plan.

Long-term results

A look at the last four fiscal years shows a significant turnaround in the company's profitability. Revenues have grown from $82.7 billion in fiscal 2022 to $94.4 billion in 2025, with growth rates stabilizing around 3-7% annually.

Even more striking is the evolution of operating profit, which has increased from $6.8 billion in 2022 to $13.8 billion in 2025. Net income has seen a jump in growth, going from $3.1 billion in 2022 to $12.4 billion in 2025. EPS has increased from $1.73 to $6.88 over the same period, clearly showing the return of operating leverage after a pandemic period and restructuring.

The company has undergone significant volatility over the past few years, reflecting a combination of structural changes in the media business and cyclical factors associated with the return of physical entertainment. While revenue and profitability growth in 2022 and 2023 was dampened by high content cost pressures, restructuring of media activities and weaker monetization of streaming, key segments gradually began to show signs of stabilization. In particular, the gradual return of attendance and pricing power in theme parks was a significant positive factor, as they moved back from cyclical lows to above-average profitability and began to regain their role as a major cash generator. This shift allowed the company to partially offset the weaker performance of its traditional media businesses and set the stage for renewed operating profit growth.

On the other hand, however, the evolution of profitability remained uneven, as higher sales were not always accompanied by a corresponding improvement in margins. Increasing investment in content, marketing and technology, together with pressure on sports rights and a volatile advertising market, led to limited operating leverage in some years. As a result, net income and earnings per share fluctuated not only in response to operating performance, but also due to one-off items, tax effects and changes in capital structure. Overall, the long-term development can be characterised as a transition from a phase of restructuring and investment to a phase of gradual stabilisation, with the key question for the coming years being whether the growing sales and strong demand can be translated into sustainable growth in margins and free cash flow.

News

Key structural changes include the consolidation of Hulu Live TV with Fubo, where Disney holds a 70% stake, and the formation of an Indian joint venture with Reliance Group, where Disney has a 37% stake. These moves reduce capital intensity and volatility in lower-return regions and segments.

At the same time, the company continues to expand its theme parks, including investments in Disneyland Paris and the development of the cruise segment, which should strengthen Experiences as a key stabilizing element of the overall portfolio.

Shareholding structure

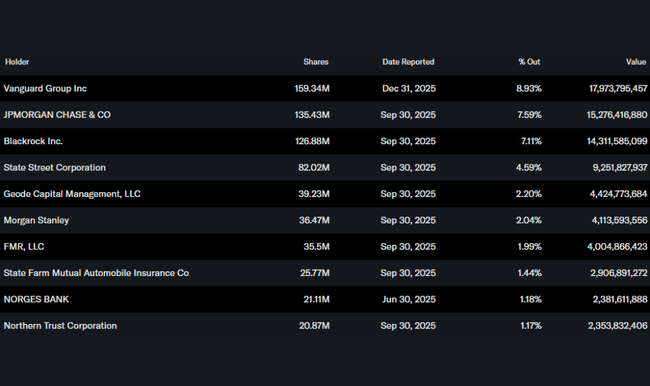

Disney shares are more than 75% held by institutional investors. The largest holdings are held by Vanguard, JPMorgan Chase, BlackRock and State Street, underscoring the company's character as a long-term institutional title with an emphasis on stability and return on capital.

Analyst expectations

Analysts view Q1 results as a temporary wobble rather than a change in the long-term story. Large investment houses in particular highlight the rapidly improving streaming economics and resilience of the Experiences segment. Consensus expects the key catalyst for the stock to be the second half of fiscal 2026, when double-digit earnings growth and strong cash generation should be evident.