Coca-Cola’s fourth-quarter and full-year results confirm the structural resilience of the business, while also highlighting the limits of growth in a fully saturated global beverage market. Revenue continues to rise primarily through pricing, product mix and brand strength rather than volume expansion. For investors, this reinforces what Coca-Cola is—and what it is not: a cash-generative, predictable franchise rather than a growth story.

That dynamic defined 2025. Organic revenue growth remained solid and earnings per share moved higher, but currency headwinds, higher marketing spending and one-off charges weighed on reported margins. The results therefore require a nuanced reading. The key is separating structural trends from temporary accounting noise when assessing the durability of profitability.

What was the last quarter like?

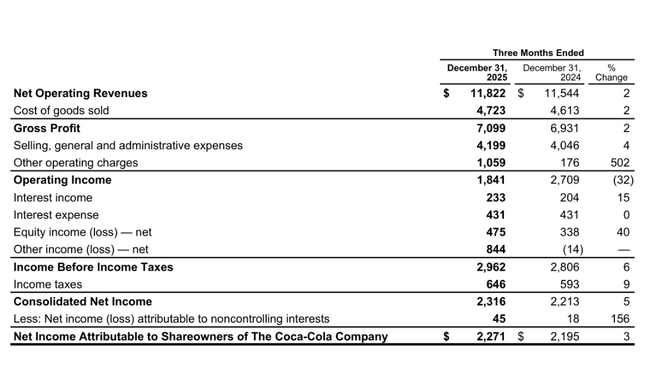

In the fourth quarter of 2025, Coca-Cola $KO achieved net sales of $11.8 billion, up 2% year-on-year. At first glance, this is a low number, but looking at the structure, it's clear that the core business grew faster. Organic sales, adjusted for currency effects and portfolio changes, grew 5%. This difference is key, as the strong dollar remains one of the main factors holding back Coca-Cola's reported numbers over the long term.

Revenue growth was driven primarily by price and product mix. Price/mix added roughly 1% in the quarter, while concentrate sales rose 4%. Units sold increased by only 1%, confirming that beverage consumption is growing very slowly globally and even stagnating in some regions. Thus, Coca-Cola continues to rely on its ability to increase the value of the portfolio sold, rather than on volume expansion.

Profitability has attracted the most attention. Operating profit fell 32% year-on-year and operating margin slumped to 15.6% from 23.5% last year. However, this decline does not reflect a deterioration in operating performance. The non-cash write-down of the BODYARMOR trademark of USD 960 million and negative currency effects played a key role. Adjusted for these items, comparable operating profit grew 13% in constant currencies, clearly demonstrating that the underlying economics of the business remain sound.

Reported earnings per share rose 4% to $0.53, while adjusted EPS was $0.58, up 6% year-on-year. Here too, the strong dollar had a negative impact, cutting around five percentage points from growth.

CEO commentary

James Quincey's assessment highlighted in particular the ability of the entire Coca-Cola system to perform consistently across regions even in an environment of heightened uncertainty. He said 2025 confirmed that the combination of strong global brands, locally relevant marketing and disciplined cost management creates a sustainable model for the long term.

Quincey also hinted that the next phase of the company's evolution will be less about portfolio expansion and more about execution quality. The focus is to be on digital transformation, deeper work with data, better marketing targeting and more effective collaboration with fulfillment partners. The goal is not to maximize short-term volume, but to increase value per consumer over the long term.

Outlook for 2026

Management has provided an outlook that can be described as conservative but realistic. Coca-Cola expects organic revenue growth in the range of 2% to 4%, which is consistent with the company's long-term trend. Adjusted earnings per share in constant currencies should grow by 4% to 6%, with currency rates likely to be slightly positive this time around.

Cash handling is an important point. The company plans to keep capital expenditure below 5% of sales and free cash flow conversion above 80%. This creates a comfortable space for further dividend increases and maintaining an attractive payout profile, which is one of the main reasons for investors to hold Coca-Cola.

Long-term results and structural development

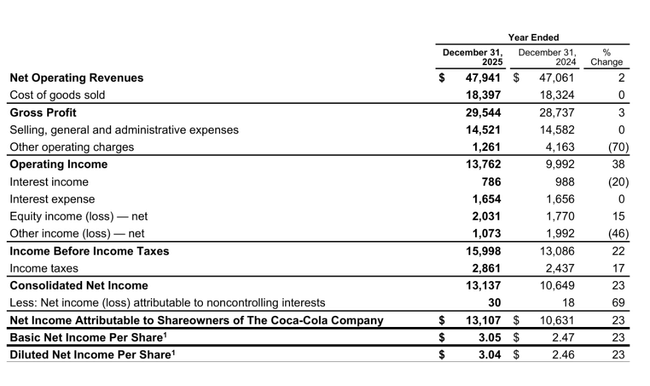

A look at the last four years clearly shows how Coca-Cola has moved into a phase of highly stable but low-dynamic growth. Revenues have grown from approximately $38.7 billion in 2021 to more than $47 billion in 2024. The growth rate has gradually slowed, but has remained consistent even during periods of elevated inflation and currency fluctuations.

Gross profit grew faster than sales, confirming the strength of brands and their ability to pass through higher costs to end prices. At the level of operating profit, the trend has been more volatile. The year 2024 brought a decline in operating profit of around 12%, mainly due to higher marketing investments and restructuring costs. However, EBITDA remains stable in the range of USD 14 billion to USD 16 billion over the long term, confirming the high quality of cash flow.

Net profit has been around USD 9 billion to USD 10 billion per year in recent years and earnings per share have been growing only moderately. This is a direct result of market maturity, not brand weakness. Today, Coca-Cola is maximizing return on capital, not volume growth, which is exactly what a conservative investor expects.

News and strategic moves

The year 2025 was marked by a strengthening of local brand relevance. The company invested heavily in marketing platforms targeting younger consumers, sporting events and local consumption opportunities. At the same time, organisational changes were made, including the creation of the Chief Digital Officer role to align data, digital and operational efficiencies across regions.

These moves do not have an immediate financial impact, but are designed to improve the long-term competitiveness of the system and reduce the risk of Coca-Cola losing touch with a new generation of consumers.

Shareholding structure

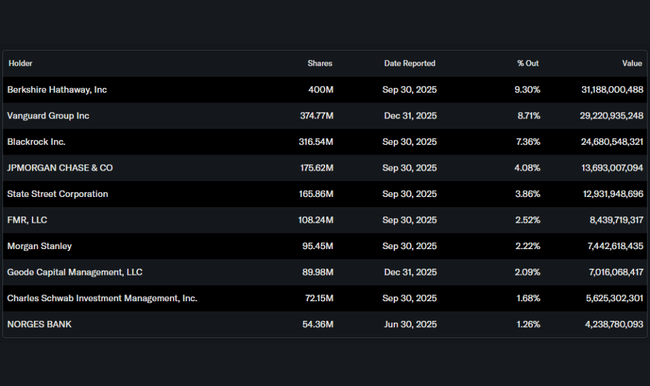

The shareholding structure remains extremely stable. Berkshire Hathaway holds a significant stake, as do Vanguard and BlackRock. The high proportion of institutional investors supports the company's long-term management horizon and emphasis on dividends rather than short-term capital experimentation.

Analyst expectations

Analyst consensus views Coca-Cola as a defensive title with limited growth potential but a high degree of certainty. Expectations hover around low single-digit earnings growth rates, with currency movements, the ability to maintain pricing discipline and the level of marketing investment remaining key variables.

Some banks have warned that the stock may come under pressure in the short term due to stagnant volumes and fluctuating margins, but the long-term investment story remains unchanged: stable brands, strong cash flow and a reliable dividend.