Shopify enters 2026 no longer framed as a high-growth company chasing scale at the expense of profitability. The 2025 performance marked a structural shift: revenue momentum remained strong, operating leverage improved meaningfully, and cash generation became a central part of the story. In Q4 alone, revenue grew 31% year over year, gross profit approached $1.7 billion, and free cash flow reached $715 million.

What matters more than the headline growth is the consistency beneath it. Shopify has now delivered double-digit free cash flow margins for ten consecutive quarters, a notable achievement for a company still expanding at this pace. The newly announced $2 billion share repurchase program reinforces management’s confidence that the current growth trajectory is durable and not dependent on temporary tailwinds.

How was the last quarter?

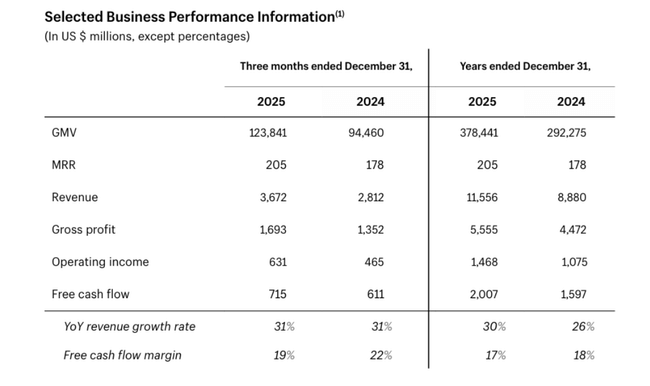

The fourth quarter of 2025 was very strong in terms of numbers. Gross merchandise volume (GMV) sold through the platform reached $123.8 billion, up from $94.5 billion a year ago, representing approximately 31% year-over-year growth. This growth is important because GMV is the basis for revenue from payments, financing and other services.

Revenue for the quarter was $3.672 billion, compared to $2.812 billion in the same period in 2024. Gross profit rose to $1.693 billion from $1.352 billion. Operating profit was $631 million, up from $465 million a year earlier. This further improves operating margins and confirms Shopify's scaling model is working.

Free cash flow for the quarter was $715 million, a 19% margin. This continues the company's streak of ten consecutive quarters with double-digit free cash flow margins. This is a major change from a few years ago when the business was heavily investable and volatile.

In terms of revenue structure, Subscription Services and Merchant Solutions reached $777 million and $2.895 billion, respectively. Merchant solutions, i.e. fees from payments, financing and other services, remain the main driver of growth. Costs grew slower than revenue, which translated into better operating leverage.

Net income for the quarter was $743 million. Adjusted for the impact of equity revaluation, adjusted net profit was $594 million, better reflecting the actual performance of the core business.

For the full year 2025, Shopify then earned $11.556 billion compared to $8.880 billion in 2024. Operating profit rose to $1.468 billion from $1.075 billion. Free cash flow for the year reached $2.007 billion at a margin of 17%.

Management Commentary

President Harley Finkelstein called 2025 a "full-throttle" year, with Shopify $SHOP not only accelerating growth but also building the infrastructure for the AI-powered commerce era. He stressed that 2026 is set to be "the year of the makers" and Shopify wants to be at the heart of their business from first order to global expansion.

CFO Jeff Hoffmeister praised the combination of 30% revenue growth for the full year and a 17% free cash flow margin. He said the company was able to invest in key projects - the product catalog, Sidekick assistant, a new universal commerce protocol and other tools - and still maintain strong profitability. He also highlighted strength across regions, merchant size and sales channels.

Outlook for 2026

For the first quarter of 2026, the company expects to:

Revenue growth in the low 30 percent year-over-year, similar to the fourth quarter of 2025

gross profit growth in the upper 20 percent

operating costs at 37-38% of sales

free cash flow margin in the low to mid-teens percentages, slightly below Q1 2025 levels

An important step is the announced share buyback program of up to $2 billion. The company doesn't have a fixed pace of buybacks, but the authorization itself signals that it is generating enough cash while seeing long-term value in its own stock.

Long-term results

In 2021, sales were $4.6 billion, operating profit was $269 million and net income exceeded $2.9 billion, thanks in part to one-time effects. The year 2022 was dramatic: while sales rose to $5.6 billion, the company posted an operating loss of $822 million and a net loss of $3.46 billion. It was a period of high investment and a slump in technology valuations.

The year 2023 marked a stabilization. Revenues were $7.06 billion, but operating profit was still negative (-1.418). Net profit was only $132 million, significantly affected by the revaluation of investments.

The turning point came in 2024. Revenues rose to $8.88 billion, operating profit reached $1.075 billion and net profit was $2.019 billion. The company significantly reduced operating costs and restored discipline.

Year 2025 accelerated this trend: $11.556 billion in revenue, $1.468 billion in operating profit, and over $2 billion in free cash flow. EBITDA rose to $1.338 billion. This transformed Shopify from a growth but loss-making company into a scalable and highly cash generative business.

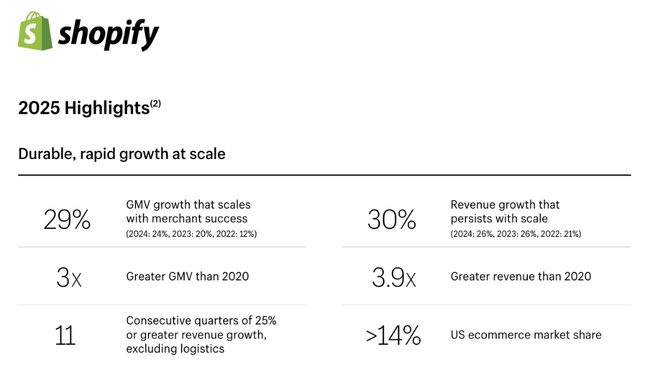

GMV growth from $292 billion in 2024 to $378 billion in 2025 confirms that the platform is gaining market share. The company now holds more than 14% of the US ecommerce market.

News and strategic moves

In addition to strong financial results, Shopify continues to expand its role in the commerce ecosystem. Key drivers include:

36% growth in international sales.

27% growth in offline sales

62% growth in Shop Pay volume

B2B business volume growth of 96%

The company is investing heavily in AI-based tools to simplify store creation, marketing and catalogue management. This helps it build an edge over smaller competitors and traditional platforms.

Shareholding structure

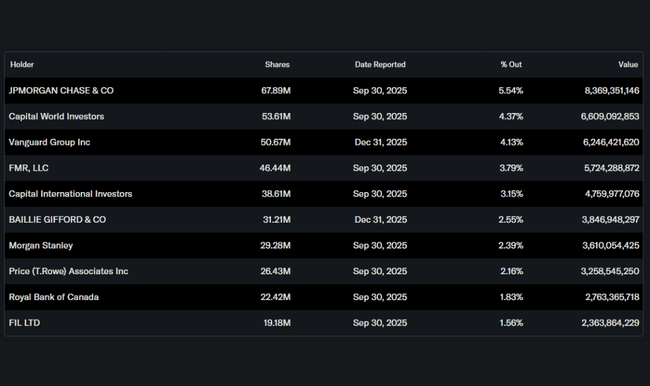

The institution holds approximately 75.5% of the shares. The largest institutional investors are:

JPMorgan Chase with a 5.5% stake,

Capital World Investors with approximately 4.4%,

Vanguard Group with more than 4%,

FMR (Fidelity) with almost 3.8%.

The low share of insiders (0.19%) means that the ownership structure is highly institutional and the stock is sensitive to movements of large funds.

Analysts' expectations

Analysts view Shopify as one of the top growth companies in the digital commerce infrastructure space. The consensus focus is on maintaining revenue growth above 25% annually and gradually expanding operating margins by scaling payment and financial services.

The combination of high growth, robust cash flow and share buybacks is viewed positively. High valuations and sensitivity to a macroeconomic slowdown that could impact merchant volumes remain a risk.