McDonald’s closed 2025 with a quarter that reflects how a global franchise model should perform in a price-sensitive consumer environment. Comparable sales rose solidly, traffic held up, and the system continued to demonstrate scale advantages. Yet the modest post-earnings dip highlights a familiar pattern: good results are quickly reframed through the lens of what happens next when growth inevitably normalizes.

The key takeaway is operational resilience. Global comparable sales increased 5.7%, with US comps up 6.8%, supported not only by higher ticket sizes but also by positive guest traffic. In the quick-service restaurant segment, traffic growth carries particular weight. It signals that value positioning, marketing execution and menu innovation remain effective even as consumers scrutinize spending more closely. With plans to open 2,600 new restaurants in 2026, the focus now shifts to how expansion and same-store momentum translate into sustained earnings growth.

How was the last quarter?

Q4 was a mix of strong demand and very good execution for McDonald's $MCD. Global comparable sales were up 5.7% and US comparable sales were up 6.8%, with management explicitly talking about positive traffic trends. This is important because in recent years many chains have been growing mainly through price and mix, but losing customers at the same time. McDonald's, on the other hand, says it narrowed its "gap" with competitors on visitation levels in the quarter to its best level in a long time.

The bottom line numbers were also solid. Revenue of $7.01 billion was above market expectations and adjusted EPS of $3.12 as well. When translated into investment parlance, this means the company can still monetize the strength of its brand, price and franchise model without having to dramatically "buy" growth through margin-busting discounts.

The fast-food giant reported fourth-quarter net income of $2.16 billion, or $3.03 per share, up from $2.02 billion, or $2.80 per share, a year earlier.

Running in the background is another important thing: the pace of expansion. For all of 2025, the company opened 2,275 restaurants and is targeting an acceleration to about 2,600 gross openings for 2026. That's a key structural driver of system sales growth alongside comparable sales. This keeps McDonald's on a trajectory toward its goal of 50,000 restaurants by the end of 2027.

Management commentary

CEO Chris Kempczinski frames the strategy with the repeated mantra of "three out of three": strong pricing, breakthrough marketing and menu innovation. It's not just a pretty slogan. In the US, management describes that Extra Value Meals packages and other pricing programs were supposed to be successful by two metrics: gaining share of traffic from low-income customers and improving perceptions of affordability. On both counts, they say they got where they wanted to be in Q4, and even gained share with the low-income group in December.

It's also interesting to see management talking openly about franchisee cash flow. Kempczinski says that despite a more aggressive value proposition, U.S. franchisee cash flow improved year-over-year, suggesting that the value proposition was not "underpriced" but well balanced - it pulled in volumes while not destroying restaurant economics.

CFO Ian Borden then highlights digital and loyalty as the most important metric. In the U.S., the company reports roughly 46 million active users in the last 90 days. He described two big campaigns in Q4 specifically: Monopoly, which drove massive digital acquisition, and "Grinch Meal," which he said set records, including the highest sales day ever. These are exactly the moments when McDonald's shows its global marketing "machine" - it can take a brand, pop culture and merchandising and translate that into footfall.

Outlook

The outlook is quite specific in the data even without the classic financial guidance type EPS band. McDonald's is counting on system sales growth to be driven in part by expansion. The company is talking about a contribution of around 2.5% from new restaurant openings alone, with a target of 2,600 new locations for 2026.

On the profitability front, the firm expects operating margins to be in the mid to upper 40% range (within the adjusted metrics McDonald's often uses for its model), and estimates 2026 capital expenditures at roughly $3.7 billion to $3.9 billion. At the same time, management acknowledges that comparable sales growth in Q1 2026 is expected to slow from Q4. That's exactly the type of signal that explains why the stock fell after the results - the market immediately switches from "beat" to "what will the pace look like in future quarters".

Long-term results

Looking at the last four years, McDonald's is an example of a company that can hold very steady profitability while gradually optimizing its cost structure, even as consumer demand fluctuates.

Revenues in 2021 were roughly $23.22 billion. In 2022, they were virtually flat at 23.18 billion, reflecting a more complex macro environment and a phase where consumers have begun to skew more heavily between "I want a brand" and "I want to save". But there was a visible shift in 2023: sales rose to $25.50 billion, up nearly 10% year-on-year, and continued to $25.92 billion in 2024, with a more modest 1.7% growth. In practice, this means that after a post-pandemic jump, the top-line has stabilised and McDonald's has had to work harder with mix, price and footfall.

Gross profit grew consistently: from $12.58 billion in 2021 to $13.21 billion in 2022, $14.56 billion in 2023 and $14.71 billion in 2024. This is important because even with relatively stable sales, the company was able to maintain and increase gross profitability, which in a franchise model is often related to a better mix of fees and higher monetization of digital channels.

The level of operating profit shows how strong operating leverage is in good years. Operating profit was around $10.36 billion in 2021, dropped to $9.37 billion in 2022, but jumped to $11.65 billion in 2023 and held steady at $11.71 billion in 2024. Translated: after a weaker year in 2022, McDonald's returned to a higher profitable level and held it.

Net income and EPS show a very similar story. Net profit was $7.55 billion in 2021, $6.18 billion in 2022, $8.47 billion in 2023, and $8.22 billion in 2024. EPS in 2024 was $11.45 (diluted $11.39). That's important context for today's investor sentiment: McDonald's is not a "turnaround" but a stable cash generator where the market is arguing mainly about what growth rate is realistic in the years ahead.

Another structural layer is working with the share count. The average number of shares has been declining: roughly 746 million in 2021 to 736.5 million in 2022, 727.9 million in 2023 and 718.3 million in 2024. This is typical of a company that returns capital to shareholders over the long term and supports EPS growth even in years when revenue growth is not dramatic.

EBITDA was in the range of approximately $12.18 billion (2021), $10.90 billion (2022), $13.86 billion (2023) and $13.95 billion (2024). Here we can see that 2022 was a weaker year, but since then performance has stabilized at a higher level.

News

There are several recurring themes in the quarter and within management commentary. The first is pricing strategy and perceptions of affordability. McDonald's doesn't want to give way to competitors on who offers the "best value". The second is marketing as a global machine, where big campaigns work across markets and can transfer creative concepts between countries. The third is menu innovation to be more anchored in taste, quality and "McDonald's identity" so that it's not just short promo items with no long-term impact. And the fourth is digital and loyalty, where the company openly says loyalty is a key digital metric and will continue to push for active user growth and engagement.

Shareholder structure

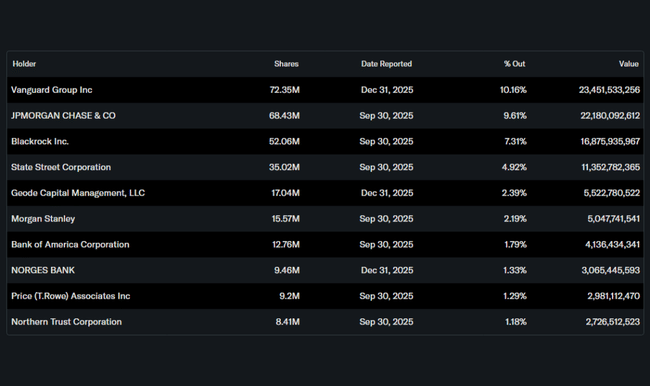

McDonald's is a heavily institutional stock. The institution holds approximately 75.5% of the stock and a similar proportion of the free float. The largest holders include Vanguard (roughly 10.16%), JPMorgan (9.61%), BlackRock (7.31%) and State Street (4.92%). Insider share is low (0.22%), which is typical for a large established corporation.

Analysts' expectations

In this type of quarter, analysts typically address less "did it turn out well" because the numbers were above expectations, and more "what's next." The main lines of debate revolve around three things.

The first is the sustainability of comparable sales growth when management itself admits to a slowdown in Q1 2026. The market will want to see if the value proposition continues to drive traffic or if the effect wears off and it becomes all about pricing.

The second thing is the economics of franchisees. If a company is pushing value and also wants to open new restaurants quickly, the returns must still be attractive to franchisees. Management says franchisee cash flow has been growing even with a stronger value mix, which is a positive sign, but analysts will want confirmation in the quarters ahead.

The third is expansion. 2,600 openings in 2026 is not just a number for a presentation. It's a commitment to capital, capacity, and site selection where returns must still be "McDonald's standard." If expansion succeeds, it will add structural growth to system sales even in an environment of weaker demand. If not, the market will begin to address whether the company is approaching saturation in key regions.