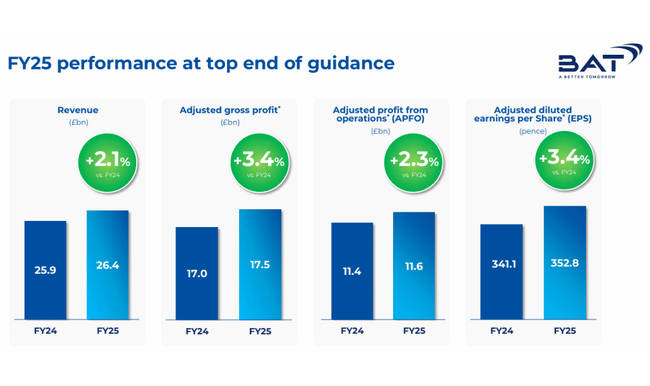

For BAT, 2025 unfolded at two distinct speeds. On one side, the traditional cigarette business continued to generate resilient cash flow in key regions, supported by pricing power and mix. On the other, the transition toward smokeless products proved far from linear, remaining sensitive to regulation, taxation and the impact of illicit trade. Reported revenue declined 1.0% to £25.61 billion at current exchange rates, but increased 2.1% on a constant currency basis. That currency gap is critical: operationally, the company is expanding, even if headline figures suggest otherwise.

The more important shift lies in business quality. BAT added 4.7 million smokeless users, bringing the total to 34.1 million, while smokeless products accounted for 18.2% of group revenue, up 70 basis points year over year. This is no longer just a transformation narrative; it is a measurable and steadily growing share of revenue that is reshaping the earnings profile of the company.

How was the last quarter?

$BTI publishes preliminary results for the full year, but some key trends are evident in just how the firm describes the second half of the year and the regional drivers. In 2025, "new category" momentum improved - particularly modern oral products - while the firm also mined surprisingly strong performance from traditional cigarettes in the U.S. thanks to price and mix. That's the combination investors paradoxically want in tobacco companies: a transformation toward smokeless products, but without breaking up the traditional cash cow faster than the new business can grow.

At constant currencies, group sales grew 2.1%, and the driver was clearly in the US, where sales grew 5.5%. BAT says the US was helped by a combination of a strong price/mix effect in cigarettes, and a very strong ramp-up of Velo Plus, where modern oral products jumped 310% year-on-year to £327m. That's an extremely high rate, which in tobacco often means two things at the same time: firstly the 'launch effect' and rapid share gain, and secondly that the company is investing in promotion and distribution and looking to make this a long-term category.

Vaporizer performance, on the other hand, is the weaker part of the story. The company admits a decline in vaporizer sales, mainly due to the proliferation of illegal products in the US and Canada and also due to regulatory and tax changes in some European countries. This is important because vaporizers have historically been seen as the main "alternative" to cigarettes. BAT is now effectively saying: our Vuse product has good potential in the long term, but in the short term the category is distorted by the illicit market and without better enforcement of the rules we cannot expect smooth growth.

Top points:

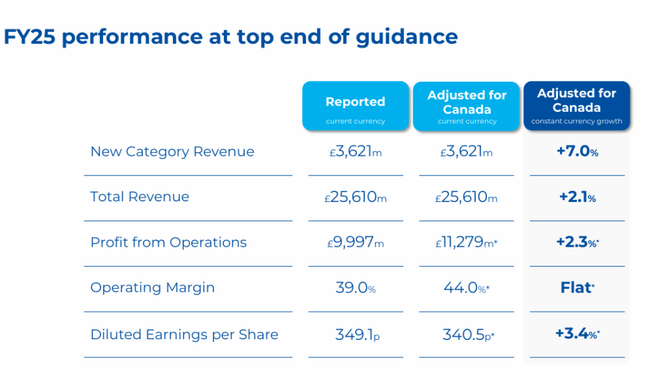

Revenue: £25.610bn.

-1.0% YoY

+2.1% at constant exchange rates

New categories - revenue: £3.621bn.

+7.0% at constant exchange rates

Smokeless products as a proportion of sales: 18.2% (+70bps)

Operating profit (reported): £9.997bn.

+265 %

Adjusted operating profit: +2.3%

Reported operating margin: 39.0%

Adjusted operating margin: 44.0% (stable y/y)

Earnings per share (diluted EPS, reported): 349.1p

+157 %

Adjusted earnings per share: +3.4%

Net cash flow from operations: £6.342bn

CEO comment

Tadeu Marroco is building the whole 2025 story on "accelerating momentum" and the fact that the company delivered results at the top end of its outlook. In practice, this is communication like: we have the traditional part of the business under control, growth and margins are improving in smokeless products, and cash is giving us room to both invest and pay out.

What he says is most valuable is a specific detail from the US: the Velo Plus had triple-digit sales growth, the Velo brand was second in volume and value share and - crucially for the market - achieved 'categorical profitability' within a year of launch. This suggests that it is not just a costly acquisition phase, but that the product can generate a profit contribution relatively quickly.

With Vuse, the tone is more cautious but structured: the performance improvement is encouraging, it's just that the whole segment is hampered by illegal supply. Marroco is essentially betting that, in time, tougher enforcement of rules will come at the federal and state level, and legal players will benefit. That's a significant "regulatory bet": without it, vaporizer growth may stall further.

Regionally, the CEO says AME (Americas and Europe) continues to pull more product categories, while APMEA (Asia-Pacific, Middle East, Africa) has been hit by fiscal and regulatory issues in Bangladesh and Australia.

Outlook for 2026

The outlook is written fairly straightforwardly, and at the same time the firm has its back: it expects to perform at the lower end of its medium-term outlook.

For 2026, BAT expects global cigarette market volume to fall by around 2%. Yet it is targeting constant-currency sales growth of 3-5%, with new category sales expected to grow at a low double-digit rate. Operating profit on an adjusted basis is expected to grow 4-6% and be "second half of the year stronger than the first", which usually means that some of the investment and costs will come earlier and the benefit will come later. Adjusted earnings per share is expected to grow 5-8%, but again at the lower end.

Currency-wise, the company says outright that it expects about a 1% negative impact of the transaction rate on earnings and about a 3% headwind to adjusted EPS growth from currency translation. This is exactly the type of thing that may seem like a detail, but for a global firm, it often determines whether or not the headline numbers "look good" even though the operating reality is fine.

From a balance sheet perspective, the important thing is the commitment to reduce debt to the 2.0-2.5× net debt to EBITDA range by the end of 2026. The company is currently around 2.48×, so already virtually inside the target, and plans to achieve this thanks to very high operating cash conversion, where it is targeting over 95%. That's more important to the dividend title than one-time revenue growth percentage: the ability to generate cash while keeping leverage in check.

Long-term results

The four-year track record confirms the company's structurally strong but accounting-volatile profile. Revenues rise from GBP25.684bn in 2021 to GBP27.655bn in 2022, then fall slightly to GBP27.283bn in 2023 and GBP25.867bn in 2024. Gross profit holds steady above GBP21bn. GBP 21.087 billion in 2021, GBP 22.851 billion in 2022, GBP 22.392 billion in 2023 and GBP 21.431 billion in 2024, reflecting the strong pricing and high margin of the traditional tobacco business.

The largest fluctuations are at the level of operating and net profit. Operating income was GBP 10.234 billion in 2021 and GBP 10.523 billion in 2022, but fell to - GBP 15.751 billion in 2023 due to massive exceptional items, before returning to positive territory in 2024 at GBP 2.736 billion. We see the same picture for net profit: GBP 6.801 billion in 2021, GBP 6.666 billion in 2022, a loss of GBP -14.367 billion in 2023 and a return to profit of GBP 3.068 billion in 2024. This confirms that it is crucial to separate structural operating performance from accounting one-offs when assessing BAT.

What has really changed in the mix of the business in 2025

The strongest structural signal is the shift in smokeless products to 18.2% of sales and growth in users to 34.1 million. This is important for three reasons. Firstly, it increases the share of growth categories in total sales, reducing the reliance on declining cigarette volumes. Second, the company explicitly says it is investing in the most profitable markets and the priority is to grow profit contribution, not just chase sales. And third, 'new categories' are no longer just an expense but are starting to be a significant profit chapter - category contribution from new categories rose 77% to £442m and contribution margin rose to 11.8%.

This is exactly the point at which the transformation changes from marketing story to accounting reality: revenue growth is fine, but profit contribution growth is what can protect the dividend and buybacks in the long term.

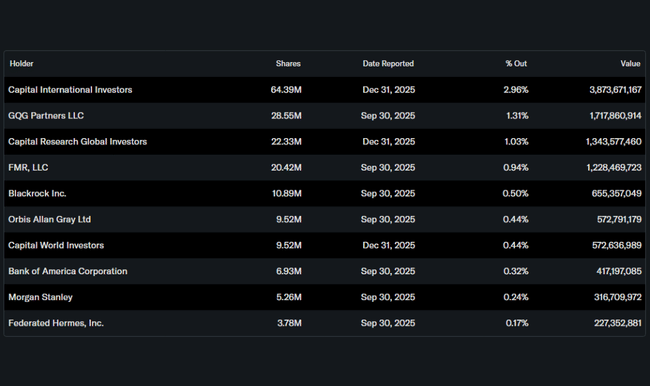

Shareholder structure

Compared to US blue chips, BAT is less "institutionally loaded". Institutions hold roughly 13.5% of the stock, insider holdings are minimal. The largest institutional holdings include Capital International Investors (c. 2.96%), GQG Partners (1.31%), Capital Research Global Investors (1.03%) and FMR (0.94%). For UK titles, this is often related to the holding structure through various nominee accounts and specifics of recordkeeping, but the point for investors is more practical: the exchange rate may be more sensitive to capital flow with a smaller "hard" institutional core than is common with, say, Coca-Cola.

Capital allocation and shareholder return

BAT for 2026 confirms two things that dividend investors want to hear: dividend growth and buybacks. The dividend per share is rising 2% to 245.04 pence, while the firm plans a £1.3bn share buyback in 2026. To this it adds a commitment to get debt into the 2.0-2.5x target range by the end of 2026 and to hold a very high cash conversion. This is the typical "cash return" profile of tobacco companies: earnings growth tends to be moderate, but return on capital is the main investment thesis.

What to watch in 2026

Most importantly, there are three specific monitoring points that tell us if the investment thesis is being met.

The first is the growth rate of advanced oral products, particularly in the US, not just at the level of sales but at the level of profit contribution. If Velo maintains a high pace while improving profitability, it will be the fastest way to move the smokeless mix towards a higher share.

The second thing is the Vuse vaporizer and the evolution of the illicit market. This is not so much about marketing as it is about regulatory enforcement. Once the market starts to clear of illegal products, the legal players have a chance to step up. If that doesn't happen, vaporizers may remain the weak link.

The third is APMEA and regulatory risk. The company itself says Bangladesh and Australia hurt it in 2025. If the environment stabilises, the region may make a partial comeback. If not, it will continue to hamper consolidated growth.