EV investing has quietly shifted from “who can grow deliveries fastest” to “who can survive the economics.” Price cuts, high fixed costs, and brutal manufacturing learning curves have made it clear that not every automaker gets to scale into profitability on schedule — and the market is increasingly willing to reward any credible path that improves gross profit, even if it’s not driven by the vehicles themselves.

Rivian’s Q4 2025 closes the year with a notable step forward: full-year consolidated gross profit turned positive at $144 million versus a $1.2 billion loss a year earlier, and Q4 delivered $120 million of gross profit. But the report also underlines the company’s split personality — automotive remains structurally under pressure and highly sensitive to pricing discipline and cost optimization. For investors, the hinge is the transition from the R1 platform to the upcoming R2, with first customer deliveries targeted for Q2 2026, while software and services — amplified by the Volkswagen Group joint venture — increasingly look like the margin engine that could change what “Rivian profitability” actually means.

Quarterly results

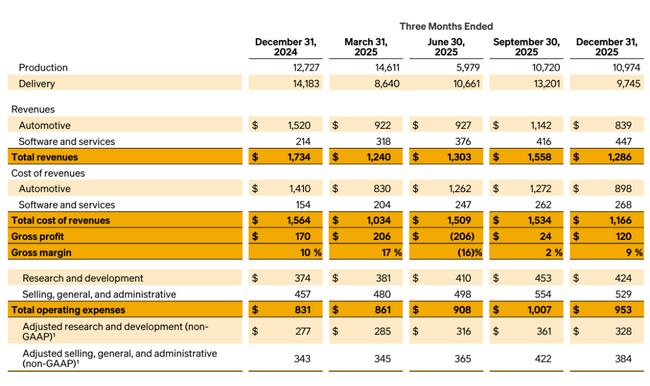

In the fourth quarter of 2025, Rivian $RIVN produced 10,974 vehicles and delivered 9,745 vehicles to customers. Consolidated revenue was $1.286 billion, down from $1.734 billion in the same period in 2024. The main reason was the decline in revenue from the automotive segment, which fell 45% year-over-year to $839 million.

The decrease was primarily driven by lower regulatory credits, which declined $270 million year-over-year, lower shipment volumes due to the expiration of tax incentives, as well as a lower average selling price due to a higher proportion of electric EDVs.

In contrast, the software and services segment accelerated significantly. Sales here rose 109% year-on-year to $447 million, mainly due to the development of electric architecture and software in collaboration with Volkswagen, but also due to remarketing and service.

Group gross profit was USD 120 million. However, the automotive division posted a gross loss of US$59 million, compared to a profit of US$110 million in Q4 2024. Software and services, on the other hand, generated a gross profit of US$179 million, almost triple that of last year. This shows that without the software segment, the quarter would have been deeply in the red again.

Full Year 2025 Results

For the full year, Rivian produced 42,284 vehicles and delivered 42,247 units. Consolidated sales rose 8% to $5.387 billion.

Automotive sales declined 15% year-over-year to $3.83 billion, driven by lower regulatory credits and lower shipment volume. This was partly offset by higher average selling prices and a higher proportion of R1 models.

Software and services saw dramatic growth of 222% to $1.557 billion. This segment is becoming a strategic pillar of the entire company.

Most significant is the shift at the gross profit level. While Rivian reported a gross loss of $1.2 billion in 2024, it has already achieved a positive gross profit of $144 million in 2025. The automotive segment remains in the red (-432 million USD), but significantly better than the -1.207 billion USD in 2024. Software and services generated 576 million USD in gross profit.

Management commentary

Founder and CEO RJ Scaringe emphasized that 2025 was all about execution and preparing to scale. He said the company has laid the foundation for dramatic growth with its R2 platform and its own autonomous chip, RAP1, unveiled at Autonomy & AI Day.

Management points to very positive early reviews of pre-production versions of the R2 and expects first customer deliveries in Q2 2026. The R2 is intended to be a significantly more affordable model that will enable entry into the mass market segment.

Outlook

A major milestone in 2026 will be the rollout of the R2. The company has completed a validation series with production tools and processes and confirms that the schedule remains unchanged.

Strategically, Rivian seeks to combine vertical hardware integration with a strong software and autonomous platform. If R2 can be launched without major production complications while continuing to expand software revenue, margins could improve significantly.

Long-term results

A look at the 2022-2025 period shows a gradual stabilization but still a very challenging path to profitability. Revenues grow from $1.658 billion in 2022 to $5.387 billion in 2025, more than tripling. However, the growth rate is gradually slowing, which is natural with a higher base.

The biggest improvement is seen at the gross margin level. The gross loss of USD 3.123 billion in 2022 has gradually reduced and the company has already achieved a positive gross profit of USD 144 million in 2025. This shift is a result of higher selling prices, optimization of manufacturing costs, and an increasing share of high-margin software.

However, the operating loss remains high. While it has declined from -$6.856 billion in 2022 to -3.585 billion in 2025, the company is still burning significant capital. So the improvement is noticeable, but the road to operating profit is still long.

Net loss is gradually declining from -$6.752 billion in 2022 to -3.646 billion in 2025. EPS has improved from -$7.40 to -3.07, but at the same time there is significant dilution, with the number of shares increasing from 913 million in 2022 to 1.186 billion in 2025.

So from a macro perspective, Rivian stands between two worlds - no longer a revenue-less startup, but still not a profitable manufacturer.

Shareholder structure

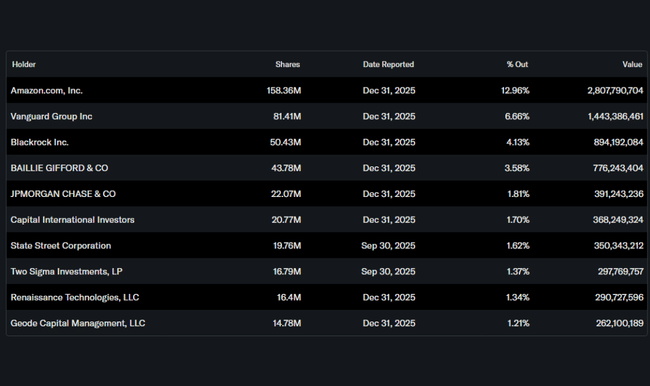

Rivian has a strong insider participation, which amounts to 33.68% of the shares, signaling significant involvement of management and founders. The institution holds approximately 45.5% of the stock and nearly 69% of the free float.

Amazon is the largest shareholder with a stake of approximately 12.96%, underscoring the strategic link between the two firms. Vanguard (6.66%) and BlackRock (4.13%) also hold significant stakes. Amazon's presence is key not only in terms of capital but also commercially thanks to its fleet of electric EDVs.