Rise or fall?📈📉

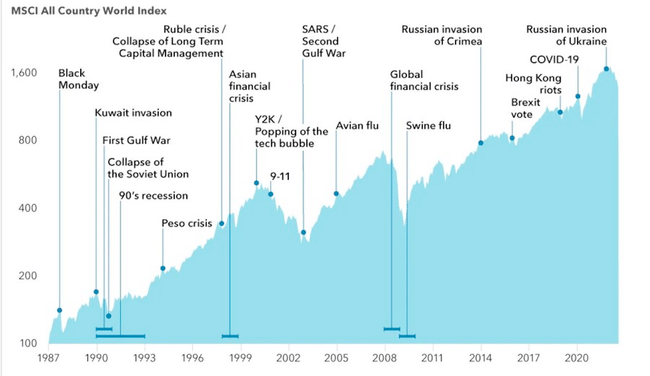

Financial markets over the past nearly 40 years have survived almost everything: Black Monday in 1987, the collapse of the Soviet Union, the Asian financial crisis, the bursting of the dot‑com bubble, the September 11 attacks, the global financial crisis of 2008, Brexit, the Covid‑19 pandemic, and the war in Ukraine. Yet the MSCI All Country World index has trended upward over the long term.

This chart nicely illustrates one of the most important lessons of investing: short‑term crises occur regularly, but the long‑term trend in equity markets remains upward.

Each of these events looked like a major problem for the global economy at the time, but markets ultimately managed to recover. It's important to remember that.

And now a bit of history...

At the end of the 1980s markets were hit by the so‑called Black Monday in 1987, when U.S. stocks fell by more than 20% in a single day. The Dow Jones $^DJI lost 22.6% of its value that day. It remains the largest percentage drop in history.

A few years later came Iraq’s invasion of Kuwait and the first Gulf War, which brought significant volatility to commodity and equity markets. In the early 1990s the collapse of the Soviet Union and an economic recession in the United States followed. Each of these events raised concerns about the stability of the global economy at the time.

Another major wave of turbulence arrived in the late 1990s. The Asian financial crisis in 1997 caused sharp declines in currencies and equities across several emerging economies and then spread to global markets. Shortly after came the collapse of the hedge fund Long‑Term Capital Management, which threatened the stability of the financial system. At the turn of the millennium the bursting of the tech dot‑com bubble followed, during which the Nasdaq lost more than half its value over a few years.

The start of the new millennium was not peaceful either.

The terrorist attacks of September 11, 2001 led to an immediate market drop and significantly increased geopolitical uncertainty.

One of the biggest tests for the financial system was the global financial crisis in 2008. The collapse of Lehman Brothers triggered a chain reaction across financial markets and indices around the world plunged by tens of percent in a short time. At the time there were scenarios predicting a long‑term collapse of the financial system. Nevertheless, markets gradually stabilized in the following years and entered one of the longest bull runs in modern history—which, incidentally, continues to this day. That alone tells us that being pessimistic about equity markets does not pay off in the long run.

The last decade was no calmer. Markets had to react to geopolitical tensions around Russia’s annexation of Crimea, the Brexit referendum, and the Covid‑19 pandemic. The pandemic in 2020 caused one of the fastest market collapses in history. Yet global indices managed to recover in a relatively short time and later reached new all‑time highs.

What matters

The chart shows one of the most important characteristics of equity markets. Short‑term shocks, geopolitical conflicts, or economic crises are a natural part of investing. Each of these events looks like a serious threat to the global economy at the moment, but the long‑term development shows that markets can adapt over time and return to growth.

The current situation—even if the level of conflict were to widen—could easily cause equities to fall by tens of percent. However, history clearly shows that within a few years markets have always recovered and even surpassed previous highs.

Bulios Black

This user has access to exclusive content, tools and features of the Bulios platform thanks to their subscription.

A lot is happening right now, but I don't expect a bear market or any extreme moves. I'm sticking to my strategy and holding stocks for the long term.

Bulios Black

This user has access to exclusive content, tools and features of the Bulios platform thanks to their subscription.

Volatility is increasing year by year and investors are becoming more sensitive, but that doesn't change anything and can be put to good use. If a larger correction comes, I'll gladly buy more.

Bulios Black

This user has access to exclusive content, tools and features of the Bulios platform thanks to their subscription.

What many today consider an unshakeable truth about the perpetual rise of stocks is actually a classic example of selection bias based on a very specific recent 40 years. If we look before 1980, we see a completely different picture—for example, investments from the 1960s only reached a real (inflation‑adjusted) profit after long two or three decades. That 'golden era' was driven by a unique combination of factors that may not repeat: the drastic fall of interest rates from 15% to almost zero, a massive inflow of fresh capital thanks to American 401(k) pension plans, and the advent of personal computers, which sharply increased corporate margins. Relying on these extraordinary conditions to last forever is therefore a very risky bet on the past.

Today we are in a diametrically different situation: the era of 'TINA' (There Is No Alternative) has ended, and safe government bonds are beginning to genuinely compete with equities, which naturally drains liquidity from the market. Higher interest rates also logically reduce the present value of future earnings, so investors are no longer willing to pay as high multiples for stocks as before. The whole world has grown accustomed to cheap money over the past decade, but in a high‑rate environment more weak companies may start to fail and record government debt will continue to hinder investment and overall GDP growth. Instead of endless optimism, we should prepare for the possibility that future returns may rest on much more fragile foundations than those we have been used to.