In the final quarter of 2025, NIO delivered 124,807 electric vehicles and lifted revenue to roughly 4.96 billion dollars, marking year-on-year growth of nearly three quarters as record volumes and improved product mix pushed the company into its first-ever quarterly profit. Although the full year remained loss-making, the return to positive operating and net income in Q4 underscores how rising scale and better gross margins can gradually shift the economics of NIO’s premium and mass-market EV lineup.

For investors, the key takeaway is the combination of rapid expansion across the NIO, ONVO and FIREFLY brands and visible cost discipline, which together drove margins to their highest level in several years. Management’s guidance for the first quarter of 2026 points to another period of triple-digit revenue growth and nearly doubled deliveries, but the company still faces heavy capital needs, intense price competition from BYD, Tesla, Li Auto and XPeng, and ongoing sensitivity to China’s demand cycle and policy shifts.

How was the last quarter?

In Q4 2025, $NIO delivered 124,807 vehicles, a jump of 71.7% vs. Q4 2024 and 43.3% vs. Q3 2025. The growth was not a one-off, but spread across three brands: premium NIO(67,433 vehicles), family-oriented ONVO(38,290 vehicles) and smaller premium FIREFLY(19,084 vehicles), with all three hitting record levels. This shows that scaling the business is not dependent on one model, but on a portfolio across price segments.

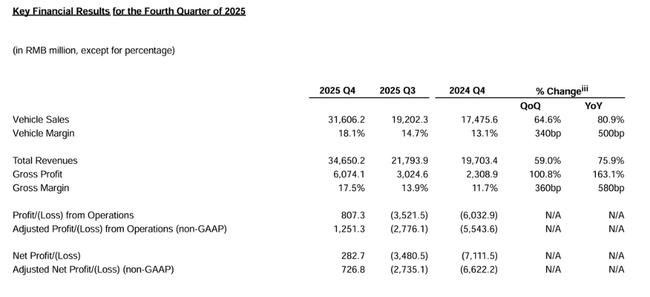

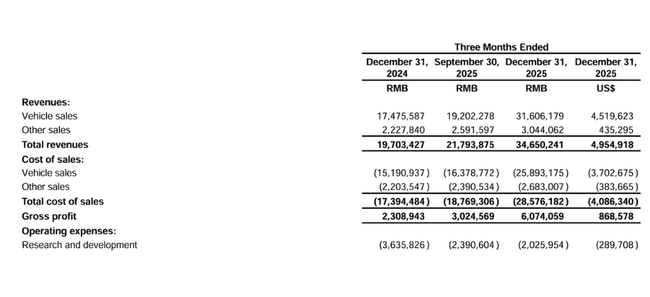

Total sales reached 34.65 billion yuan, or roughly $4.96 billion, up +75.9% year-on-year and +59.0% quarter-on-quarter. Car sales alone were 31.61 billion yuan, approximately $4.52 billion, and grew even faster than total sales, reflecting both higher volume and higher average selling price due to a more favorable model mix. Other sales (e.g., services, parts, research services, used cars) totaled 3.04 billion yuan, or about $435 million, and grew at a slower but still double-digit rate.

Gross profit in the quarter was 6.07 billion yuan, about $0.87 billion, up 163.1% year-on-year and doubling quarter-on-quarter. Gross margin jumped to 17.5% from 11.7% a year ago and 13.9% in Q3. The key driver is vehicle margin, which improved to 18.1% from 13.1% in Q4 2024 and 14.7% in Q3 2025, thanks to more premium models (e.g. All-New ES8, ONVO L90) and material cost reduction effects. This shift is structural: it comes from a combination of production scaling, internal technology development and supply chain optimization.

Operating costs (R&D, sales, marketing and administration) were under strong control in Q4 2025. R&D expenses fell to 2.03 billion yuan, about $290 million, down 44.3% year-on-year and 15.3% quarter-on-quarter, mainly due to "organizational optimization" and lower development costs in later-stage projects. Adjusted R&D expenses (excluding stock-based compensation and one-time restructuring costs) were 1.74 billion yuan, about $250 million.

Selling, general and administrative expenses were 3.54 billion yuan, about $506 million, down 27.5% year-over-year and 15.5% quarter-over-quarter. Adjusted SG&A expenses were 3.39 billion yuan, approximately $485 million. The decline is again driven by a reduction in support staff and lower marketing spend - this is a structural change in the cost base, although some of the savings may be cyclical (less aggressive campaigns).

The result is an operating profit of 807.3 million yuan, about $115 million, versus a loss of 6.03 billion yuan a year ago and 3.52 billion yuan in Q3. Adjusted operating profit excluding stock awards was 1.25 billion yuan, about $179 million, the first positive quarter in NIO's history and an important milestone on the road to sustainable profitability.

Net profit for Q4 2025 was 282.7 million yuan, approximately $40 million, compared to a net loss of 7.11 billion yuan in Q4 2024 and 3.48 billion yuan in Q3 2025. Adjusted net profit excluding stock awards and one-time expenses was 726.8 million yuan, approximately $104 million. Earnings per share (basic and diluted) for the quarter were 0.05 yuan, or about $0.01, while adjusted earnings per share were 0.29 yuan, about $0.04.

From a cash flow and balance sheet perspective, the company had 45.9 billion yuan in cash, restricted cash, short-term investments and time deposits, or about $6.6 billion, as of December 31, 2025. While NIO achieved positive operating cash flow in both the third and fourth quarters of 2025, it remained in the red for the full year, and self-reported current liabilities exceed current assets - meaning its liquidity position is ample but tight and dependent on continued revenue growth and the availability of credit lines.

Management commentary

CEO William Bin Li highlighted that deliveries were up 71.7% in Q4 2025 and that all three brands achieved record numbers, with full year deliveries of 326,028 vehicles representing growth of 46.9%. Between the lines, this tells investors that the multi-brand strategy is working and that the company can build relevant share in each segment (premium SUV, family SUV, small city car) despite strong competition.

The CEO also announces continued mass deployment of proprietary smart car technologies, investment in battery swapping and charging, and expansion of the sales and service network. The tone is confident, focused on growth and technological superiority, although the company is aware of the need for better profitability - the mention of targeting "twelve key technologies" suggests that NIO does not want to significantly reduce R&D, but rather do it more efficiently.

CFO Stanley Yu Qu highlighted the improvement in margins - 18 .1% margin on vehicles and 11.9% margin on other sales - and the first positive adjusted operating profit of 1.25 billion yuan. The CFO's tone is more disciplined - promising further efficiency gains and cost optimization in 2026 to be the main driver of sustainable profits.

Outlook

For the first quarter of 2026, NIO expects deliveries of 80,000-83,000 vehicles, equivalent to a year-on-year growth of roughly 90.1-97.2%. Total sales are expected to reach 24.48-25.18 billion yuan, or approximately $3.50-3.60 billion, representing a year-on-year growth of 103.4-109.2%. Thus, the outlook is for continued very rapid growth in volume and sales, although the absolute level is seasonally lower than the Q4 peak - which is normal for an automaker.

The company does not explicitly disclose margin targets or profit expectations in this outlook, but given the gross and vehicle margins achieved in Q4, we can expect management to target at least maintaining double-digit margins and further improving operating profitability. The outlook looks rather optimistic to aggressive, as it assumes more than double the sales growth from a weaker Q1 2025; this growth is based on the continued success of new models and that the Chinese EV market will remain strong despite the price war and possible change in subsidies.

The firm also cautions that the outlook reflects its current view of the business environment and that it is subject to change - i.e. it does not include shock scenarios (such as a sharp market slowdown, new export tariffs or major regulation) that could negatively impact results.

Long-term results

For the full year 2025, NIO achieved sales of 87.49 billion yuan, or ~$12.51 billion, an increase of 33.1% from 2024, when sales were 65.73 billion yuan (~$9.15 billion at a similar exchange rate). This builds on previous years, when sales grew by roughly 12.9% in 2023 and 36.3% in 2022, from 36.14 billion yuan in 2021. NIO has thus systematically scaled its volume over the past four years, although the growth rate fluctuates according to the phase of the model cycle and the situation in the Chinese EV market.

However, the cost base has long grown faster than sales. The cost of goods sold rose from 29.31 billion yuan in 2021 to 44.12 billion yuan in 2022, 52.57 billion yuan in 2023 and 59.24 billion yuan in 2024 before reaching 75.57 billion yuan (about $10.81 billion) in 2025. Still, gross profit improved: from 6.49 billion yuan in 2024 (~$0.94 billion) to 11.92 billion yuan in 2025 (~$1.70 billion), a growth of 83.5% and a gross margin shift from 9.9% to 13.6%. This is a structural change - NIO was able to lift margins despite price competition, indicating a combination of premium positioning on select models and improved efficiency.

Operating costs (R&D, sales, marketing and administration) have been the main reason for massive losses in recent years. It was 28.37 billion yuan in 2024, 25.71 billion yuan in 2023 and 20.78 billion yuan in 2022, while it was 11.32 billion yuan in 2021. In 2025, R&D expenses decreased to 10.61 billion yuan (~$1.52 billion) by roughly 18.7%, while adjusted (excluding stock awards and one-time items) they decreased to 9.09 billion yuan (~$1.30 billion). Selling and administrative expenses rose only slightly to 16.09 billion yuan (~$2.30 billion) and adjusted were 15.22 billion yuan (~$2.18 billion), almost unchanged from 2024.

Despite these savings, the operating result for 2025 was still a loss: -14.04 billion yuan, or ~$2.01 billion, although this was a 35.8% improvement over 2024 (when the loss was -21.87 billion yuan). Adjusted operating loss decreased to -11.51 billion yuan, about $1.65 billion, from -19.95 billion yuan in the previous year. At the net income level, the firm reported a loss of -14.94 billion yuan (~-$2.14 billion) in 2025, versus -22.66 billion yuan in 2024, an adjusted -12.41 billion yuan (~-$1.78 billion).

Earnings per share (EPS) were significantly negative from 2021-2024: -6.72, -8.89, -12.44, and -11.03 yuan per share, respectively; full-year EPS improved to -6.85 yuan, or ~$0.98, in 2025, adjusted -5.47 yuan (~$0.78). Meanwhile, the number of shares increased significantly from 1.57 billion in 2021 to 1.64 billion in 2022, 1.70 billion in 2023 and 2.06 billion in 2024, so investors faced significant dilution. This is a consequence of the capital-intensive model, with NIO repeatedly issuing new shares to fund expansion - structurally, the higher share count means that even as profitability improves, it will take longer to get EPS well above zero.

Operating leverage only starts to kick in in 2025. In previous years, operating costs often grew faster than sales, mainly due to development and marketing expansion, leading to deepening losses (operating loss of -4.50 billion yuan in 2021, -15.64 billion in 2022, -22.66 billion in 2023, -21.87 billion in 2024). But in 2025, NIO combines double-digit sales growth with a decline in research costs and stabilization of sales costs, leading to a clear improvement in loss and the first profitable quarter. This is a structural shift - the company is moving from a "growth regardless of profit" phase to one where growth is accompanied by efficiency pressures.

EBIT and EBITDA show a similar trend. EBIT for 2024 was -21.63 billion yuan, while EBITDA was -13.93 billion yuan; in previous years, EBITDA fell from -985 million yuan in 2021 to -10.05 billion yuan in 2022 and -15.15 billion yuan in 2023. Although the detailed 2025 EBIT/EBITDA figures are not fully broken down in the report, the combination of improved gross margins, reduced operating expenses and a positive Q4 makes it clear that EBITDA is well on its way to breakeven - a key milestone for a capital-intensive carmaker on its way to sustainable financing without further dilution.

News

NIO is strengthening its technology and capital base in 2025 and early 2026. In February 2026, its smart driving chip subsidiary Shenji received a 2.257 billion yuan cash deposit from investors in China in exchange for newly issued shares, with NIO retaining a 62.7% stake after the transaction. In doing so, the company is both monetizing part of its technology platform and reducing the capital burden of chip development, while retaining control of a key technology that could be the differentiator against competitors.

In addition, in December 2025 and January 2026, NIO bought about 1.08% stake in NIO China from some investors for a maximum of 1.002 billion yuan to increase its controlling stake to an expected 92.9%. This increases the influence of the parent company on the most important operation and simplifies the structure of the group, which is important for any further financing or partnership.

Also crucial is the approval of performance share awards for CEO William Bin Li: under the 2026 plan, he has been granted 248.45 million restricted stock units, divided into ten tranches, the vesting of which is linked to market capitalisation and net profit targets. This increases the alignment of management's interests with shareholders, but also represents future dilution; investors should monitor how quickly these targets are achieved and how the number of shares outstanding evolves.

Shareholding structure

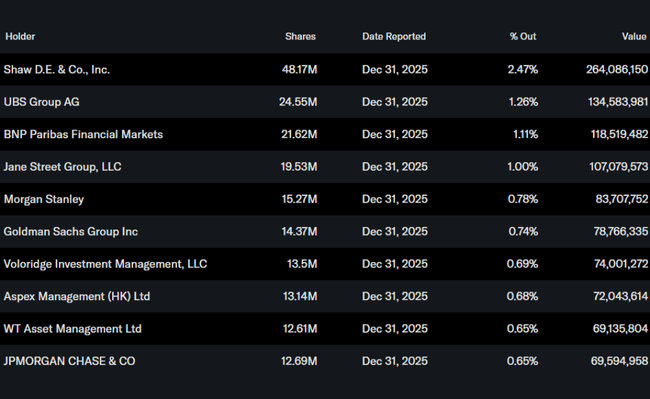

Insiders hold approximately 2.11% of the shares, institutions hold approximately 14.78% of the total, and institutional investors hold approximately 15.09% of the free float, with 555 institutions holding shares. The largest institutional holders at the end of 2025 include D. E. Shaw & Co. with 48.17 million shares (~2.47%), UBS Group with 24.55 million shares (~1.26%), BNP Paribas Financial Markets with 21.62 million shares (~1.11%), and Jane Street Group with 19.53 million shares (~1.00%). Thus, the structure is a combination of smaller insider holdings, significant but not dominant institutional holdings, and large retail and "other" holdings, which means the stock is sensitive to changes in market sentiment and capital flow from index and theme funds.