In fiscal Q2 2026, Micron reported results that underline how deeply the AI boom is reshaping the memory market, with revenue surging to about 23.9 billion dollars and profit in the mid teens billions as prices and volumes for data center memory jumped together. Gross margin expanded into the mid 50s and beyond on the back of scarce high bandwidth memory capacity and strong DRAM pricing, pushing earnings to levels that would have looked unrealistic just a few quarters ago.

From an investment perspective, Micron still operates in a highly cyclical industry that historically swings between acute shortages and painful oversupply, but the current phase looks like a full blown “supercycle” powered by AI workloads, with most forecasts showing demand exceeding supply through at least 2026. The key question for shareholders is how long the mix of strong AI driven demand and disciplined industry supply can last before new megafabs in the U.S., Korea and Taiwan come online and start to normalise margins and returns.

What was Q2 2026 like?

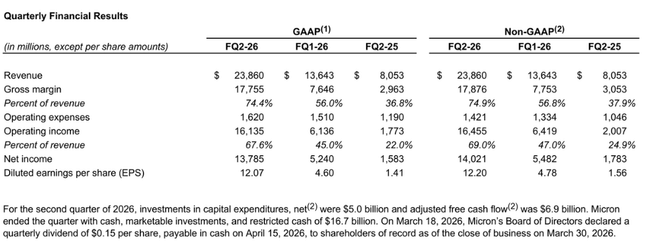

Revenue in the second fiscal quarter of 2026 was $23.86 billion, up from $13.64 billion in the previous quarter and $8.05 billion a year ago. This puts quarter-on-quarter growth at over 70%, and year-on-year revenue nearly tripled - the result of a combination of sharp growth in memory prices and very strong uptake, particularly in AI-related segments.

Gross profit jumped to $17.76 billion with a gross margin of around 74-75%, compared to less than 37% a year ago. GAAP operating profit was $16.14 billion, which equates to an operating margin of about 68%; adjusted operating profit of about $16.46 billion implies an even slightly higher margin. Meanwhile, a year ago, Micron $MU was around 22-25% operating margin - so this is a significant shift, driven primarily by the extraordinary pricing environment.

GAAP net income was $13.79 billion, adjusted net income was $14.02 billion. Earnings per share were $12.07 (GAAP) and $12.20 (adjusted), compared to $4.60-$4.78 in the prior quarter and only about $1.41-$1.56 a year ago.

Operating cash flow was $11.90 billion, up significantly from $8.41 billion in Q1 and $3.94 billion a year ago, and adjusted free cash flow was $6.9 billion. Capital expenditures after accounting for government incentives are roughly $5 billion, a high number, but in the context of booming demand and plans to expand production, this is consistent with efforts to "lock in" capacity for AI generation. At the end of the quarter, Micron had about $16.7 billion in cash and investments, so net debt is well manageable given the size of earnings and cash flow.

The company also announced a quarterly dividend of $0.15 per share, payable in April 2026 to shareholders of record at the end of March. While this is a relatively small amount in the context of current earnings, management frames it as a signal of confidence in the sustainability of the cycle, which may be an important psychological factor for some investors.

Segments.

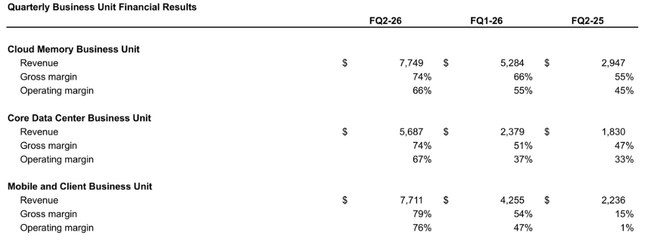

The Cloud Memory Business Unit generated revenue of roughly $7.75 billion, up from $5.28 billion in Q1 and $2.95 billion a year ago. The segment's gross margin was around 74% and operating margin was around 66% - exceptionally high figures, driven by a combination of industry-leading AI server products and limited capacity availability across the industry.

The "Core" datacenter division had sales of about $5.69 billion, versus $2.38 billion in Q1 and $1.83 billion a year ago, with a gross margin of about 74% and an operating margin of about 67%. This shows that demand for server memory (not just pure AI, but high performance computing in general) is very strong and customers are willing to pay significantly higher prices for reliable supply.

The Mobile and Client Business Unit (MCBU) segment had revenues of approximately $7.71 billion, up from $4.26 billion in Q1 and $2.24 billion a year ago. The gross margin here is around 79% and the operating margin is around 76%, which is a huge turnaround from just one percent operating margin a year ago. This is related to both the recovery in demand for phones and PCs, and the shift to higher density and performance memories where Micron can collect premium prices.

The automotive and embedded segment generated sales of around $2.71 billion, up from $1.72 billion in Q1 and $1.03 billion a year ago. Gross margin was about 68% and operating margin was about 62%, up significantly from about six percent a year ago - the automotive world is rapidly filling up with memory and storage for assisted driving, infotainment and other smart features, and with the current capacity shortage, this is another source of very profitable growth.

Management comment

Sanjay Mehrotra, CEO and Chairman, termed the Q2 results as new records in sales, gross margin, earnings per share and free cash flow and stressed that he expects similar records in the third fiscal quarter as well. The key message is that the combination of a "strong demand environment, tight supply within the industry and good execution" has created an extremely favorable environment in which memory is becoming a strategic asset for customers in the AI era.

Mehrotra also mentions that Micron is investing in its global manufacturing base to meet growing demand, and that the 30 percent dividend increase reflects confidence in a "consistently strong" business. The tone is very confident, but management also refers to the risks in materials for the Securities and Exchange Commission (SEC), noting the traditional cyclicality of the memory business and other potential factors that could slow the current boom.

Outlook

For the third fiscal quarter of 2026, Micron expects revenue of around $33.5 billion, with a tolerance band of plus or minus $750 million. This marks another significant increase from an already record Q2, and confirms the company's confidence in the continuation of an extremely strong demand cycle, particularly from AI datacenters.

Gross margin is expected to be around 81%, even higher than Q2, and operating expenses are expected to be around $1.6 billion on a GAAP basis and $1.4 billion on an adjusted basis. Earnings per share are expected to be approximately $18.90 ± $0.40 on a GAAP basis and $19.15 ± $0.40 on an adjusted basis. At a diluted share count of around 1.14-1.15 billion, this is an extraordinary level of profitability, approaching the levels of the most profitable semiconductor companies in history.

Management notes in its outlook comments that this scenario is based on continued strong demand for AI memories, disciplined supply in the industry, and the assumption that there will be no sudden overheating of customer investments.

Long-term results

Over the past four fiscal years, Micron has gone through the classic memory boom-bust-boom cycle. It had sales of around $30.76 billion in 2022, dropped to around $15.54 billion a year later, recovered to $25.11 billion in 2024, and shot up to $37.38 billion in 2025. Gross profit even went slightly negative in 2023 (a loss at the gross profit level) as memory prices fell below fully allocated costs; by 2024, gross profit was already around $5.61 billion and jumped to $14.87 billion in 2025.

Operating profit was very strong in 2022, fell into a large loss in 2023, returned to a modest profit of around $1.30 billion in 2024, and jumped to $9.77 billion in 2025. Thus, net income went from a negative $5.83 billion in 2023 to $0.78 billion in 2024 to $8.54 billion in 2025, with earnings per share rising from about $5.34 to $0.70 and then to $7.65.

The number of shares has increased slightly over time (around 1.11-1.12 billion diluted shares), so the EPS growth is primarily driven by a turnaround in profitability, not financial engineering. EBITDA was about $16.74 billion in 2022, dropped to about $2.21 billion in 2023, rose to about $8.94 billion in 2024, and reached about $9.77 billion in 2025. Combined with the current quarterly results, it is clear that Micron has entered a new, extremely strong phase of the cycle - but history reminds us that this phase is not permanent.

Shareholder Structure

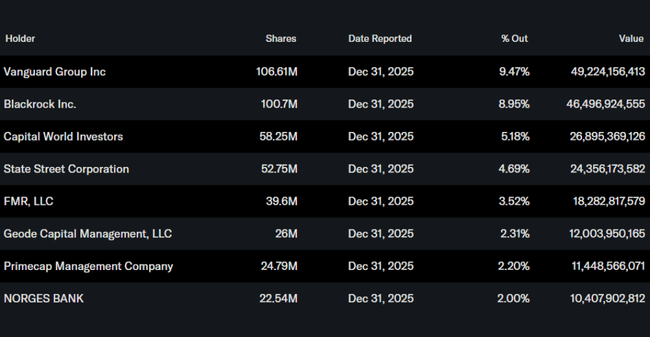

Insiders (management and directors) hold only a small proportion of shares, around 0.3 percent. The institution owns about 82-83 percent of the shares, with the rest going to retail and other investors. The largest institutional shareholders include Vanguard Group with about 9.5 percent, BlackRock with about 9 percent, Capital World Investors with about 5 percent, State Street with about 4.7 percent, and FMR (Fidelity) with more than 3.5 percent.

Such strong dominance by large funds means that Micron is a "core" holding in many index and sector funds focused on semiconductors. The stock is very liquid and its performance is sensitive to both specific memory market news and overall sentiment towards technology titles. For the retail investor, this means that it rides with the big pension and index players - but also that if sentiment towards AI and chips changes, movement can be very rapid in either direction.

News and strategic moves

Dividend increase of 30 percent - the board approved a quarterly dividend of $0.15 per share, a significant jump from the previous level and a signal that management believes in a longer duration of the current earnings cycle, not just a short-term "shock."

Massive expansion of AI manufacturing capacity - Micron confirms that it is significantly ramping up investment in its global manufacturing base (new and expanded factories in the US, Asia, and especially for HBM and advanced DRAM) to meet demand from datacenter and AI platforms; this keeps capex high in the short term, but should ensure long-term revenue from its most profitable products.

Use of government incentives - the company continues to draw significant support from the US CHIPS Act and other programs (billions for new US fabs), which lowers net investment costs and improves project returns, but also ties the company to meeting capacity and technology commitments to governments.

Strengthening its position in Asia - In addition to US projects, Micron is doubling down on its bet on Asia (especially Taiwan and Singapore) with new or expanded manufacturing plants, diversifying geographic risk and bringing production closer to key customers, but remaining exposed to geopolitical tensions in the region.