Nike’s third fiscal quarter underlined how incomplete its reset still is: revenue was roughly flat at 11.3 billion dollars, but net income fell 35% to about 0.5 billion and diluted EPS dropped to 0.35 dollars as gross margin compressed and profit came in well below last year’s level. The softness is most visible in direct to consumer, where Nike Direct declined and digital sales in key regions like EMEA and China fell double digits, while wholesale inched higher as the company leans back into retail partners.

At the same time, the “Win Now” turnaround program is deliberately putting extra pressure on near term earnings. Management is pruning lower quality product, resetting inventories and rebalancing channels away from an over concentrated DTC push, moves that create several points of revenue headwind and add severance and restructuring charges today, but are meant to leave a cleaner, more sport centric portfolio and healthier margin structure from fiscal 2027 onward.

How Q3 2026 turned out

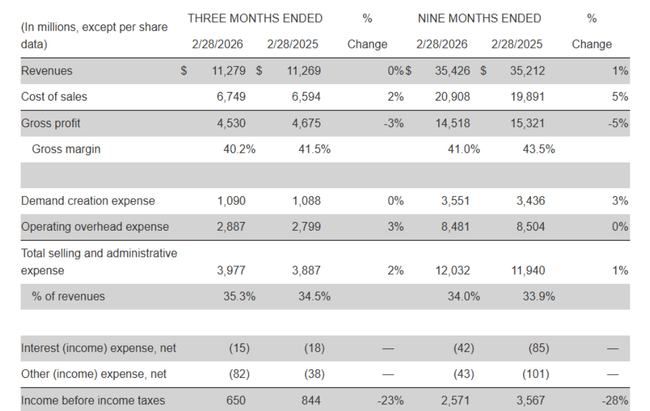

Revenue: $11.279 billion, virtually unchanged from $11.269 billion a year ago, down about 3% on a currency-adjusted basis.

Nike brand revenue: approximately $11.0 billion, roughly +1%, with growth in North America offsetting declines in Europe and China.

Wholesale: $6.5 billion, +5% (+1% on a currency-adjusted basis), the main driver of growth.

Nike Direct: $4.5 billion, -4% (currency-adjusted -7%), digital -9%, owned stores -5%.

Converse: $264 million, -35%, down in all regions.

Gross margin declined 130 basis points from 41.5% to 40.2%. The main reason for this is higher tariffs in North America, which increase unit costs of imports. Selling and administrative expenses increased 2% to $4.0 billion:

"Demand creation" (advertising + sports marketing) was around $1.1 billion, roughly in line with last year - higher sports marketing spend and currency effects offset lower brand marketing.

Operating overhead was up about 3% to $2.9 billion due to severance costs and foreign exchange effects, partially offset by lower other administrative expenses.

Operating profit fell from $844 million to $650 million (-23%). Net income fell from $794 million to $520 million (-35%), and diluted EPS fell from $0.54 to $0.35 (-35%). The effective tax rate jumped from 5.9% to 20% as last year's period included a one-time non-cash tax benefit that boosted after-tax earnings.

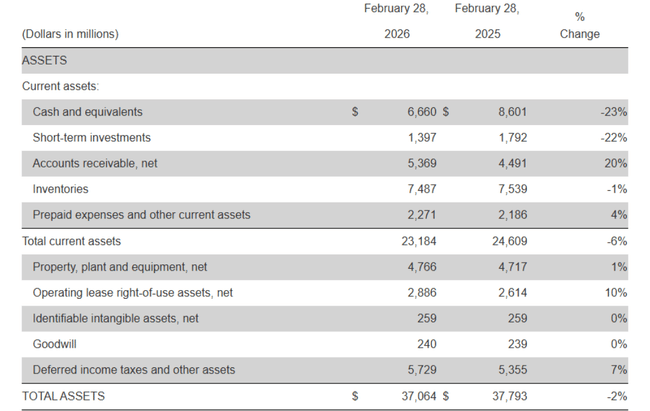

Inventories were approximately $7.5 billion, down 1% from a year ago - lower volume and a different product mix partially offset higher unit costs due to tariffs. Cash and short-term investments fell to $8.1 billion, about $2.3 billion less than a year ago, as operating cash flow was insufficient for a combination of dividends, debt repayments, capex and share repurchases.

Management Commentary

CEO Elliott Hill described the quarter as a period of "significant steps to improve the health and quality of the business". He stressed that the pace of improvement varies across the portfolio, but the areas that Nike has prioritised are already showing early signs of recovery. At the same time, he acknowledged that the work is not done, but he said the direction is clear and teams are moving forward with a focus on speed and discipline.

CFO Matthew Friend said third-quarter results were in line with internal expectations. However, he also pointed out that the "Win Now" actions will impact results for the rest of the calendar year - so the company expects the clean-up phase to be reflected in the numbers in future quarters. Still, he says the moves are intended to set Nike up for long-term profitable growth, even if they do worsen margins and earnings per share in the short term.

Why the stock fell after the results

The stock closed around $52.8 during the trading day, but fell about 9% to about $48.2 in after-hours trading after the results were released. There are several reasons:

Earnings per share of -35% - EPS of $0.35 is noticeably weaker than last year, and the market is concerned that it will take longer to return to previous levels, especially since management itself says that "Win Now" will continue to hurt the numbers in the short term.

Stagnant sales and weak Nike Direct - sales are flat and falling in real terms, with the channel that Nike has long bet on suffering the most: direct sales and digital. Investors see that growth is now being driven by wholesale, which has lower margins and less control over the brand.

Pressure on margins due to tariffs - gross margins are down 130 basis points and the company says the main cause is high tariffs in North America. This isn't a simple problem that can be solved in one action - it's a structural pressure that can drag on for longer.

Unclear turning point - management talks about discipline and long-term growth, but explicitly warns that restructuring will weigh on results for the rest of the year. The market doesn't see a specific point at which EPS and margins will start to clearly improve.

Combined with the trend of recent years (declining annual sales and earnings), this is leading investors to reassess valuations - Nike $NKE is still a strong brand, but no longer with a profile of steady earnings growth.

Long-term results

For the most recent full fiscal year (ending May 31, 2025), Nike earned $46.3 billion, down nearly 10% from $51.4 billion in the prior year. The year before, revenues were about $51.2 billion, and in 2022 they'll be about $46.7 billion, so the company is hovering around the same level rather than growing appreciably after a pandemic period.

Gross profit fell to $19.8 billion in 2025 from $22.9 billion in 2024. Meanwhile, operating expenses held high (around $16.1 billion, down only slightly from a year ago), so operating profit fell from $6.3 billion to $3.7 billion (-41%). Net income fell from $5.7 billion to $3.2 billion, and earnings per share from roughly $3.76 to $2.17.

The number of shares is down slightly due to share buybacks (about 1.61 billion diluted shares in 2022 and about 1.49 billion in 2025), but the drop in EPS is still significant. EBIT is down from about $6.3 billion to $3.9 billion, EBITDA from $7.2 billion to about $3.7 billion. So Nike has been generating solid profits over the long term, but the trend of recent years has been down, not up.

Shareholders

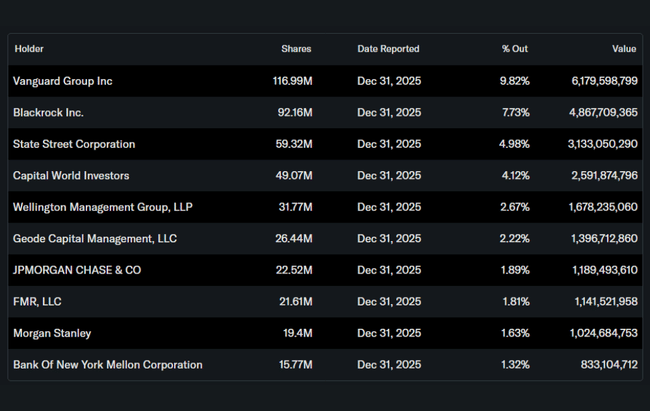

Insiders (management and directors) hold approximately 1.5% of Nike's stock. Institutional investors own around 83-85% of the stock and free float, which is typical of large US blue-chips.

The largest owners include:

Vanguard Group with a stake of approximately 9.8%.

BlackRock with approximately 7.7%.

State Street around 5%

Capital World Investors approximately 4%

This means that the share price is heavily influenced by the sentiment of the large funds. When they collectively decide that the growth profile and margins are weaker, there is a rapid repricing - just like after the current quarter.

News and action over the past quarter

"Win Now" program - Nike continues a package of measures aimed at rapidly improving efficiency: layoffs, simplification of organizational structure, greater focus on key categories and channels. In the short term, this increases costs (severance), but should reduce the fixed cost base.

Shift in sales structure - additional focus on wholesale partners in North America to clear inventory faster and strengthen share in key segments. This is a partial departure from the earlier "Direct-to-Consumer at all costs" strategy.

Inventory Control - The company continues to work on reducing inventory in problem categories and better production planning so it doesn't have to rely as much on discounts.

Marketing mix - Nike is shifting spending towards sports marketing (athletes, leagues, events) while pure brand advertising is more moderate. The goal is to strengthen the core brand in sports, not just lifestyle image.

Dividend - The company paid about $609 million in dividends to shareholders in the quarter, up about 3% from a year ago, and continues to maintain a 20+ year streak of annual dividend increases.