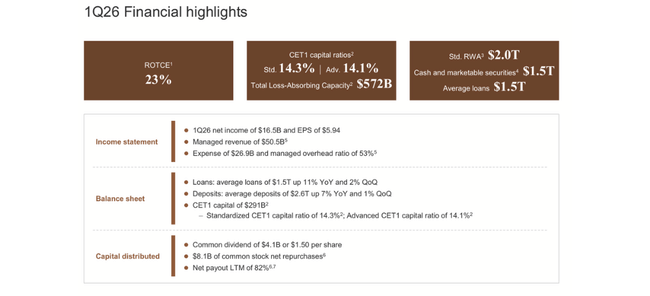

JPMorgan didn’t just beat expectations in Q1 2026, it reminded everyone why it sits at the top of the Wall Street food chain. Net income climbed to about 16.5 billion dollars for the quarter, up roughly 13% year‑on‑year, and return on equity hovered near 19%, levels that most universal banks only show in optimistic investor‑day slides.

What makes the print more than an accounting outlier is the breadth behind it: consumer and commercial banking kept growing, investment banking and markets revenues rebounded, wealth and asset management added fee income, and the balance sheet remains stuffed with capital and liquidity, giving the franchise room to keep taking share while others are still patching holes from the last rate shock.

Q1 2026 results

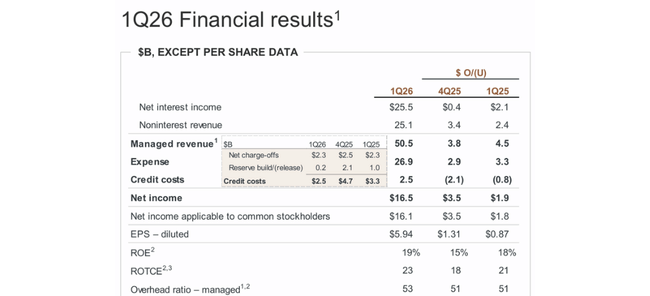

The bank reported managed revenues of around $50.5 billion for the first quarter, up about 10 percent from the same period last year. Roughly half came from interest income - net interest income was around $25.5 billion, up nine per cent on last year - and the other half from fees and trading, where non-interest income was up eleven per cent. This shows that JPMorgan $JPM is able to benefit from both the higher rate environment and the markets and fee business.

Net income came in at $16.5 billion, up from about $14.6 billion in the same period last year. Earnings per share were $5.94, well above last year's $5.07 and also above what the market was expecting. Return on equity comes out to nineteen percent and return on tangible equity to twenty-three percent, which is elite levels in the banking world. Even net of the cyclical favorable environment, that's just a very high profitability.

On the expense side, the bank spent about $26.9 billion, up about fourteen percent from a year ago. So it's true that costs are growing fast, but revenues are growing even faster, so profitability has improved despite higher payroll, marketing and other items. Loan loss provisions were $2.5 billion, with net charge-offs of $2.3 billion - almost the same as last year - and the net addition to reserves was only slightly positive, indicating that the bank sees no deterioration in credit quality.

The balance sheet and capital position show why Dimon keeps talking about a "fortress balance sheet." CET1's core capital is about $291 billion, CET1's capital ratio is about 14.3 percent (standardized methodology), total loss absorbing capacity (TLAC) is about $572 billion, and cash with liquid securities is about $1.5 trillion. Average loans are up eleven percent year-over-year to about 1.5 trillion and average deposits are up seven percent. So the bank is both growing and sitting on a very strong capital cushion.

Shareholders have not been left out - in this quarter alone they received roughly $4.1 billion in dividends ($1.50 per share) and have received another $8.1 billion back through buybacks. So over the past twelve months, the total "payout" - the combination of dividends and buybacks - is about 82% of earnings.

Retail & Consumer (Consumer & Community Banking)

The Consumer & Community segment delivered a net profit of around five billion dollars, up around twelve percent from a year ago. Revenues were approximately $19.6 billion, up seven percent year-over-year.

Retail Banking & Wealth Management grew primarily due to higher fees and investment management revenues. The mortgage business benefited from higher production, although net interest income in this segment declined slightly. Cards and auto financing were clearly a strong driver, with higher revolving credit card balances and higher auto leasing revenues pulling this subsegment's revenues up more than ten percent.

Retail costs grew rapidly, up about eleven percent. They were pulled up by investments in marketing, higher depreciation in leasing, and higher fees for bankers and consultants. Provisions remain within reasonable limits - net charge-offs rose slightly, but some provisions are dissolving thanks to better real estate prices. The segment's overall return on capital of around thirty-two percent shows that JPM's consumer business is very profitable, albeit cyclical.

Commercial and Investment Bank (CIB)

The Commercial and Investment Bank is the main "driver" of results. Net income was about nine billion dollars, up thirty percent from a year ago, and revenues rose to about 23.4 billion dollars, up nineteen percent.

In investment banking, revenues were up nearly forty percent, and advisory and equity fees were up about 28 percent. This meant that M&A and equity issuance picked up again after a weaker period, and JPM was able to carve out the biggest slice of that - over nine per cent of the global IB fee market in the first quarter. Payments added double-digit growth thanks to higher deposits and fees, while the credit side benefited from higher balances and gains from portfolio hedging.

Trading and securities services were also very strong. Trading revenues were around $11.6 billion, up twenty percent from a year ago, with fixed income trading growing by more than twenty percent and equity trading by around seventeen percent. Securities services benefited from higher market valuations and greater client activity. Costs in CIB rose by around thirteen per cent - mainly due to higher fees and commissions - but the segment's profitability still improved, with return on capital around twenty-one per cent.

Asset & Wealth Management

The wealth management segment generated a net profit of around $1.8 billion, about twelve percent higher than last year. Revenues moved to $6.4 billion, representing about eleven percent growth. The main drivers are higher management fees due to rising market valuations and net capital inflows, as well as higher client trading activity.

Assets under management climbed to about $4.8 trillion, client assets to $7.1 trillion, and long-term net inflows into funds and other products were about $54 billion in the quarter alone. This is important for stability - the larger this cushion, the less reliance on one-off transactions in investment banking.

What Dimon had to say about this and how to think about it

Jamie Dimon's commentary on the results is that performance is strong across the business - retail, investment bank and wealth management are all growing at the same time, in an environment that is supportive but also fraught with risk. He notes that the bank has "plenty of capital and liquidity" and that while changes to the proposed capital rules have removed the biggest extremes, there is still room for improvement.

On the macro front, he says the US economy has been resilient so far: people have jobs, people are spending, companies are in good shape, plus fiscal policy, some deregulation, investment in AI and previous Fed actions are helping. But on the other hand, he warns of a mix of geopolitical risks, tensions in energy markets, trade disputes, high deficits and inflated asset prices. In other words - the numbers look great, but there's no reason to think the risks have gone away.

Long-term results: strong trend, but 2025 was not a new record

JPMorgan had about $153.8 billion in revenue in 2022, about $236.3 billion in 2023 and about $270.8 billion in 2024 - very strong growth, driven mainly by higher rates and activity in the markets. 2025 brought in around 256.5 billion in revenues, a slight decline from 2024 but still well above 2022-2023 levels.

Gross profit rose to about $168.2 billion in 2025, up from $158.8 billion in 2024 and $145.7 billion in 2023. Operating expenses rose to about $95.6 billion, up slightly from $83.7 billion in 2024, so operating profit fell slightly from $75.1 billion to $72.6 billion. Still, that's significantly higher than 2022, when operating profit was around 46 billion.

Net income reached about $57.0 billion in 2025, just a bit less than the $58.5 billion in 2024 but noticeably more than the $49.6 billion in 2023 and $37.7 billion in 2022. Meanwhile, earnings per share moved from about $12.1 in 2022 to $16.3 in 2023, $19.8 in 2024 and $20.1 in 2025, thanks to buybacks and profitability growth.

This implies several things:

2024 was the "peak" of the cycle so far in terms of revenue and profit, and 2025 was slightly behind, but it was still a very strong year.

The trend over the last four years is clearly up - higher earnings, higher EPS, higher gross profit.

Q1 2026 builds on this trend and shows that the bank has not fallen off the top of the cycle yet, rather it is near the top.

Shareholders

JPMorgan is a classic institutional large bank. Insider holdings are small, around half a percent of the stock, with the majority in the hands of funds.

According to the latest data, they are holding:

Vanguard roughly 265.8 million shares (about 9.9%)

BlackRock about 211.6 million (about 7.9%)

State Street about 125.3 million (about 4.7%)

Morgan Stanley about 66.4 million (about 2.5%)

The institutions as a whole control over three-quarters of the free float. That said, the evolution of the share price is very much about how the consensus of the big funds evolves. If they recalculate the models and conclude that a 19% ROE and sixteen and a half billion in quarterly earnings is sustainable, they can send the stock significantly higher. If, on the other hand, they see this as the top of the cycle and start counting on a normalization of profitability, they can put the brakes on the upside even after a great quarter.

News and strategic moves over the past period

The bank continues to clean up and fine-tune retail - building credit cards and consumer finance, but keeping discipline on risk, as seen in stable charge-offs and only modest reserve changes.

In investment banking, it confirms its number one position globally - a nearly 10 percent share of fees in the first quarter and double-digit fee growth show JPM is taking full advantage of the resurgent M&A and capital markets.

Wealth management is building on massive growth in assets under management and net inflows, which is key to a stable fee business over the long term.

The firm communicated a 2026 net interest income outlook of around $103 billion, although it expects rates to fall further - relying on loan growth, particularly in cards and other credit segments, and a better deposit mix.

At the regulatory level, JPMorgan is actively involved in the debate over the final form of Basel III rules in the US - the aim is that capital rules should not restrict banks' ability to fund the economy while leaving room for a reasonable payout of capital to shareholders.