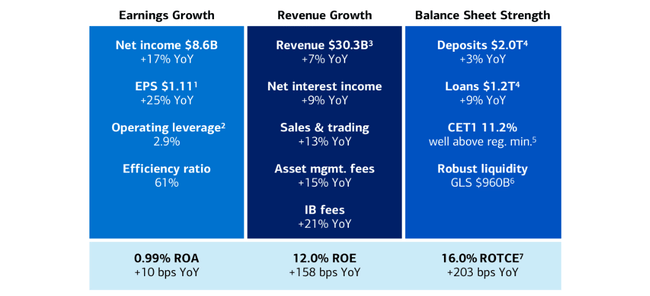

Bank of America kicked off 2026 with the kind of broad‑based beat that reassures investors the franchise is using the higher‑for‑longer rate backdrop to full effect. Net income rose 17% year‑on‑year to 8.6 billion dollars, diluted EPS jumped 25% to 1.11 dollars - the highest quarterly reading in almost two decades - and revenue climbed 7% to about 30.3 billion, outpacing expectations on the back of higher net interest income, robust trading, a rebound in investment banking fees and steady growth in wealth management.

Management reinforced the message with commentary about “healthy” U.S. consumers and stable asset quality, arguing that strong card spending and benign credit metrics show the bank is not buying its earnings growth by taking more risk on the loan book.

How Q1 2026 turned out

For the first quarter of 2026, Bank of America $BAC generated approximately $30.3 billion in earnings after interest, versus about $28.2 billion in the same period last year. This equates to seven percent growth. Net interest income was $15.7 billion, up nine percent from a year ago, primarily due to higher interest rates in prior years, growth in loan balances and asset re-pricing. Noninterest income rose to about $14.5 billion from $13.8 billion, reflecting stronger trading, also higher investment banking and asset management fees.

Net income came in at $8.6 billion in Q1, up from $7.3-7.4 billion a year ago, up around 17%. Earnings per share (diluted EPS) was $1.11, up from around $0.89-0.90 last year. Thus, EPS was up about 25% year-over-year, partly due to earnings growth and partly due to fewer shares outstanding after buybacks. Meanwhile, market expectations were around $1.00-1.01 per share, so the bank's EPS and earnings clearly beat.

Costs grew more slowly than revenues. Non-interest expenses increased by about four percent, while revenues grew by seven percent, giving room for an improvement in operating leverage of about 2.9 percentage points. This is exactly what analysts and investors wanted to see after years in which costs often "ate" revenue growth.

Credit quality remained stable. Net charge-offs held at relatively low levels, and the overall picture suggests no dramatic problems for either consumers or corporate clients. Management's comments on the results highlight that consumers are still spending, employed and repaying, while businesses are in good financial health in most cases.

The bank's capitalisation remains robust: the CET1 ratio is around 11.2% and the leverage ratio (SLR) is in a safe band above regulators' requirements. This allows for a combination of dividend and share buybacks without bringing the bank close to regulatory limits, although the exact Q1 capital payout numbers are not dissected in detail in the available reports.

Segments

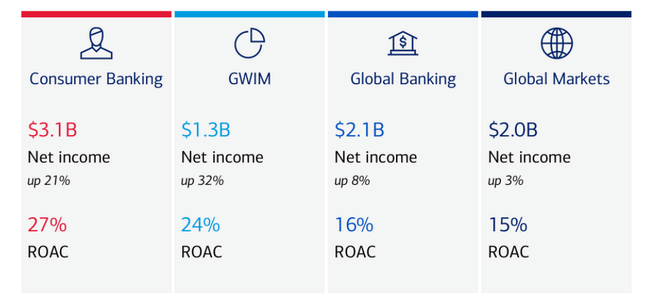

Consumer Banking - generated net income of around $3.1 billion on revenue of $11.0 billion, implying roughly five percent revenue growth. Growth was mainly driven by higher interest income, with average deposits of around $951 billion and average loans of around $322 billion. Card transactions (debit and credit combined) reached about $245 billion, a seven percent growth, and return on equity ratios (ROAAC) in this segment held around 27 percent.

Global Wealth & Investment Management (GWIM) - delivered about $1.3 billion in net income and $6.7 billion in revenue, or about 12 percent growth. Wealth management fees rose 15% to about $4.2 billion, client assets reached $4.6 trillion (growth of about 10%), and about $20 billion of new capital flowed into managed portfolios. Average loans in the GWIM grew 13% to 262 billion.

Global Banking - reported net income of around $2.1 billion and revenue of $6.3 billion, about 5% growth. Drivers were higher investment banking fees, leasing income and net interest income; average deposits rose 13% to $648 billion and average loans rose 5% to $397 billion.

Global Markets - generated approximately $2.0 billion in net income; sales and trading revenue was approximately $6.4 billion, up 13% from last year, including a small positive impact from the revaluation of the proprietary credit position (DVA).

So overall, the result holds together: retail banking, investment banking, trading and wealth management all contributed to growth in revenue, earnings and return on capital.

As management commented on the results

CEO Brian Moynihan reported two main messages in his commentary.

First, that this was strong, across-the-board growth. He highlighted that the bank had achieved a "strong start to the year", with revenue up seven per cent, net profit up 17 per cent and EPS up 25 per cent. He cited growth in net interest income, good trading performance, higher fees from investment banking and asset management as key drivers.

Second, that consumer and credit quality remain healthy. Moynihan says bluntly that customers continue to spend, have stable incomes and the bank sees no widespread problems in the portfolio. This is important in an environment where rates are not as high as they were in 2023-2024, but they are still relatively restrictive and some investors were concerned that this would translate into a significant increase in non-performing loans.

Moynihan and other members of management have reiterated that Bank of America will continue to seek positive operating leverage - i.e., keeping cost growth below revenue growth - and leverage investments in digitization and AI (such as "Erica 2.0" in retail) to increase efficiency without sacrificing the customer experience.

Long-term results

In 2022, Bank of America will generate roughly $115.1 billion in revenue. Revenue moved to $171.9 billion in 2023 (up roughly 49%; part of this is due to the methodology and the high rate environment), to $192.4 billion in 2024 (+11.9%), and fell slightly to $188.8 billion in 2025 (-1.9%). Thus, 2025 was more of a "stabilization" year after very strong growth in previous years.

However, gross profit rose to $104.6 billion in 2025 from $96.1 billion in 2024. Operating expenses rose only slightly to $69.7 billion (from $66.8 billion), so operating profit jumped to $34.9 billion, up 19% from $29.3 billion in 2024. This means that despite slightly lower sales, the bank was able to improve profitability and margins.

Net income for 2025 reached $30.6 billion, up from $27.1 billion in 2024 and $26.5 billion in 2023. Diluted EPS rose from roughly $3.19 in 2022 to $3.08 in 2023 and $3.22 in 2024 to $3.82 in 2025. EPS growth is supported by both higher earnings and a decline in the number of shares, with the average number of diluted shares declining from about 8.17 billion in 2022 to about 7.85 billion in 2024 and about 7.55 billion in 2025.

Shareholders

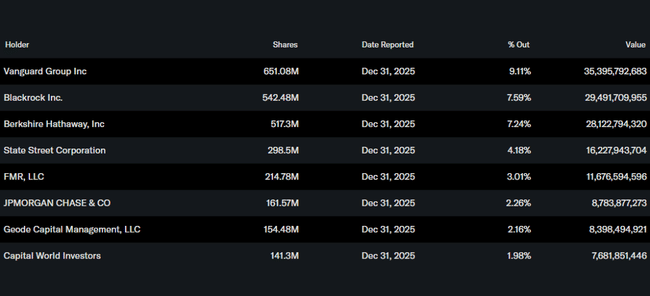

Insiders (management and board) account for about 7.4% of shares, which is quite a lot for a large US bank. The institution as a whole holds about 71.6% of the shares and about 77% of the free float.

The largest shareholders include:

Vanguard with a stake of about 9.1% (about 651 million shares)

BlackRock with about 7.6% (about 542 million shares)

Berkshire Hathaway with about 7.2% (about 517 million shares)

State Street with about 4.2% (about 298 million shares)

The presence of Berkshire Hathaway (Warren Buffett) in particular is a signal to many investors that it is a "favored" bank in his portfolio, which may play a role in sentiment and how readily retail investors hold the stock. At the same time, however, the share price is strongly tied to how large fund houses view Bank of America as a sector title - their collective change of heart can move the price significantly.

News and strategic moves

Normalization after an era of extremely high rates: after three rate cuts in late 2025, the Fed is keeping rates around 3.5%-3.75% for now. Bank of America is no longer just a "pure bet on higher rates" - it needs to show growth in fee and trading businesses as well, as Q1 2026 confirms.

Emphasis on net interest income and wealth management: management has repeatedly said that NII remains a key driver, but that the main growth legs are Merrill Lynch and Private Bank, where the bank is building new relationships and growing assets under management.

Digitisation and AI ("Erica 2.0"): The bank is expanding its use of AI in retail banking, particularly through its virtual assistant Erica. The aim is to reduce servicing costs, improve the customer experience and thereby promote positive operating leverage.

Capital policy: Bank of America is combining dividend and buybacks, and after 2025, with EPS of $3.82 and growing net income, it has room to further increase payouts - always, of course, taking into account capital requirements and stress test results.

Competitive position: within the large US banks, Bank of America remains the "second pillar" next to JPMorgan - smaller in terms of revenue but with a very strong retail and wealth footprint. Q1 2026 shows that the bank can deliver revenue and earnings growth even in a normalized rate environment, which is a good sign for investors.