TSMC’s latest quarter reads like a blueprint for what an AI super‑cycle does to a best‑in‑class foundry. Revenue for Q1 2026 reached about 1.134 trillion Taiwan dollars, roughly 35.7 billion dollars, up 35% year‑on‑year and at the very top end of the guidance range management gave back in January, as demand for advanced AI and high‑performance computing processors drove record March sales and kept leading‑edge nodes running hot. Net income jumped by roughly 58% compared with a year ago, pushing earnings per share to 22.08 Taiwan dollars – about 0.70 dollars per common share, or 3.49 dollars per New York‑listed ADR – while gross margin expanded to around 55–66% depending on mix and currency and operating margin sat close to the high‑40s, levels that most chip designers, let alone manufacturers, can only dream of.

Management is signalling that this is not a one‑off spike. For the second quarter, TSMC expects dollar revenue to climb again toward roughly 39–40.2 billion, with gross margin in the low‑to‑mid‑60s and operating margin in the mid‑50s, supported by orders from customers like Nvidia and Apple and by a product mix where advanced technologies account for well over 70% of wafer sales. To keep up, the company plans to lean toward the high end of an enormous 52–56 billion dollar capital‑expenditure budget in 2026, ploughing cash into N2 capacity and advanced packaging such as CoWoS – a reminder that even for the clear winner of the AI chip boom, sustaining those extraordinary margins requires writing some of the biggest capex cheques in the entire tech industry.

How Q1 2026 turned out

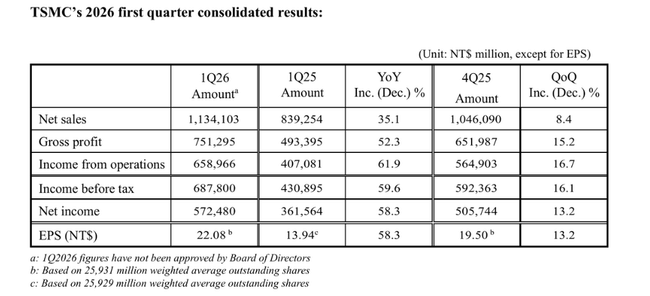

For Q1 2026, TSMC earned $TSM TWD1.13 billion, or roughly $35.9 billion. Year-over-year, revenue growth was 35.1% in TWD and 40.6% in USD, with quarter-over-quarter revenue growth of 8.4% in TWD and 6.4% in USD. Net income came in at TWD 572.5 billion, or about USD 18 billion, up 58.3% from a year ago and up 13.2% from Q4 2025.

Margins are also top-notch for the semiconductor sector. Q1 gross margin was 66.2%, operating margin was 58.1% and net margin was 50.5%. This means that for every dollar of sales, the company is left with roughly half a dollar of net profit after all costs. From a global foundry perspective, this is an almost unmatched level and confirmation that TSMC has tremendous pricing power in its most advanced processes.

The sales structure shows where the growth is coming from. 3nm processes accounted for 25% of sales, five nanometers 36% and seven nanometers 13%. Together, advanced technologies (7nm and better) accounted for 74% of wafer sales. This means that TSMC is now largely a "leading-edge" fab - and it is these nodes that are key to AI, datacenters, high-end smartphones and high-end GPU/CPUs.

Quarter-on-quarter sales grew despite a seasonally weaker period - Q1 is often quieter for semiconductors, but this time demand for 3nm and 5nm processes outweighed seasonality. This can be seen in the CFO's comments, who says Q1 growth was driven by "strong demand for our most advanced process technologies".

What management has to say

Commenting on the numbers, CFO Wendell Huang stressed that the business was driven by strong demand for its most advanced processes in Q1 and that the same engine would drive Q2. The company expects Q2 2026 revenue in the range of $39-40.2 billion, another quarter-on-quarter growth.

For Q2, TSMC also gives a gross margin outlook in the range of 65.5-67.5% and an operating margin between 56.5% and 58.5%. This means that even with high investments and capacity expansion, it does not expect any significant profitability loosening. Management is essentially saying "we will continue to invest massively, but you won't see it on margins".

In the broader TSMC commentary, they talk about:

demand is driven primarily by AI and datacenter chips

demand for chips in general is starting to outstrip supply

customers are accelerating their capacity expansion plans for 2026 and beyond

and TSMC has full order books at the 3nm and 5nm nodes while preparing for the next generation (2nm)

Long-term results

Revenues in 2022 were roughly TWD2.26 trillion, falling slightly to TWD2.16 trillion a year later (the company was then absorbing a drop in PC and smartphone demand after the covid boom). That was a "breather" year, when the market was wondering if TSMC was in for a prolonged downturn after extremely strong years. The answer came quickly: sales jumped to TWD 2.89 trillion (+34%) in 2024 and TWD 3.85 trillion (+33%) in 2025, driven mainly by the emergence of AI and datacenter chips.

The improvement in margins is even more pronounced. Gross margins in 2022 of around TWD 1.35 trillion shrink to TWD 1.18 trillion in 2023 due to weaker demand, but jump to TWD 1.62 trillion in 2024 and TWD 2.30 trillion in 2025 - up nearly 42% in a single year. Operating profit has followed a similar path: from TWD 1.12 trillion (2022) to TWD 0.92 trillion (2023) to TWD 1.32 trillion (2024) and TWD 1.96 trillion (2025). This shows two things at the same time - TSMC can cut back quickly in a bad year and, conversely, make the most of high margins in a better year.

Net profit dropped from roughly TWD 993 billion to TWD 852 billion in 2023 (-14%), but rose to TWD1.16 trillion in 2024 and TWD1.74 trillion in 2025, a further increase of almost 50%. Earnings per share tell the same story: 191 TWD in 2022, 164 TWD in 2023, 223 TWD in 2024 and 335 TWD in 2025, with the number of shares virtually unchanged. That said, EPS growth is purely about business, not financial gimmicks.

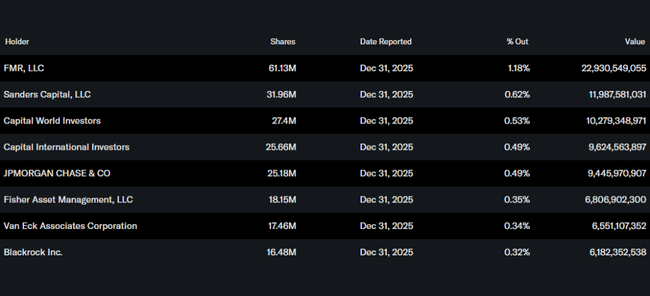

Shareholders

Insiders hold about 0.05% of the stock, institutions about 15.7% of the total number of shares and free float. This is significantly less than the typical US blue chip, where institutions often own over 70%. The rest is spread among the public sector, domestic investors and retail shareholders.

The largest institutional foreign shareholders include FMR (Fidelity) with about 1.2%, Sanders Capital with about 0.6%, Capital World Investors and Capital International Investors, each with a stake of under one percent. None of these players has a position comparable to, say, Vanguard or Berkshire at US banks - TSMC is a more "spread out" title from a global perspective.

News and strategic moves

AI as the main driver: the company is clear that demand for 3nm and 5nm processes is mainly driven by AI and datacenter chips - GPUs, accelerators and advanced CPUs. Customers (large cloud players, design firms and traditional chipmakers) are pushing their orders forward to secure capacity.

Upcoming 2nm generation ramp: TSMC is investing heavily in the 2nm node, which is expected to go into mass production in the second half of this decade. Q1 2026 shows that the company has the financial strength and margins to fund this ramp from its own cash flow.

Geography and geopolitics: TSMC continues to build capacity outside Taiwan - factories in the US (Arizona), Europe (Germany) and Japan. These projects are expensive and margins on them will initially be lower, but the company sees them as a strategic necessity given the US and EU pressure to "onshoring" critical manufacturing.

Export and security restrictions: like ASML, TSMC operates in an environment of increasing export and security restrictions against China. So far, it has been able to compensate for the shortfall in Chinese demand with Western customers, but the company has to take this into account in its production and investment planning.

Strong position in the ecosystem: TSMC produced over 12,600 different products for more than 500 customers on 305 process technologies in 2025. This implies tremendous technological depth and customer stickiness to its ecosystem - switching to another foundry would be extremely costly for most.