Intuitive Surgical’s first quarter of 2026 checks almost every box you’d want from a high‑quality med‑tech name. Revenue climbed 23% year‑on‑year to about 2.77 billion dollars, driven by a 17% increase in total procedures (around 16% growth on da Vinci and 39% on Ion) and a steadily expanding installed base of both systems. Non‑GAAP EPS jumped to roughly 2.50 dollars, up about 38% versus last year and well ahead of expectations, while recurring revenue from instruments, accessories and services grew in line with the top line and now accounts for roughly 86% of total sales.

The mild pullback in the share price says more about expectations than about the quarter itself. After several years of high‑teens to nearly 20% procedure growth, management is guiding 2026 da Vinci volumes up by about 13–15%, and investors are highly sensitive to any hint that growth is normalizing and that margin headwinds from tariffs and operating‑expense growth in the low‑to‑mid teens could cap upside over the next few years. In that sense, Q1 looks less like a warning sign about the business and more like a reminder about the stock: Intuitive is moving into a more mature phase where it still delivers robust double‑digit growth and expands its robotic footprint, but the valuation is rich enough that even small changes in growth and margin trajectories show up immediately in the price.

Q1 2026 results

Revenues, performance and systems

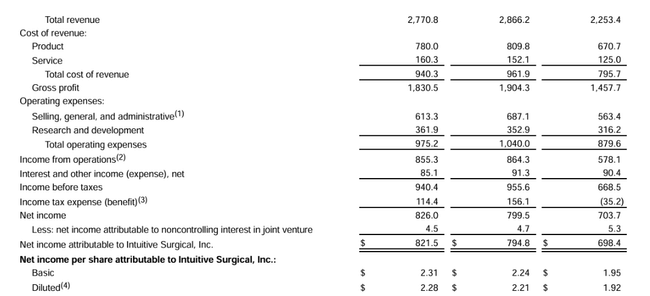

In the first quarter of 2026, Intuitive $ISRG achieved revenues of $2.77 billion, up 23 percent from $2.25 billion in the same period of 2025. Growth in excess of twenty percent rests on three pillars. The first is a higher number of procedures on the da Vinci and Ion systems, the second is a higher number of new systems installed, and the third is a growing installed base that generates recurring revenue from instruments, accessories and services.

The number of interventions on Intuitive systems increased globally by approximately seventeen percent. Procedures on da Vinci alone grew around sixteen percent, while Ion is going through an even faster phase, with procedures on that system up around 39 percent. The company placed 431 da Vinci systems in the quarter, compared to 367 a year ago, with the number of new da Vinci 5 systems rising from 147 to 232. The da Vinci installed base increased to 11,395 systems, up 12% from a year ago, and Ion to 1,041 systems, up 22% year-over-year.

Revenue structure and profitability

Tooling and accessories revenue was $1.69 billion in the first quarter, up 23% from $1.37 billion a year ago. The main drivers were growth in da Vinci procedures, changes in customer purchasing behavior and rapidly increasing use of the Ion system. Systems revenue increased to $651 million compared to $523 million a year ago, reflecting a higher number of new systems placed, a higher proportion of rentals and higher average selling prices. Of the 431 da Vinci systems, 243 were placed under operating leases and 118 were placed on a usage-dependent basis, compared to 198 leased and 107 placed on a usage-dependent basis a year ago.

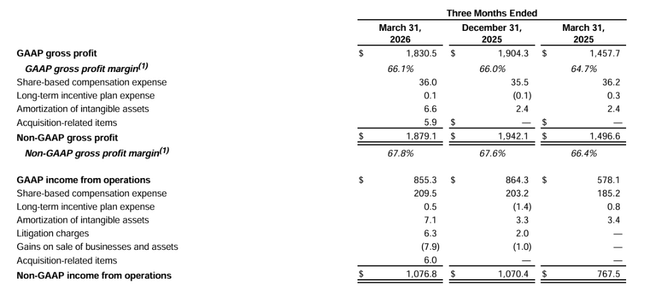

Profitability has improved significantly. Accounting-standard operating profit rose to $855 million versus $578 million in the first quarter of 2025, and adjusted operating profit rose to $1.08 billion versus $770 million. Net income by accounting standards was $822 million, which translates to earnings of $2.28 per share versus $1.92 a year ago. Adjusted net income rose to $901 million and adjusted earnings per share to $2.50, compared with $662 million and $1.81 per share in the first quarter of 2025.

Those numbers mean that adjusted earnings per share are growing at about 38% on 23% revenue growth, and the company has significantly beaten analysts' expectations, who were expecting sales of about $2.62 billion and earnings of about $2.12 per share. Still, the stock is down after the results, as the market is looking not just at the last quarter, but at the outlook for growth rates going forward.

Outlook for 2026

For the full year 2026, Intuitive expects the number of procedures on da Vinci systems to grow by approximately 13.5% to 15.5%. This is still a very respectable pace, but it also marks a slowdown from previous years, when growth was higher and was one of the reasons for the stock's very strong performance. The company also expects adjusted gross margin to be in the range of 67.5% to 68.5% of sales and growth in adjusted operating expenses to be roughly between eleven and fourteen percent.

The impact of customs measures is built into the outlook. The company says directly that it expects the current tariffs to reduce gross margin by about one percentage point. Should tariffs be further extended or tightened, the impact on margins and overall results for the year could be more significant. This is a factor that the market is watching because the company has a global supply chain and most of its manufacturing and components happen outside the United States.

It is the combination of a gradual slowdown in the growth of interventions and the sensitivity of margins to external influences that is one of the reasons why the stock fell in regular trading after an otherwise very good quarter.

The evolution of the business in recent years

Looking at the numbers over the last four years, there is a very clear upward trend. Revenues in 2021 were approximately $5.71 billion. In 2022 they rise to around $6.22 billion, in 2023 to $7.12 billion and in 2024 to $8.35 billion. The growth rate has been between about nine and seventeen percent per year, with growth accelerating in the last two years.

Net income shows a similar pattern. After reaching about $1.70 billion in 2021, it dropped to about $1.32 billion in 2022, only to return to growth in subsequent years. In 2023 it was around 1.80 billion and in 2024 it was around 2.32 billion. Earnings per share, due to a slight decline in the number of shares and growth in net income, rose from about $4.66 to $4.79 in 2021 to about $3.65 to $3.72 in 2022, then to about five dollars in 2023 and to more than six dollars in 2024.

Overall, this means that Intuitive is a long-term growth company with high margins and the ability to grow earnings per share at a higher rate than sales. The brief blip in 2022 was more of an episode than a trend change. The subsequent return to double-digit sales growth and even faster earnings growth shows that the company has been able to switch back into growth mode, and the first quarter of 2026 fits into that picture.

Shareholders and capital structure

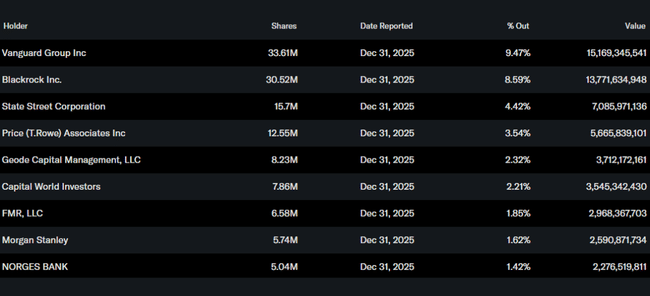

Intuitive Surgical's shareholder structure is very similar to other large healthcare titles. According to data from Yahoo Finance, insiders hold roughly one-half of one percent of the stock, while the institution owns approximately eighty-nine percent of all shares and nearly ninety percent of the free float. More than 3,200 institutions hold shares in their portfolios.

Among the largest investors are asset managers, who tend to be the mainstays of large index and actively managed funds. Vanguard holds about 33.6 million shares, about nine and a half percent of the company. Blackrock owns about 30.5 million shares, or roughly eight and a half percent. Other significant positions are held by State Street, T Rowe Price and Geode Capital, which together add another unit of percent. For the investor, this means that the title is heavily in the hands of long-term institutional capital, and short-term price swings are often associated with over-hyped expectations rather than panicked retail moves.

Why the stock is down after earnings despite a strong quarter

At first glance, it would seem that after 23% revenue growth and nearly 40% earnings per share growth, the stock must be rising. Moreover, Intuitive beat estimates on both revenue and earnings and showed another shift in both the number of performers and the size of its installed base. Still, the title lost around three per cent in the regular session and only pulled back some of the decline in post-trade trading.

The reason for this is that the market is looking primarily at the future growth rate for Intuitive. The company itself says it expects growth in da Vinci surgeries in 2026 to be in the range of about thirteen and a half to fifteen and a half percent, down from last year. It also notes that tariffs will continue to put pressure on gross margins and that it must invest in operating costs to maintain its technological edge and relationships with hospitals.

Inversely, Intuitive has had a period of extremely strong growth and some very strong quarters, so some of the positive news has already been priced in. The current quarter confirms that the business is in great shape, but also shows that the growth rate will gradually normalize from very high levels to still decent, but lower levels.