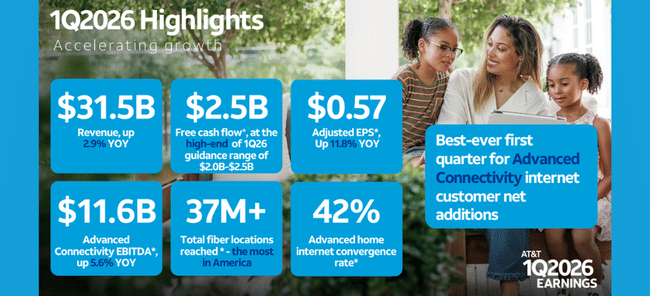

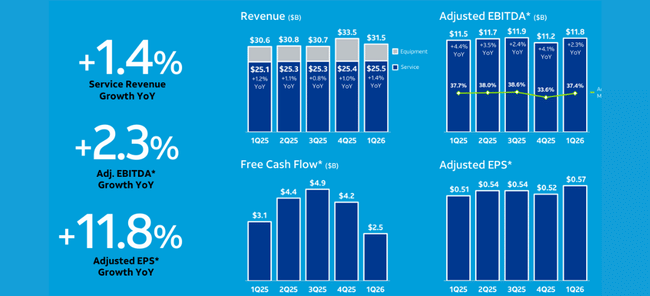

AT&T’s first quarter of 2026 delivered the kind of steady, no‑drama numbers you’d hope to see from a telecom that has spent the past few years simplifying its structure and refocusing on connectivity. Total revenue grew 2.9% year‑on‑year to 31.5 billion dollars, slightly ahead of expectations, driven by a 3.6–4.7% increase in Advanced Connectivity service revenue as wireless and fiber bundles continued to scale. Adjusted EPS came in at 0.57 dollars, up 11.8% from a year ago and modestly above the roughly 0.55‑dollar consensus, helped by 15–16% growth in operating income as the mix shifts away from legacy copper services toward higher‑margin 5G and home internet.

Management reaffirmed its full‑year 2026 guidance: adjusted EPS of 2.25–2.35 dollars, free cash flow of at least 18 billion dollars and a capital‑return plan that calls for more than 45 billion dollars to be returned to shareholders via dividends and buybacks between 2026 and 2028, while gradually bringing net‑debt‑to‑EBITDA down from just over 3x toward a 2.5x target in the following three years. Q1 free cash flow of 2.5 billion dollars was seasonally soft and below last year, but still in the guided 2.0–2.5‑billion range, and the company added 584,000 internet customers (split evenly between fiber and fixed wireless), with nearly 45% of advanced home‑internet users also taking AT&T wireless - a sign that the “advanced connectivity” strategy is doing exactly what it’s supposed to do: grow a sticky, bundled base that can support debt reduction and a high dividend without needing eye‑catching top‑line acceleration

Q1 2026 results

AT&T's consolidated revenue $T reached $31.5 billion in the first quarter, up roughly 2.9 percent from last year's $30.6 billion. The main reason for this is growth in the advanced connectivity and fiber optics segment, fueled in part by newly acquired customers from the Lumen fiber optics acquisition.

Operating profit rose to $6.7 billion from $5.8 billion a year ago and adjusted operating profit to $6.9 billion from $6.4 billion. Net income from continuing operations was $4.2 billion, while diluted earnings per share from continuing operations were $0.54, down from $0.61 last year because last year's figure still included the contribution from the stake in DirecTV. On an adjusted basis, however, earnings per share rose from $0.51 to $0.57, or about twelve percent, easily beating analysts' estimates.

Operating cash flow was $7.6 billion compared to $9 billion last year, with last year's number including about $1.4 billion from DirecTV. Capital expenditures were $4.9 billion, total capital investment including vendor financing repayments was $5.1 billion and free cash flow after those expenditures was $2.5 billion. Total debt at the end of the quarter is $138.4 billion, net debt is $126.4 billion.

Advanced connectivity: a key growth driver

The advanced connectivity segment, which brings together mobile services, fiber optics and fixed wireless, is now the core of AT&T's investment story. In the first quarter, it generated $28.5 billion in revenue, up 4.7 percent year-over-year, while service revenue in this segment grew 3.6 percent to $22.9 billion.

In mobile services, the company added 294,000 new postpaid phone customers and maintained a very low churn rate of 0.89 percent. Mobile service revenues grew around two percent, reflecting a combination of higher client numbers, more expensive tariffs and the unwinding of some promotions.

An even more pronounced shift is seen in fixed internet. Advanced residential and business internet services added a total of 584,000 new connections, with 292,000 on fibre and 292,000 on fixed wireless. The pure residential segment added 512 thousand connections, of which 273 thousand were on fibre and 239 thousand on fixed wireless. Revenues in this segment grew by more than twenty-seven percent, making it the fastest growing part of AT&T $T's business today.

As a result, profitability is picking up. Advanced Connectivity segment operating profit jumped to $6.9 billion, about fourteen and eight-tenths percent growth, and segment operating margin rose to 24.1 percent from 22 percent last year. Adjusted segment EBITDA was $11.6 billion, plus 5.6 percent year-over-year, and EBITDA margin is around 40.6 percent.

The convergence ratio is also an important indicator. Approximately 42 percent of households with advanced Internet from AT&T also have mobile service, and if the new optical customers acquired through the Lumen acquisition are excluded, it's nearly 45 percent. The company says this is the fastest organic convergence growth in history, supporting the thesis that service interconnection increases customer value and profitability.

Legacy business, Latin America and network

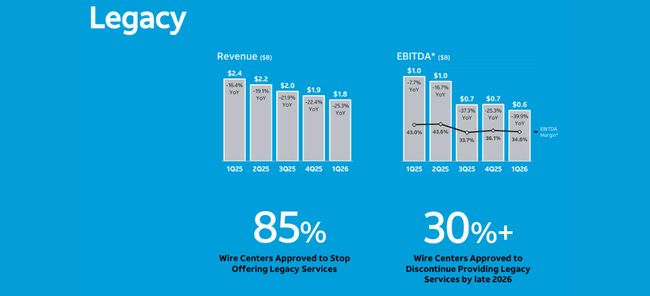

On the flip side stands the legacy business, i.e. legacy voice and data services over copper. Here, first-quarter revenues fell to $1.77 billion, a decline of over 25 percent. The segment's operating profit fell to $612 million and margins slid from roughly 43 to 34.6 percent. But AT&T sees that as part of the plan. The goal is to phase out this business and migrate customers to fiber and wireless.

The Mexico segment posted sales of about $1.17 billion, up about twenty-one percent, primarily due to exchange rates and higher customer numbers and equipment sales. However, operating profit fell to $20 million as costs grew even faster.

In terms of infrastructure, AT&T continues to invest massively in fiber optics. The total reach of the optical network exceeds 37 million addresses, including more than four million added by the acquisition of part of the Lumen optical business. The company confirms that it is targeting over forty million optical addresses by the end of 2026 and over sixty million by 2030, in part by structuring optical assets into subsidiaries with outside capital.

Outlook to 2026 and long-term plan

After the first quarter results, AT&T's outlook for 2026 is only confirmed. It expects total service revenues to grow in the low single digits of percent, advanced connectivity service revenues to grow by more than five percent, and legacy revenues in the copper-based segments to decline by more than twenty percent. Adjusted EBITDA is expected to grow at a rate of three to four per cent, with the advanced connectivity segment growing at over six per cent.

Management continues to see adjusted earnings per share in the range of two dollars twenty-five to two dollars thirty-five. Free cash flow should reach at least eighteen billion dollars, even after accounting for higher cash taxes and pension contributions.

Between 2026 and 2028, AT&T plans to return more than forty-five billion dollars to shareholders, through a combination of dividends and share repurchases, while reducing debt to a target net debt to adjusted EBITDA ratio of about two and a half. That's the core of the long-term thesis: moderate growth, strong free cash flow, debt reduction, and a stable dividend.

Long-term business development

The last few years have been all about "housekeeping" for AT&T. The company has divested media assets, restructured its portfolio, and started investing aggressively in fiber optics and mobile while pushing down debt. Revenues tended to stagnate to grow modestly after the exit of the media businesses, but the quality of those revenues improved as recurring revenue from connectivity gained more weight.

Operating profit has historically been weighed down by high depreciation and one-off costs, but has gradually stabilised and grown in recent quarters. Free cash flow of around fifteen to sixteen billion dollars a year gives the company room to fund significant capital expenditures, pay down debt and pay a dividend without materially straining the balance sheet.

Today, AT&T looks less like a conglomerate and more like a pure telecom operator with two clear priorities. The first is growth in advanced connectivity via fiber, fixed wireless and mobile, the second is gradual debt reduction and return of capital. From this perspective, Q1 2026 fits neatly into the long-term picture.

Shareholders and capital policy

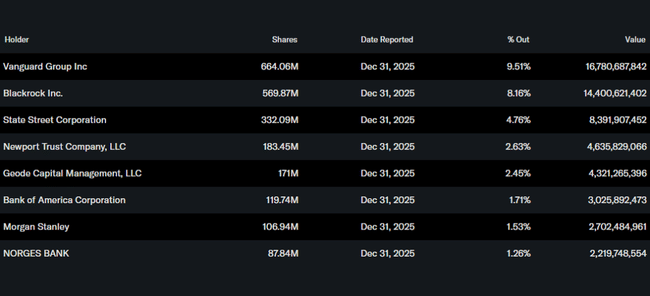

AT&T's ownership structure is typical of a large dividend player. Insiders hold less than one percent of the stock, according to Yahoo Finance, while the institution owns roughly eighty-four percent of the stock and free float. The largest shareholders are Vanguard, Blackrock, State Street and other large global funds, which together control a substantial portion of the company.

The company pays a dividend of $1.11 per share per year, which at the current share price implies an attractive dividend yield in the higher single digits of percentages. In addition, it plans to buy back more than twenty billion dollars worth of its own shares between 2026 and 2028 as part of a package of more than forty-five billion returned to shareholders.

For investors, AT&T today is more a story of steady cash flow than rapid growth. The first quarter of 2026 shows that the company can grow modestly, lift profits in its core connectivity segment, and hold the outlook while sending much of its free cash flow back to shareholders. This makes sense for those looking for yield and stability, not dynamic revenue growth.