Tesla has entered 2026 at a stage where it is no longer just a "pure" growth story built on increasing car production, but increasingly a combination of a car company, an energy company and a technology company focused on artificial intelligence, autonomy and robotics. In the first quarter of 2026, it managed to return to double-digit revenue growth while visibly improving profitability. Revenue grew 16 percent to about $22.4 billion, gross margin rose to 21 percent and free cash flow exceeded $1.4 billion.

At the same time, however, the numbers reveal that this is no longer seamless "linear" growth. Car deliveries are only growing in the lower units of percentages, inventories are rising, and parts of the business, especially energy, are having a weaker quarter after an exceptionally strong year. Management openly says that a big part of today's results and future expectations are massive investments in AI infrastructure, FSD (Supervised), robotaxi and the humanoid robot Optimus. This leaves Tesla as a company with huge potential for investors, but also with increasing complexity and dependence on the success of projects that are just beginning their ramp.

Q1 2026 results

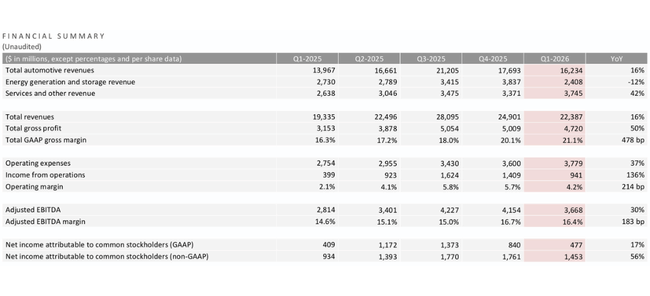

Tesla $TSLA delivered a combination of a return to growth and a distinct shift in profitability in Q1 2026. Revenue reached $22.4 billion, up 16 percent year-over-year from $19.3 billion in Q1 2025. Gross profit increased to $4.72 billion and gross margin rose to 21.1 percent from 16.3 percent a year ago.

Automotive sales rose to $16.2 billion, plus 16 percent year over year, boosted by shipment growth, a higher mix of services and FSD and leasing. In contrast, Energy revenues fell 12 percent to about $2.4 billion, as a weaker quarter in Megapack deployments and lower storage volumes from 14.2 GWh to 8.8 GWh, following an exceptionally strong 2025. Services and Other revenues rose 42 percent to $3.7 billion, reflecting growth in Services, Insurance, Superchargers and other ancillary services.

GAAP operating profit was $941 million versus $399 million a year ago, and operating margin rose to 4.2 percent from 2.1 percent. Adjusted operating profit (non-GAAP) was $1.08 billion versus $770 million last year. GAAP net income attributable to shareholders was $477 million, up 17 percent year-over-year, or $0.13 per share. Adjusted net income was $1.45 billion, with adjusted earnings per share of $0.41, up about 52 percent from a year ago and above consensus of about $0.36 to $0.37.

Operating cash flow in the quarter was $3.94 billion, capital expenditures were $2.49 billion and free cash flow was $1.44 billion compared to $664 million in the same period in 2025. Cash and short-term investments rose to about $44.7 billion, $700 million more than at the end of 2025, even though Tesla is simultaneously funding a large investment program in AI, batteries, robotics and manufacturing.

On the volume side, Tesla produced 408,386 cars and delivered 358,023, a year-over-year increase in deliveries of about six percent but a sequential decline against a strong fourth quarter. The gap between production and deliveries of over fifty thousand cars lifted global inventories to 27 days from fifteen at the end of the previous quarter, one of the points the market is watching with caution.

Management commentary and key messages

On the call, management said that it sees the quarter as a confirmation of a return to growth, but also as a period of massive investment in future business. It highlights several points.

First, continued growth in vehicle demand in Asia and South America and a re-acceleration in Europe and North America after a weaker 2025. Tesla talks about how its strategy of affordability and lower operating costs is competitive, especially at a time when fossil fuels are suffering from volatile prices and geopolitics.

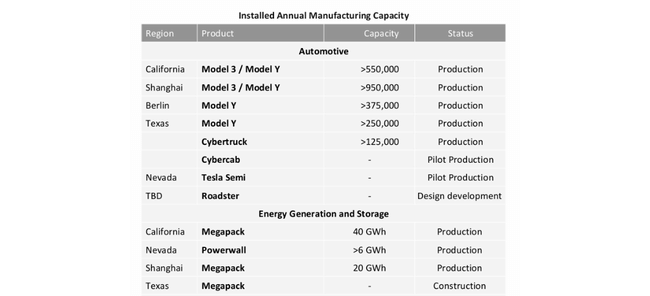

Second, management repeatedly mentions massive investments in infrastructure and AI software for Robotaxi and future robotics businesses. In the first quarter, Tesla began ramping up AI computing cluster capacity, rolling out new battery and materials factories, and preparing lines for Megapack 3, Cybercab, and Tesla Semi. It has begun ramping up LFP batteries in Nevada, cathode materials and lithium refining in Texas, and the company itself says battery capacity is still a major constraint on car production growth.

Third , Musk and the team are making it clear that Tesla is moving from a pure car company to one whose future profits are increasingly to be driven by AI, software and fleet services. In Q1 2026, FSD (Supervised) expansion continued, growing the number of active subscribers to 1.28 million, a year-over-year growth of more than fifty percent, and the company is testing new models for monetizing FSD as a standalone product.

The commentary also acknowledges that this strategy means increased investment in R&D, operations and infrastructure, which will put pressure on operating margins in the short term, but is essential to staying ahead in autonomous driving, robotics and energy, according to management.

Outlook and new projects

Tesla doesn't publish detailed EPS guidance in the earnings release like traditional blue-chip companies, but it does outline key targets for 2026.

For cars, Tesla says it will focus on maximizing the use of existing factories and that delivery and installation volumes will depend on aggregate demand, supply chain readiness, and allocation between sales to customers and its own fleet of Robotaxis. In terms of new products, the company confirms that the Cybercab, Tesla Semi and Megapack 3 are on track for mass production during 2026.

AI and software are a big part of the outlook. Tesla says the latest version of FSD (Supervised) 14.3, launched in April, brings revamped reinforcement learning training to handle long-tail situations, an improved visual encoder for worse conditions, and a rewritten compiler and runtime that cuts inference latency by up to a fifth. This is intended to accelerate development towards fully unsupervised operation for both Robotaxi and customer cars.

In Europe, the major news is the approval of FSD (Supervised) in the Netherlands by the Dutch regulator RDW on 10 April, making the country the first European market to have officially enabled FSD (Supervised) under the UN R-171 standard. Both Tesla and analyst commentators say the move paves the way for a relatively rapid expansion into other European Union countries, notably Germany, France and Italy, with the aim of wider coverage by summer 2026.

Robotaxi continues to grow in the US. Tesla reports that paid Robotaxi miles nearly doubled quarter-over-quarter in the first quarter. It has already expanded its unsupervised service area in Austin and in April launched unsupervised rides in Dallas and Houston, while also preparing to enter other major cities including Phoenix, Miami and Las Vegas. Safety remains a priority, and the company says it continues to test and adjust services to meet regulatory and practical standards.

The Megafactory near Houston is set to start production of Megapack 3 for the new Megablock system this year, which is expected to lift annual storage capacity to tens of GWh. Gigafactory New York has begun shipping new solar panels of its own design with multiple zones for better shade performance and faster installation. At the same time, the Supercharger network is expanding, growing nineteen percent year-over-year and adding over 2,200 new racks in the first quarter.

Optimus represents the most ambitious chapter of the outlook. Management says the first large-scale humanoid robot factory will begin to come online in the second quarter of 2026 in Fremont, where the first-generation line will replace the Model S and X production lines and will be sized for a capacity of around one million robots per year. A second generation line is under development in Texas with a target capacity of up to ten million robots per year in the long term.

Long-term business development

The long-term numbers for 2021 to 2024 show how dramatically Tesla has transformed. Revenues grew from $53.8 billion in 2021 to $81.5 billion in 2022, $96.8 billion in 2023, and $97.7 billion in 2024. After extremely strong growth of more than fifty percent in 2022 and nearly nineteen percent in 2023, the pace nearly stalled in 2024, when revenues added less than one percent.

Gross profit in 2021 was about $13.6 billion, jumping to about $20.9 billion in 2022, only to gradually decline to $17.7 billion and $17.45 billion in 2023 and 2024. Thus, gross margin has been gradually declining after a period of extremely high values due to price discounts, new project costs and competitive pressure. Operating profit first more than doubled from 6.5 billion in 2021 to 13.7 billion in 2022, then fell to 8.9 billion in 2023 and further to 7.1 billion in 2024.

Net income rose from $5.5 billion in 2021 to $12.6 billion in 2022 and nearly $15 billion in 2023, only to fall to about $7.1 billion in 2024. Earnings per share follow this pattern, rising from roughly $1.63-$1.87 in 2021 to $3.62-$4.02 in 2022 and $4.31-$4.73 in 2023 to fall to roughly $2.04-$2.23 in 2024.

Results for the first quarter of 2026 fit this story. After a year of stagnation and declining margins, Tesla is showing a return to 16 percent revenue growth and a significant improvement in gross margin and profitability, but it is also clear that this is no longer a simple story of a "pure-play" automaker that just scales one product. Today's numbers are a blend of services growth, FSD, energy, AI and robotics investments, as well as the cost of maintaining and expanding the technology lead.

Shareholders and ownership structure

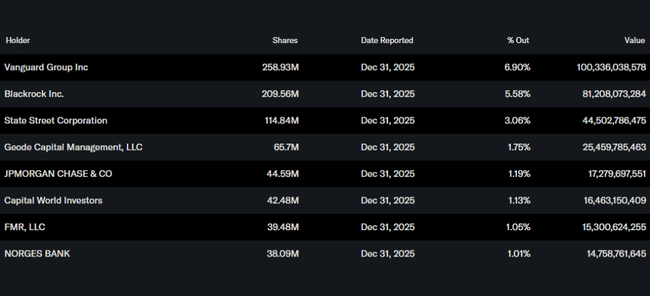

According to the report, insiders hold approximately 11.1 percent of Tesla's stock, which is a high stake for a large company and reflects strong management and founder involvement. Institutional investors own roughly 44.8 percent of the stock and approximately 50.4 percent of the free float, with more than 5,200 institutions holding some stake.

The largest shareholders are large passive and actively managed fund managers. Vanguard owns about 258.9 million shares, nearly seven percent of the company. BlackRock has about 209.6 million shares, or about five and a half percent. State Street holds about 115 million shares and Geode Capital holds about 65.7 million. The dominance of these players means that the share price is very sensitive to changes in sentiment of large funds towards Tesla as both a growth and technology story.

News and strategic shift

Beyond the numbers, Q1 2026 is about the news that frames the company's future. The approval of FSD (Supervised) in the Netherlands is the first major European breakthrough and, along with intensive pre-regulatory testing and thousands of FSD runs in Europe, paves the way for more widespread deployment across the European Union.

Robotaxi is expanding in the US, where Tesla says that paid miles have nearly doubled from the previous quarter and that it is preparing to roll out the service quickly in other cities once testing is complete and the necessary permits are obtained. In AI computing, the company has launched a Cortex 2 cluster with the equivalent of more than 130,000 H100s, is expanding its own development of Dojo 3 chips, and plans to build a large-scale semiconductor fabrication facility for inference chips in partnership with SpaceX.

At the same time, Tesla is pushing digital products such as its own voice assistant Grok in cars, new safety score functionality linked to insurance, and other infotainment services. On the energy side, it continues to innovate with solar panels and the expansion of Megachargers for Semi tractors, with the first public stations of this type already in California.

Overall, Q1 2026 shows Tesla as a company that is returning to growth after a period of margin pressure while aggressively investing in AI, autonomous driving, robotics and energy. For investors, this means the potential is huge, but it also increases the complexity of the story and the dependence on the success of projects that are just beginning to ramp up.