Verizon has had a quarter that confirms that the ongoing transformation is starting to show up clearly in the numbers. Revenues are up to about $34.4 billion, net income is up to $5.1 billion and free cash flow is up slightly even as the company continues to invest heavily in the network and integrate Frontier. From a profitability perspective, the key takeaway is that EBITDA is at record levels and earnings per share is growing faster than sales, giving management the courage to raise its full-year target for earnings per share and free cash flow.

Customer numbers show that the trend is turning in mobile and broadband. Verizon is reporting positive Q1 postpaid phone net adds for the first time in more than a decade, broadband is adding hundreds of thousands of new connections, and mobile/broadband service revenue is growing in a range the company only hinted at as a target at the beginning of the year. All this on top of a quarter weighed down by the January network outage.

Q1 2026 results

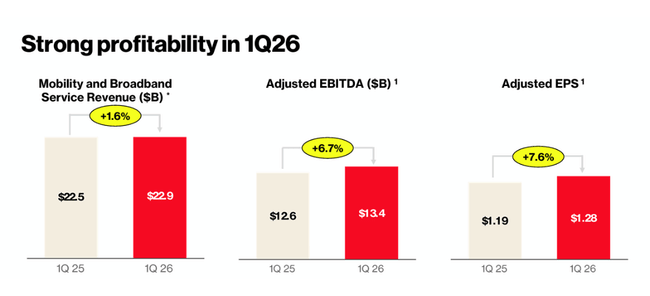

For the first quarter of 2026, Verizon $VZ revenue reached approximately $34.4 billion, representing year-over-year growth of around 3%. Service revenue from mobility and broadband are the main drivers, while device revenue added a few percent thanks to higher sales volume.

Net profit rose to USD 5.1 billion, up about 3% y-o-y, and earnings per share increased several percent, growing faster than sales alone. This reflects a combination of improved margins, savings and lower taxation. Adjusted EBITDA grew to an all-time high of around US$13.4 billion, an increase of almost seven percent year-on-year and a clear signal that the company is maintaining discipline on the cost side.

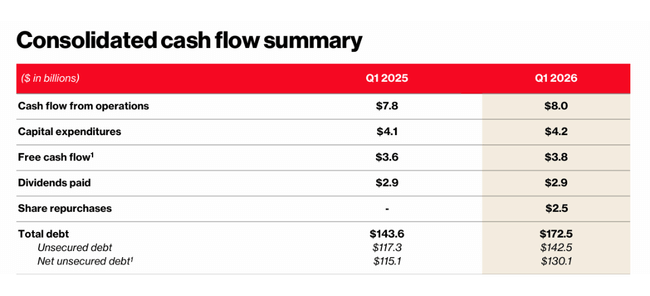

In terms of cash, Verizon generated about USD 8.0 billion from operations in Q1, slightly more than last year. Capital expenditures were around US$4.2 billion, bringing free cash flow up to around US$3.8 billion. This is a solid result for the first quarter of the year, which tends to be seasonally weaker for telcos.

The balance sheet shows the impact of the Frontier acquisition. Total debt increased to over USD 140 billion and net debt to EBITDA jumped in the short term. However, management stresses that it has already repaid about half of the debt assumed with Frontier during Q1 and aims to bring debt back to target by the end of 2026.

Management commentary

Verizon management describes Q1 as further evidence that the company's transformation toward simpler products, better customer experience and more efficient operations is working. CEO Dan Schulman highlights three key points.

First, the improving momentum in mobile services. The firm achieved its first positive Q1 postpaid phone net adds since 2013, despite the fact that traditionally the start of the year is a weaker period for mobile operators. Management interprets this as confirmation that it is managing to attract new customers without extreme promotional aggressiveness while better retaining existing ones.

Second, continued growth in broadband, particularly fixed wireless and fibre. Verizon $VZ added over 300k new broadband connections in the quarter, and management emphasizes that the combination of FWA and fiber is one of the key growth legs of the business for years to come.

Third, the ability to lift profitability despite one-time negative impacts. According to the company, the January network outage reduced service revenue growth by about 0.8 percentage points, yet in March, mobile and broadband service revenue growth was in the middle of the target range. Management is using this as an argument that the fundamental trend is better than the quarterly number alone would suggest.

Transformation, news and strategic moves

Verizon has been operating under a clearly stated transformation plan in recent quarters. This has several specific pillars that translate into numbers and news in Q1.

In mobility, the company continues to simplify its tariff offerings, reduce excessive promotions and focus more on customer value than net volume at any price. This improves ARPU structure and reduces churn. At the same time, investments in the 5G network and capacity expansion continue, which is necessary to maintain quality of service amid rising data demand.

In broadband, Verizon is building on the growth of fixed wireless and expanding its fibre network. The goal is to have a combination of high-speed wireless and fiber optics in response to the growing demand for higher-speed home Internet, both for residential customers and smaller businesses. The Frontier acquisition fits here as an opportunity to expand footprint while capitalizing on synergies in operations and infrastructure investment.

On the financial side, cost-saving programmes continue. Verizon has set a multi-year goal to reduce operating costs in the billions of dollars, and Q1 shows that this program is on track. Improved EBITDA margins and earnings per share growth faster than revenue show that this is not just "hyped" results, but a real change in efficiency. At the same time, the company is maintaining a strong dividend policy and adding a buyback of its own shares on top.

Long-term numbers

Verizon's long-term numbers show that the company is not a growth stock in the classic sense, but rather a defensive cash flow generator. Revenues have been mostly stagnant or growing in the low single-digit percentages annually in recent years, in an environment of heavy investment in 5G, spectrum and optics.

Meanwhile, profitability has historically suffered from a combination of high debt, costly spectrum auctions and a highly competitive environment. But over the past two years, we have seen a trend where adjusted earnings per share and free cash flow have been gradually increasing, even if revenues as a whole have not accelerated dramatically. This is exactly the picture of transformation: the company is not adding as much to the top line, but it is improving customer mix, cost structure and capital discipline.

Q1 2026 fits into this story. Rather than a big jump in revenue, it's a visible improvement in profitability, cash flow and customer metrics, on top of an increased outlook for the full year. For an investor looking for a stable dividend title with decent free cash flow and gradually improving fundamentals, these are exactly the kind of numbers they want to see from Verizon.

Shareholders

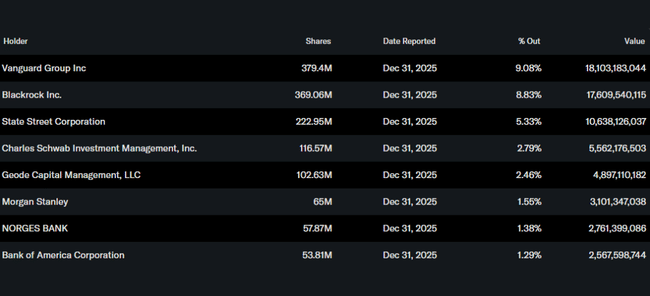

Verizon remains a heavily institutionally owned stock. Most of the shares are held by large asset managers, including funds like BlackRock and Vanguard, which together control high units of percent of the company. Insiders own only a small stake, which is standard for large telcos.

The company has a long history of stable dividends and regular dividend payment growth. Combined with free cash flow in the tens of billions of dollars a year, this makes it a popular title for income investors. At the same time, Verizon uses buybacks to reduce the number of shares outstanding, which promotes earnings per share growth even in years when earnings add little.