Tesla’s latest quarter captures the paradox of its current phase: operationally stronger than ever, financially resilient, yet increasingly constrained by the limits of profitability. The company continues to post record deliveries and robust cash generation while pushing deeper into its transformation from an automaker to a broad-scale AI, energy, and autonomy platform.

Behind the headline numbers, however, lie growing costs, margin compression, and a more competitive global EV landscape. As tariffs, price cuts, and production mix reshape Tesla’s economics, investors are forced to reconcile the company’s dual identity — a manufacturing powerhouse and a technology story under pressure to prove it can still grow profitably in a maturing market.

How was the last quarter?

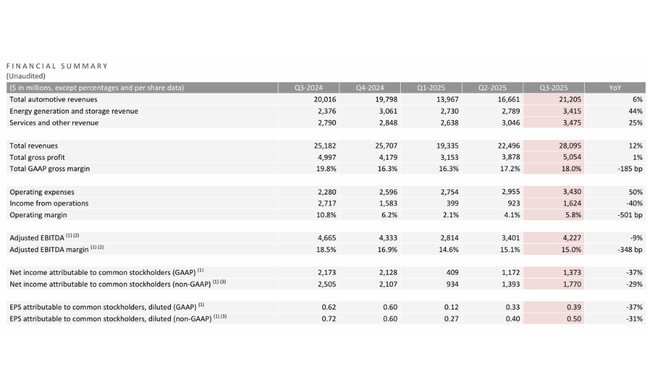

In the third quarter of 2025, Tesla $TSLA increased revenue to about $28.1 billionwhich means 12% year-over-year growth. Driven primarily by higher vehicle deliveries and very strong growth in the energy and services segments, the pure automotive segment grew at a single-digit rate, while energy (batteries and solar) added more than 40% and services and other revenue added about a quarter. Thus, it appears that the company is gradually shifting from a pure "car-company" to a broader technology and energy platform.

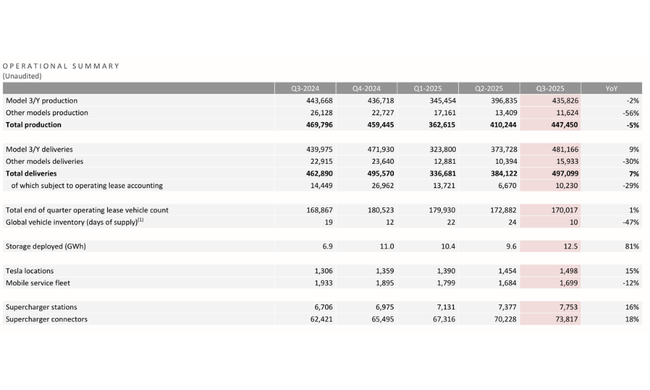

This volume growth is mainly driven by mainstream models. Tesla delivered in the quarter over 497,000 vehiclesof which more than 480,000 were Model 3 and Model Y, a roughly 9% year-over-year increase in this key pair. In contrast, other models (S, X, Cybertruck and others) declined in volume, which is reflected in the overall mix - the company is increasingly dependent on "folk" models. The positive news is that Tesla's inventory turnover has accelerated significantly: the number of days of new car inventory has dropped to around ten, which is significantly lower than a year ago and previous quarters.

Even more interesting is the development in the energy sector. Tesla has deployed in Q3 roughly 12.5 GWh of storage, which is a jump of more than 80% from last year and a new record. Thus, the energy segment is no longer just an "appendage" but is becoming a visible business pillar. Energy revenues are growing much faster than the automotive sector and are also making a positive contribution to gross margin.

Profitability as a whole is under pressure. Gross profit was virtually unmoved year-on-year and overall gross margin held around 18 %below the levels Tesla achieved in the golden days of high prices and minimal competition. Operating profit fell to about 1.6 billion dollarswhich is down 40% from a year ago., a operating margins fell to 5,8 %. The main culprits are rising operating costs (especially SG&A and R&D related to AI and new projects), higher stock-based compensation, lower revenue from emission credits, the absence of a one-off FSD effect that helped the comparable period last year, and pressure on unit costs due to lower fixed absorption on some models, higher tariffs and a less favourable sales mix.

At the net income level, Tesla reported GAAP profit of around $1.4 billion, which means a decline of roughly one-third from the prior year. Non-GAAP profit, adjusted for certain items, fell at a similar rate. But the picture wouldn't be complete without looking at cash flow: operating cash flow was approximately $6.2 billion and with lower capital expenditures. free cash flow climbed to a record high of about $4 billion. This shifted the cash and investments position to more than $41.6 billionfive billion more than in the second quarter. Simply put - book profits are down, but cash is flowing.

Outlook and strategy

Tesla doesn't divulge as much directly in the numbers for the period ahead, but the bottom line is clear from management's comments: in the short term, pressure on margins and high uncertainty due to tariffs, trade policy and fiscal changes; in the long term, a drive to build the company around three pillars - transport, energy a Robotics/AI.

In the automotive sector, Tesla is responding to cooling demand and fierce competition with a combination of a wider range of products and an emphasis on more affordable options. In the U.S., it launched the Model 3 Standard and Model Y Standard with a range of over 300 miles and priced under $40,000 to mitigate the impact of the expiration of some tax incentives and to maintain volume. It also offers a more powerful Model Y Performance and expands financing and leasing options, including certified used cars. The goal is to utilize existing manufacturing capacity in California, Texas, Shanghai and Berlin, improve fixed absorption and expand the addressable market.

Even more strategically important than the new options is the move towards autonomy. In the Bay Area, Tesla has launched ride-hailing service using Robotaxi technologyto test the next step in fleet monetization. Each newly delivered car is designed for autonomy and software - including "Full Self-Driving" - that is expected to be a source of recurring revenue once regulation and technology allow for more mass deployment, according to the company.

At the same time, the energy business is growing in importance. Products such as Megapack 3 and Megablock are intended to simplify and cheapen large storage installations for utilities and industry, creating another vertical where Tesla is on the cutting edge. Each energy product is designed to be plugged into virtual power plants and optimized using "Autobidder" or other AI tools.

The company's leadership openly says that there is no getting around short-term turbulence in tariffs, subsidies or global trade. The answer is to scale the core business, invest carefully in future lines (especially autonomy and robotics), and use a strong balance sheet to help Tesla survive the "price war" phase in the EV segment without sacrificing long-term growth potential.

Long-term results

The last four years show the Tesla story in several acts. The first act - 2021 to 2022 - was a period of explosive growth and margin expansion. Revenue grew from roughly $54 billion in 2021 at $81 billion in 2022that's more than 50%, while at the same time, profitability was also soaring. Gross profit soared to more than 20.8 billion, operating profit exceeded 13.6 billion, and net income more than doubled. Margins then benefited from a unique combination of high demand, relatively little competition, strong pricing power and production scaling effects.

The second act comes between 2023 and 2024. Revenues continue to grow, but at a dramatically slower pace, hitting 96.8 billion in 2023 and jumping only slightly to 97.7 billion in 2024. Growth has slowed while pricing pressure in the EV segment has intensified. This can be seen in gross profit, which after peaking in 2022 started to decline - falling from 20.9 billion to 17.7 billion in 2023 and 17.5 billion in 2024.

At the same time, operating costs are rising significantly. Research, development and administrative expenses have risen from roughly 7.2 billion in 2022 to more than 10.3 billion in 2024. Some of this is investment in the future - AI, autonomy, robotics, new models and factories - but some of it reflects a more complex environment, legal costs and the broader scope of the company. The result is that operating profit has gradually declined from a peak of 13.6 billion in 2022 to 8.9 billion in 2023 and to 7.1 billion in 2024.

The most obvious break comes at the net profit level. Roughly 12.6 billion in 2022 has turned into 15 billion in 2023, another very strong year, but 2024 brought a sharp drop to 7.1 billion. Earnings per share fell from roughly $4.73 to 2.23 USDor more than half. The extremely favourable tax effect in 2023 (negative tax expense), which did not return in 2024, played a role in this, while operating pressure remained.

If we look at Tesla through an EBITDA lens, the story is less dramatic, but the trend is similar. After rocketing to more than $17.6 billion in 2022, EBITDA is around $14.8-14.7 billion in 2023 and 2024, stable but no longer expanding. The company is thus at a crossroads: volumes are high, revenues are near $100 billion, but further margin improvement will require either a significant technology advantage or a shift of the business towards a higher share of software, services and energy.

Shareholding structure

Tesla's ownership structure is a hybrid between a technology growth stock and a "cult" stock with significant insider influence. Roughly 12.5% of shares are held by insiders - namely Elon Musk and other key individuals - which is an exceptionally high proportion for a company of this size. The institution owns approximately half of the company and holds more than 56% of the free float.

The largest institutional shareholders are again funds Vanguard - Total Stock Market Index Fund and 500 Index Fund, which together hold over 5% of the firm. This is followed by large passive players such as Fidelity 500 Index Fund a iShares Core S&P 500 ETF. This means that a large portion of the stock is in the hands of long-term index investors, which provides some stability, but also leads to Tesla being very sensitive to changes in sentiment towards growth and technology titles as an asset class.

Investor expectations

Investors today see two layers to the Tesla story. The first, visible and measurable, is the conventional electric car and energy storage business - here the company is expected to continue to grow in volume, but in an environment of fierce competition and regulation, it will have to live with lower margins than it has become accustomed to in recent years. Success here will be measured by whether it can sustain double-digit growth in the energy business, stabilise automotive margins, while generating strong free cash flow.

The second, more speculative layer is the story AI and autonomy. Robotaxis, ride-hailing, autonomous driving software, energy algorithms and the potential of humanoid robots all make up the "option value" that investors are projecting into the stock to varying degrees. If Tesla can prove that any of these projects can generate billions of dollars in high-margin profits, it could completely change the valuation of the company and return it to the category of growth icons. If not, Tesla will more closely resemble a "big carmaker with a technological overhang".

Thus, in the coming quarters, the market will be watching two numbers in particular: the evolution of automotive margins and the growth rate of the energy sector, complemented by specific milestones in autonomy and Robotaxi services.