Few companies embody the concept of “steady growth through sustainability” like Waste Management. The U.S. waste giant delivered record quarterly revenue and cash flow, proving that even traditional industries can thrive in the age of decarbonization. Its core business — waste collection, landfills, and disposal services — remains highly profitable, while strategic bets on recycling and renewable natural gas are now paying off.

The company’s acquisition of WM Healthcare Solutions expanded its reach into medical waste, a lower-margin segment for now but one that opens a new growth frontier. As commodity recycling prices fell sharply, WM still managed double-digit gains in revenue and cash flow. It’s becoming less a garbage collector and more a circular-economy powerhouse built on operational excellence and green innovation.

How was the last quarter?

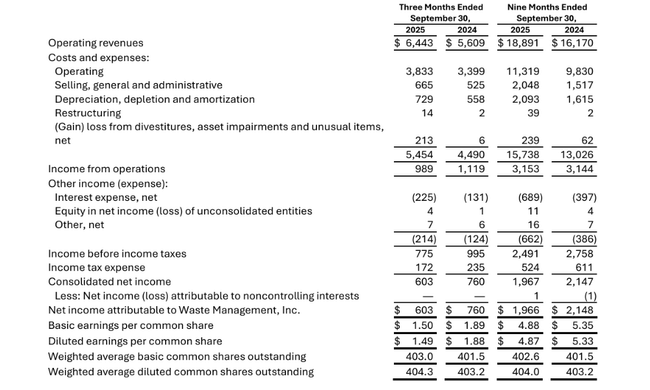

In the third quarter of 2025 $WMreached $6.44 billion in revenue, a year-over-year growth of roughly fifteen percent. The majority is still made up of the so-called legacy business - that is, traditional collection, landfill and recycling - which has grown to $5.8 billion. The rest was accounted for by WM Healthcare Solutions' new medical waste division, which added another roughly 0.6 billion.

Profitability held at a very solid level. Operating EBITDA was about $1.72 billion, about $1.97 billion on an adjusted basis. That equates to an adjusted margin of over 30%, with the legacy business alone around 32% on an adjusted basis. Even more attractive is the core business - waste collection and disposal - where the adjusted EBITDA margin came in at around 38%, demonstrating the strong pricing power and operating efficiencies the company has in this segment.

The healthcare segment is weaker in terms of margins so far, but it is growing. WM Healthcare Solutions brought in sales of about $628 million and EBITDA of about $89 million in the quarter, and on an adjusted basis, $110 million, a lower but gradually improving margin. Management openly says there is integration and optimization work underway, so the current numbers are more floor than ceiling.

From a cost perspective, we can see a shift in the right direction. In the legacy business, adjusted operating expenses have declined relative to revenue by about 1.6 percentage points. Better driver retention, a targeted move away from low-margin municipal contracts and higher utilization in landfill and industrial hauling are helping. SG&A costs in the legacy division remain disciplined at around nine per cent of revenue, a very reasonable level for such a capital-intensive business.

On the net profit front, the company is down year-on-year, with reported profit falling to around $603 million compared to $760 million a year ago. But after adjusting for one-time items, the picture is reversed: adjusted net income rose to roughly $801 million, and adjusted earnings per share rose from $1.96 to $1.98.

Management Commentary

Commenting on the results, CEO Jim Fish highlighted three key drivers: discipline in growth, cost optimization and expansion of sustainable operations. Collections and landfill, he said, is going through a "record margin period", which is evident in the numbers - margins in this segment are historically very high, despite weaker prices for recycled materials.

At the same time, management notes that the recycling and energy segments have also managed to increase operating EBITDA year-on-year despite a roughly one-third drop in commodity prices. This is a direct result of heavy investment in sorting automation and in the production of renewable natural gas from waste. In other words, the business can now extract more value from a tonne of waste than it used to.

WM Healthcare Solutions is more of an investment phase at the moment - integrating people, processes and IT running across 16 geographies. But management stresses that it wants to be selective in its approach to clients and is pushing for long-term contract longevity, not quick volumes at any cost. In the short term, this also means deferred price increases for some customers, but in the long term, more stability in revenues.

From a cash flow perspective, management remains very confident. In the first nine months of the year, the company generated more than $4.3 billion of operating cash flow, up roughly 12 percent from last year, and free cash flow of about $2.1 billion has picked up even faster. At the same time, the company has been steadily reducing debt and is heading toward a target leverage ratio of 2.5-3.0× EBITDA by mid-2026.

Outlook

For 2025, WM confirms that it is targeting adjusted operating EBITDA in the range of approximately $7.5 billion to $7.6 billion. This would imply further year-on-year growth and an EBITDA margin of roughly 29.5 percent to slightly above 30 percent, with the upper end of the range raised slightly by the company. Free cash flow should be between $2.8 billion and $2.9 billion, even after taking into account the fact that the company is gradually moving from the investment phase to the "harvest" phase for its sustainable projects.

At the revenue level, management is more cautious. Full-year revenue is now expected to be around $25.3 billion, more near the lower end of the original range. Structurally, however, the outlook remains positive. The core business still has room for moderate growth driven by price, moderate volume growth and efficiency. Sustainable energy and recycling are adding higher percentage growth, albeit from a smaller base, and medical waste is expanding its service offering to clients. Together, these three directions should keep WM in a stable revenue growth and free cash flow mode over the long term.

Long-term results

A look at the last four years shows an extremely consistent growth profile. WM's revenues have grown from roughly $17.9 billion in 2021 to $22.1 billion in 2024. While the rate of growth has fluctuated slightly - from roughly ten percent just after covide to three to eight percent in subsequent years - the direction is clear: a steady expansion of the business within a relatively unpretentious but regulated industry.

Even more interesting is the evolution of profitability. Gross profit grew from roughly 6.8 billion in 2021 to 8.7 billion in 2024, growing faster than sales alone. That means the company is either pricing services better or gaining operational efficiencies - and probably both. Meanwhile, the cost of output sold is rising, but more slowly than would be consistent with pure volume growth - and in an environment where wages, fuel and equipment maintenance are all going up over the long term.

At the level of operating profit, the story repeats itself. Operating profit has risen from just under three billion dollars in 2021 to over four billion in 2024. EBITDA has risen from around 5 billion to around 6.4 billion. That means not only the ability to grow, but more importantly, the ability to grow profitably, which is certainly not a given in a capital-intensive industry that requires constant investment in fleets, landfills, recycling lines and now energy facilities.

Net income rose from about $1.8 billion to $2.7 billion over the same period, and earnings per share from about $4.3 to $6.8. At the same time, the company is gradually reducing the number of shares outstanding, so EPS growth is still a bit faster than overall earnings growth. Thus, WM is able to combine business growth, margin expansion, stable dividends, and a buyback on top of that, which is a very attractive mix for long-term investors.

What's also interesting is that WM delivers these numbers over a cycle. Even in years when the economy slowed and some industrial volumes or prices of recycled commodities went down, the company was able to maintain revenue growth and profitability. Waste is simply generated in good times and bad, and WM has been able to add more and more technological and sustainable layers to this "boring" nature of the business, increasing the value of every ton that passes through the system.

Shareholder structure

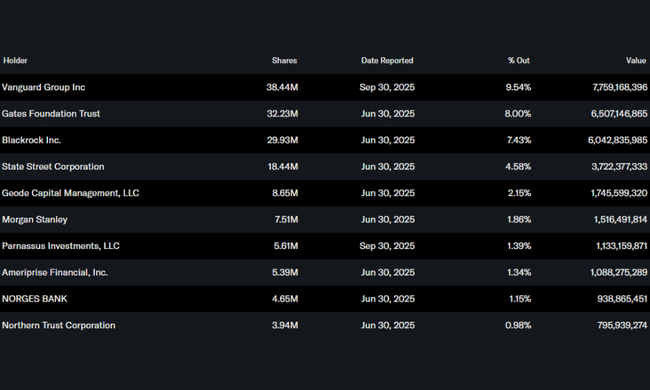

WM is a typical "institutional darling". Only about a quarter of a percent of the shares are in the hands of insiders, while the institution holds about 85 percent of all shares and free float. As a result, the title is a fixture in large index and actively managed portfolios, adding to liquidity while ensuring a relatively stable shareholder base.

The largest shareholder is the Vanguard Group with a stake of around 9.5 percent. The Gates Foundation Trust also has a strong position with around eight per cent, which is an interesting signal in terms of the perceived sustainability and long-term nature of the business. Other large holders include BlackRock with around 7.5 per cent and State Street with just under five per cent. In total, WM is held by over two and a half thousand institutional investors.

This ownership structure means that management is under constant scrutiny by long-term, often conservative investors who emphasize stable cash flow, reasonable debt, discipline in capital spending, and a consistent dividend policy. This fits well with how WM's business actually operates.

News

- Launched four new growth projects: two renewable natural gas facilities in Texas and California and two recycling projects (a new plant in Texas and an automation facility in California).

- In total, 10 of the originally planned 20 RNG projects and 31 of the 39 recycling projects are already in operation, meaning the investment wave will gradually tip into the "harvest" phase of higher margins.

- Continued integration of WM Healthcare Solutions across 16 geographies, including the alignment of sales and back-office processes and pricing alignment.

- Improving debt leverage through rising EBITDA and debt repayments; the company targets a leverage ratio of 2.5-3.0x EBITDA around mid-2026.

- Confirmation of full-year guidance for adjusted EBITDA and free cash flow, despite weaker recyclable commodity prices and slower ramp-up of the healthcare segment.

Analysts' expectations

WM has long been viewed as a defensive growth title - it is not a "rocket" company, but one where the market typically expects a combination of moderate revenue growth and stable to moderately expanding margins, supported by predictable free cash flow. The third quarter rather reinforced this perception - the core business did not disappoint with its performance and the sustainable segments showed that they can grow even in an environment of unfavorable commodity prices.

As a result, analysts typically focus on three questions at WM: how fast cash flows will grow in the coming years, what will be the return on capital for large sustainable projects, and how smoothly WM Healthcare Solutions will be integrated and profitable. If the company meets its own guidance of an EBITDA margin of around thirty percent and free cash flow near three billion dollars per year, it should easily defend its place among the "core" long-term positions in the portfolios of large investors.