In a category defined by intensity and constant reinvention, Monster Beverage has reclaimed its position as the brand that sets the pace. This quarter showed that the company hasn’t lost an ounce of momentum — it’s innovating aggressively, expanding globally, and regaining the operating discipline that once made it the envy of the beverage industry. The cultural icon of the energy drink world is evolving, not aging.

Revenue growth surged into the double digits, international markets strengthened their role as the company’s primary growth engines, and margins climbed back to pre-pandemic highs. After a few uneven years, investors now see a company returning to peak form — bold, profitable, and once again leading the global energy drink race.

How was the last quarter?

Monster Beverage $MNST confirmed that its brand and business model still have tremendous strength. The third quarter brought another record and, most importantly, a return to the form that investors have come to expect from this company. The company benefited from a combination of growing demand for premium energy drinks, thoughtful pricing and expansion in foreign markets. Moreover, the growth momentum was accompanied by a marked improvement in margins, indicating that management is successfully managing not only to generate higher revenues but also to streamline the operating structure.

Driving the results remained the flagship Monster Energy range and its derivatives Reign Total Body Fuel, Reign Storm and Bang, which together form the heart of the portfolio. The company recorded double-digit growth across segments and regions, with key markets in Europe and Asia continuing to increase their share of total revenue. This is proof that the strategy of globalisation and expanding distribution channels is delivering tangible results. Gross margins improved thanks to lower production costs and more efficient inventory management, while operating profit grew at a significantly faster rate than revenue itself. As a result, Monster is achieving one of the best profit to sales growth ratios in its history this year.

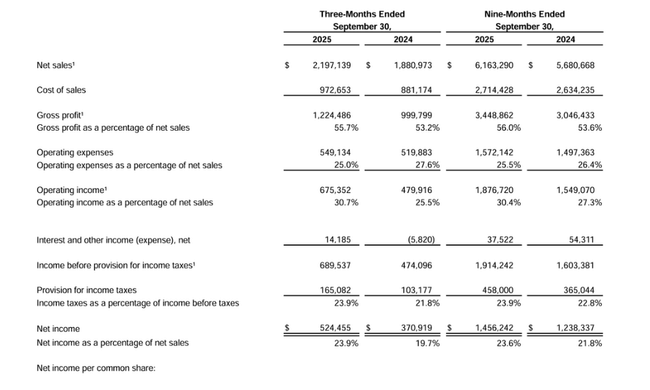

- Revenues: USD 2.20 billion → +16.8% year-on-year (USD 1.88 billion in Q3 2024).

- Gross margin: 55.7% → improvement from 53.2% a year ago.

- Operating Income: USD 675.4 million → +40.7% year-on-year.

- Net Income: USD 524.5 million → +41.4% year-on-year.

- Earnings per share (EPS): USD 0.53 → +41.1% vs. USD 0.38 last year.

- Operating expenses: USD 549.1 million → 25% of sales (down from 27.6% last year).

- Foreign sales: USD 937.1 million → +23.3% yoy, accounting for 43% of sales.

While the core energy portfolio is pulling results up, the alcohol division is struggling with a decline in demand. This segment remains complementary for the company and recent developments show that management's focus remains on the key soft energy drink market where Monster has the greatest margin potential. Overall, however, the quarter sent a very strong signal to investors - Monster was able to improve performance, strengthen financial stability and expand its international reach without negatively impacting efficiency.

CEO comment

In particular, management highlighted the strength of the core business and Monster's ability to respond to changing consumer preferences. CEO Rodney Sacks spoke of the combination of "disciplined growth" and "long-term thinking" that protects the company from market fluctuations. He said the focus remains on strengthening the brand while investing in innovation in areas that add value for customers. These include new formats, healthier product variants and locally adapted flavours that can appeal to a wide range of customers.

Sacks also stressed that Monster sees competition not only in the energy drink world, but also in the broader context of functional beverages that combine energy, health and performance. Management's goal is to maintain the growth trend without exaggerated fluctuations, which is to be ensured by a combination of a strong brand, research and tight cost controls.

Outlook

Although the company did not provide specific numerical guidance for the next quarter, signals from management and the market point to a continued growth trend. Key segments, notably Monster Energy and Reign, continue to have strong traction, while expansion in emerging markets provides scope for further volume increases. The evolution of aluminium and other input prices, which have historically impacted margins, will also be an important factor for the period ahead. However, the company is in a favourable position due to its volumes and bargaining power.

In terms of long-term strategy, investments in product innovation and marketing activities are expected to continue, with an emphasis on digital channels and partnerships with major sports brands. Monster thus continues to build on its combination of authenticity, performance and global recognition, which is a key competitive factor in its segment.

Long-term results

Historically, Monster remains one of the few players that has been able to grow consistently even in an environment of volatile commodities and changing trends. Since 2021, revenues have increased by more than a third and the company is approaching the $7.5 billion annual sales mark. Gross and operating margins have remained exceptionally high over the long term, confirming the strength of the brand and management's ability to manage costs.

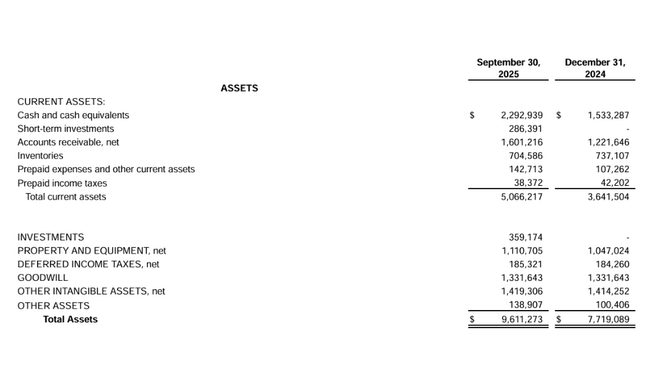

While 2024 brought a short-term decline in net profit, current results show a return to the original momentum. EBITDA and operating cash flow remain stable, allowing the company to finance expansion from its own resources without significant debt. From an investor's perspective, Monster represents a typical growth company with a healthy balance between expansion and profitability - a combination that competitors have been unable to replicate over the long term.

News

- Monster achieved all-time high sales, driven primarily by its core energy drink portfolio.

- International sales exceeded 40% of total sales for the first time.

- Gross margin increased due to more efficient production and a stronger pricing position.

- The company strengthened its cooperation with Coca-Cola in distribution and logistics.

- The alcohol division remains a weaker link, but management confirmed that its contribution to the group will be re-analysed.

Shareholding structure

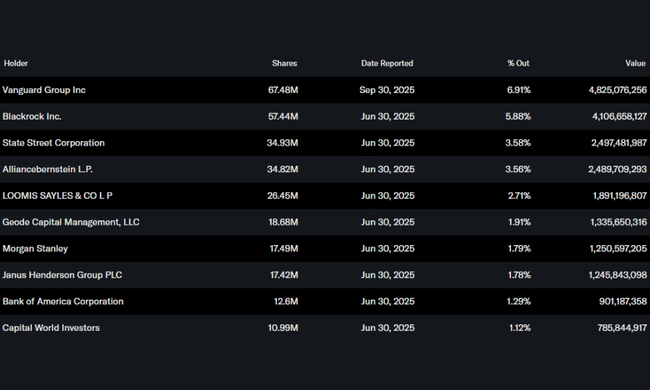

Monster Beverage has an extremely strong and stable ownership base. Insiders, i.e. the management and founders of the company, own approximately 28.6% of all shareswhich ensures a high degree of control over strategic direction and continuity of leadership. The remaining majority of shares are held by institutional investorswho hold approximately 69% of all shares and more than 96% of the free float.

The largest shareholders include:

- Vanguard Group Inc. with a 6.9% stake (67.5 million shares)

- BlackRock Inc. with 5.9% (57.4 million shares)

- State Street Corporation with 3,6 % (34,9 million shares)

- AllianceBernstein L.P. with 3,6 % (34,8 million shares)

This mix of founder clout and strong institutional backing provides Monster stock with stability, low volatility and high long-term investor confidence.

Analysts' expectations

The market views the results as confirmation that Monster is returning to a steady growth trajectory after a challenging period. Analysts expect double-digit growth rates to continue through at least the first half of 2026, with the ability to maintain gross margins above 55% remaining a key factor in further valuation appreciation.

Increasing geographic diversification, which reduces dependence on the US market, is also a positive factor. While competitive pressure in the premium energy drink segment and the eventual normalisation of pricing power in the retail sector remain risks, Monster has so far confirmed that its brand has the strength to stand up in an environment of increased competition and changing consumer sentiment.