Boeing’s third quarter offered the first real glimpse of a company slowly regaining its footing after years defined by production turmoil, regulatory scrutiny and repeated certification setbacks. Encouraging signs emerged across its commercial programs, where output is becoming more predictable and operational stability is gradually returning. The improvements aren’t dramatic yet, but they signal the start of a recovery phase investors have been waiting for.

Still, the company is far from clear skies. The 777X — once touted as Boeing’s flagship long-haul aircraft — continues to drag on results as certification delays mount and accounting charges pile up. Even so, the quarter wasn’t without strengths: a rising backlog, better delivery volumes and incremental progress in defense operations. Boeing is moving forward, but the path ahead remains long, technical and demanding.

What was the last quarter like?

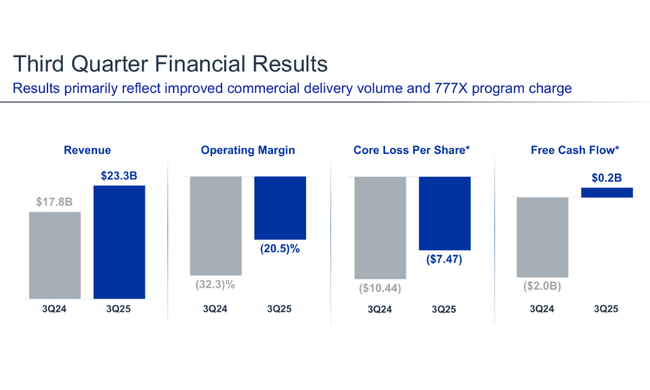

Boeing $BA reported revenues of $23.3 billion, up 30% year-over-year. The commercial division was the driver, delivering 160 aircraft - the most since 2018. Higher deliveries were key to the company's ability to generate operating cash flow in excess of $1 billion and even slightly positive free cash flow. This is a major milestone as the company has struggled with long-term negative operating cash flow in recent years.

Profitability, however, has been hit significantly by another revision to the 777X program. Under the new certification schedule, a $4.9 billion pre-tax charge had to be booked, resulting in a net loss of $5.3 billion and a significant loss per share. While operating performance is improving, the structural costs of this program remain the biggest issue for Boeing as a whole. Without this exceptional item, however, the results would clearly point to a gradual recovery of the core parts of the business.

Also significant was the improvement in the Defence and Space segment, which is returning to better numbers after a string of losses. Defence contracts delivered stronger sales and a positive operating margin, which helped offset some of the pressures in the commercial aerospace division. The company's total backlog rose to $636 billion, reflecting robust global demand for new aircraft and military systems. Despite persistent near-term pressures, the results showed that the company has a strong portfolio and demand that can serve as the basis for a gradual return to profitability in the years ahead.

CEO comment

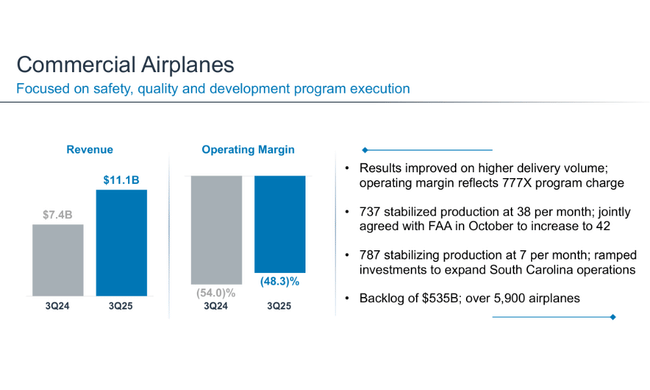

Kelly Ortberg emphasized that Boeing is gradually completing the steps necessary to stabilize the company after the technology, regulatory and reputational shocks of recent years. He thanked employees for the improvements in discipline and quality that have made it possible both to hold 737 production steady at 38 units per month and to gain FAA approval for a phased increase to 42 units. It is this shift that Ortberg said is proof that the relationship with the regulator is moving in the right direction.

He has taken a frank approach to the 777X program, describing the shift in certification as a disappointment, but one that he says is not indicative of the quality of the aircraft, but of the complexity of the regulatory environment. He stressed that test flights are going well, but work needs to be completed on processes, supply chains and production readiness. He reiterated several times in his comments that the company needs to regain the trust of customers and partners and that "there are no shortcuts".

Ortberg also talked about how he sees 2025 as a transition year - the key will be to maintain positive cash flow, stabilise production and gradually increase productivity. Only then can a return to historic levels of profitability be expected.

Outlook

Boeing expects the coming months to be characterized by a gradual increase in production in the commercial division, stable demand for the 737 and 787, and continued backlog growth. Meanwhile, management expects cash flow to remain positive and improve with each increase in production cadence. The company also confirmed that its priority is to reduce debt, which remains at a high level.

In terms of profitability, however, the outlook will be cautious. The revision of the 777X program means that the return to stronger margins will be slower and will likely be delayed until 2027-2028. For the defense division, Boeing expects to see a gradual improvement in performance as troubled programs are stabilized and new contracts are awarded. On cash flow, the company expects a positive full-year result and a significantly stronger 2026 due to higher delivery volumes as well as a gradual leveling off of exceptional costs.

Long-term results

Boeing's long-term financial trajectory has been marked by an extensive period of losses, which has resulted in very weak 2024 results. The firm's revenues have been in the range of $62 billion to $78 billion per year for the past four years, but profitability has been highly volatile. While 2023 was close to operating profit, 2024 brought a plunge into deep losses with negative operating margins. This reflects long-term supply chain issues, aircraft rework costs, certification delays, and multiple costs associated with regulatory requirements.

The year 2024 showed a negative operating result of over $10 billion. Losses were compounded not only by exceptional items but also by rising production and logistics costs. In addition, revenue growth in the commercial division was partially offset by weaker performance in defence. EBITDA has also been extremely volatile in recent years, ranging from positive values of over 2 billion to deep negative values. The high costs have been fully reflected in earnings per share, where Boeing has been in the red almost continuously in recent years. This reflects the structural burden of the 737, 787 and 777X programs.

Although current trends point to improvement in 2025, the accounting history of recent years is a testament to the extent of the problems the company has experienced. The long-term numbers prove that the road to recovery will not take a few quarters, but likely several years. Full normalisation will require stable production, error-free deliveries and a restoration of confidence from regulators and airlines.

News

- Boeing and FAA agree to increase 737 production to 42 units per month.

- The 777X program has undergone a major schedule revision, resulting in an accounting cost of $4.9 billion.

- The Defense Division won a new contract from the U.S. Space Force and expanded its cooperation with the Australian Air Force.

- 787 production continues with planned capacity expansion in South Carolina.

- Backlog exceeded $636 billion, the most in company history.

Shareholders

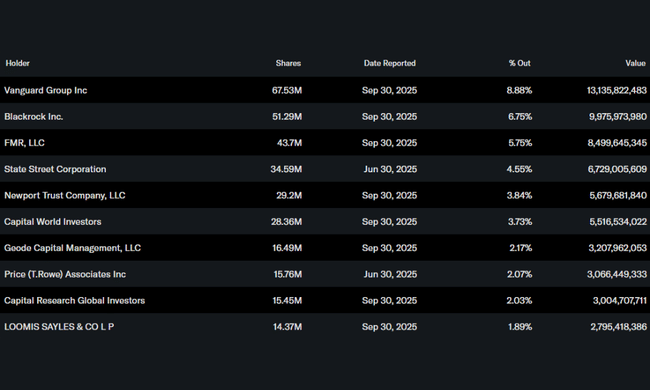

Boeing's ownership structure remains firmly in the hands of institutional investors, who control more than 74% of all shares. The largest shareholder is Vanguard Group with approximately 8.9% of all shares, followed by BlackRock and FMR, with each of these investors holding tens of millions of shares. Insider holdings remain minimal - below one-tenth of one percent. The high share of institutional investors confirms that Boeing remains one of the key long-term positions of large pension funds and ETFs tied to the U.S. index market.

Analysts' expectations

Analysts view Boeing's situation as the beginning of a possible recovery, but one that will be gradual and contingent on production stabilization. They view the ongoing problems of the 777X program as the biggest fundamental risk to the profitability outlook. Although the market reaction to the results was mixed, the consensus is that positive cash flow and increasing delivery rates will create a firmer foundation for margin improvement in the years ahead.

The expectation is that 2026 could already deliver a more significant improvement in operating profitability if the increased 737 production and increased 787 production rates can be sustained. Analysts stress that continued strengthening of quality processes and close cooperation with the FAA will be key.