AbbVie closed the third quarter with results that highlight the resilience of its post-Humira strategy. Immunology and neuroscience remain the primary engines of expansion, while aesthetics and oncology add balance to the broader business mix. The company’s continued ability to generate top-line momentum underscores the strength of its diversified pipeline. Yet the quarter also reveals mounting pressures on profitability as AbbVie pours more resources into research, clinical development, and portfolio-expanding acquisitions.

At the same time, the numbers make it clear that AbbVie is entering one of its most investment-intensive periods in years. The company is allocating substantial capital to programs in autoimmunity, migraine, neurodegeneration and further immunology research — decisions that inevitably weigh on GAAP performance. Even tak, AbbVie maintains key advantages: robust cash flow, fast-growing blockbusters Skyrizi and Rinvoq, and the confidence to raise its dividend once again for 2026. These factors give investors reassurance that near-term margin pressure is part of a deliberate long-term growth strategy.

How was the last quarter?

AbbVie $ABBV ended the third quarter of 2025 with very strong revenue growth, with consolidated revenue rising to $15.776 billion, a nine per cent rate on a reported basis and 8.4 per cent at constant currency. Immunology again drove the results, bringing in nearly $8 billion, representing nearly 12 percent growth. Dominance was confirmed by the pair of Skyrizi and Rinvoq, which together replace the earlier reliance on Humira. Skyrizi, with revenues of $4.708 billion, grew 46 percent year-on-year, while Rinvoq added 35 percent to reach $2.184 billion. In contrast, Humira continued to retreat rapidly, with revenues falling more than 55 percent, but the company had long expected this.

The neuroscience portfolio also delivered strong growth, with revenues of $2.841 billion, up more than 20 percent year-over-year. Vraylar, Botox Therapeutic and the migraine treatment segment (Ubrelva, Qulipta) all posted double-digit growth rates. Oncology remained stable, with Venclexta growing slightly while Imbruvica continued to decline. Aesthetics, on the other hand, faced pressure, with sales down slightly due to cooling demand in mature markets, particularly for Botox Cosmetic.

However, the operational side of the results showed a less positive picture. GAAP EPS fell to just $0.10 due to high costs for acquired intellectual property rights and a milestone payment of $1.50 per share. Adjusted earnings were $1.86, down 38 percent from last year. GAAP operating margin fell to 12.1 percent, while on an adjusted basis the company achieved 30.9 percent. R&D expenses rose to nearly 15 percent of sales, and IPR&D expenses were up to 17 percent of sales. However, the high cost base is due to intensive investments in pipeline to boost growth profile over the next decade.

The full earnings presentation can be found here.

Management commentary

CEO Robert A. Michael highlighted that AbbVie once again has a very strong growth profile, driven by the success of replacement immunology therapies and expansion in other strategic areas, particularly neuroscience and migraine. He said the company is at a key stage where it is both monetising its existing portfolio and investing sharply in next-generation medicines. Meanwhile, the dividend increase shows management's confidence in the company's financial strength. The CEO also commented on the continued progress in the development of Rinvoq for other indications and the potential for the treatment of alopecia areata, where he rates the latest data as breakthrough.

Outlook

The company raised its full-year target range for adjusted EPS to $10.61-$10.65, despite significant cost pressures and continued pipeline investments. However, for GAAP earnings, the company expects lower numbers due to one-time R&D expenses. AbbVie also announced a 5.5 percent dividend increase starting in 2026, continuing its long-term policy of steady payout growth. Management expects strong growth rates for both Skyrizi and Rinvoq in 2026, along with a gradual recovery in aesthetics and stabilization in oncology.

Long-term results

Looking at long-term results, we see significant fluctuations due to the emergence of Humira biosimilars, portfolio transformation, and a jump in research investment. The company's 2024 revenue was $56.33 billion, a slight year-over-year increase. However, in 2023, revenues fell by more than six per cent due to the sharp decline of Humira in the US. In contrast, the company reached over $58 billion in 2022, while 2021 was similarly strong with $56 billion.

Gross margins improved significantly again after the pressure of 2022-2023. In 2024, it climbed to over $39 billion in gross profit, up 16 percent year-over-year, reflecting the portfolio's shift toward advanced, high-margin therapies. By contrast, 2023 was a weak year, with gross profit falling sharply while older products fell.

Operating expenses rose significantly in 2024, by more than 43 percent to more than $30 billion. This jump is the result of massive investments in development, clinical trials and pipeline expansion. As recently as 2022 and 2021, operating costs were significantly lower, around $20 billion.

As a result, operating profit fell to $9.1 billion in 2024, compared to $12.8 billion in 2023 and even over $18 billion in 2022. Net profit fell to $4.28 billion in 2024, down from nearly $12 billion two years earlier. EPS followed a similar trend, falling to $2.4 in 2024, down from over $6.6 in 2022.

The EBITDA trend shows the transformation of the entire company - while it was over $31 billion in 2022, it plummeted to $17.3 billion in 2023 and further declined to $14.9 billion in 2024. This trend is clearly linked to heavy investment in research and portfolio transformation.

News

- The FDA approved the expansion of Rinvoq's indication for ulcerative colitis and Crohn's disease in patients for whom the deployment of anti-TNF therapy is not appropriate.

- Rinvoq succeeded in a second pivotal Phase 3 study for the treatment of alopecia areata, with up to 55% of patients achieving 80% hair coverage within 24 weeks.

- Studies have also shown significant improvements in eyebrow and eyelash growth, strengthening the molecule's position in dermatology.

- Management also highlighted advancing pipelines in oncology, migraine and neuroscience.

Shareholders

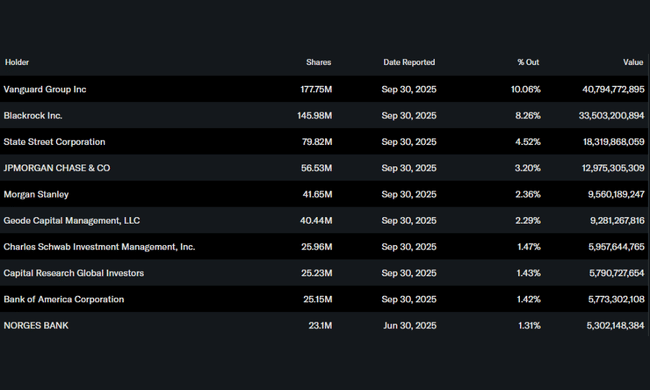

AbbVie has a stable, predominantly institutional ownership base. The institution holds approximately 75 percent of the free float, while insiders own less than 0.1 percent. The largest shareholders include Vanguard Group with more than 177 million shares, BlackRock with just under 146 million shares and State Street with nearly 80 million shares. The fourth-largest investor is JPMorgan with more than 56 million shares. The structure shows that the firm is firmly anchored in the portfolios of large asset managers managing long-term capital.

Analysts' expectations

Analysts expect 2026 to bring a re-acceleration in growth, mainly due to Skyriz and Rinvoq further replacing Humira. Revenue growth, margin stabilisation and a return to higher EBITDA are expected once the cost burden associated with the expanded pipeline subsides. The median target price has increased slightly in recent weeks and analysts continue to view AbbVie as one of the most stable dividend players in the pharmaceutical sector.