AMD enters the second half of the year with momentum that goes far beyond a routine rebound. The company has turned uncertainty around export restrictions into an opportunity to strengthen its standing in the global semiconductor hierarchy. The latest quarter confirms that AMD can translate AI‐driven compute demand into tangible financial performance, posting strong top-line expansion and improving margins — all while Chinese GPU sales remain largely absent.

What is becoming increasingly clear is that AMD is no longer defined by a single product line or competitive rivalry. Instead, it is assembling a multilayered compute ecosystem that spans data-center accelerators, hyperscaler partnerships, high-end PCs and embedded architectures. This diversification gives AMD multiple engines of growth, even as it commits to heavy investment cycles in AI infrastructure and next-generation development.

How was the last quarter?

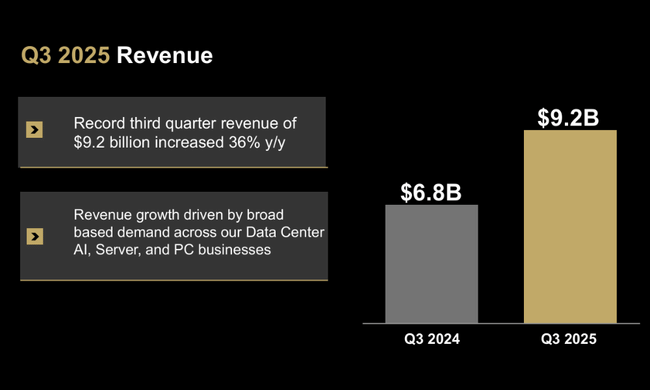

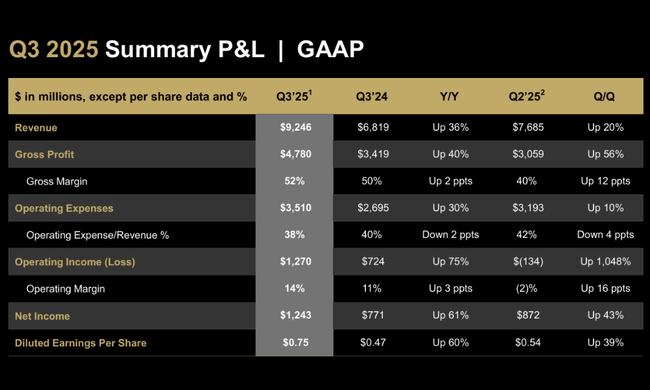

Q3 2025 was a recordquarter for $AMD in terms of both revenue and profitability. Revenues reached $9.25 billion, up 36% year-over-year and a solid sequential growth rate of 20%. Driven primarily by EPYC datacenter processors and Instinct AI accelerators, but also by the client and gaming business, which is returning to growth mode after a weaker period. Importantly, the company was also able to significantly improve margins - GAAP gross margin rose to 52%, while non-GAAP gross margin held at a very comfortable 54%.

At the earnings level, you can see how quickly AMD's results stabilized after the "export control" intervention in the second quarter. GAAP operating profit jumped to $1.27 billion, non-GAAP operating profit to $2.24 billion. GAAP net income of $1.24 billion and non-GAAP net income of $1.97 billion represent tens of percent year-over-year growth, with adjusted earnings per share of $1.20 up roughly a third from last year. The contrast to the second quarter, where inventory and related costs associated with the US restrictions on MI308 GPUs were still showing up, is also impressive - now the company is showing not only revenue growth, but a return to standard profitability levels.

A look at the segments shows a clear dominance of datacenter and a very dynamic turnaround in the client and gaming business. The datacenter segment earned $4.3 billion, up 22% from a year ago, and benefited from strong demand for fifth-generation EPYC processors as well as MI350 accelerators in AI clusters. The client and gaming segment brought in $4 billion, up a dramatic 73% y/y. Of that, the client business generated $2.8 billion (+46% y/y) thanks to record Ryzen sales and a richer product mix, while gaming surged to $1.3 billion (+181% y/y) thanks to higher sales from semi-custom console chips and demand for Radeon GPUs. The only weaker part is the embedded segment with sales of $857m (down 8%), where demand is still normalising after the previous boom.

Interesting detail: the third quarter results do not include any revenue from MI308 GPU shipments to China. Still, AMD managed to achieve record numbers, which acts as an important signal to investors - the business is less dependent on sensitive markets and export restrictions are not fatal to the company's growth momentum. At the same time, the product mix appears to be shifting towards higher-margin and more capital-intensive AI solutions, which will increase sensitivity to datacenter investment cycles in the years ahead.

CEO commentary

Lisa Su comments on the results unequivocally: AMD is entering a new phase of growth driven by the "expanding compute franchise" and the rapidly growing datacenter AI business. She emphasizes that this is not only a y/y jump in revenue, but also a qualitative change - EPYC processors and Instinct accelerators are becoming a solid part of large hyperscale and enterprise platforms, not just an "alternative" to the dominant players. Combined with a record quarter and strong Q4 outlook, management is talking about a "clear shift" in growth trajectory.

At the same time, it points out that AMD is not just putting wind in the sails of a single product or GPU generation. The portfolio is expanding across the board - from server CPUs, to AI accelerators and Helios, to high-end desktop and HEDT Ryzen Threadripper 9000 processors for makers and pros. CFO Jean Hu adds that the company is generating record free cash flow despite investing aggressively in AI and high-performance computing. That's a combination that gives management room for both further investment and long-term shareholder value creation.

Outlook

The outlook for Q4 2025 confirms that AMD is not counting on "breathing room." The company expects revenue of around $9.6 billion, plus or minus $300 million. The midpoint of the outlook implies about 25% year-over-year revenue growth and about 4% sequential growth. Non-GAAP gross margin should be around 54.5%, slightly above third-quarter levels. AMD also notes that even the Q4 outlook does not include MI308 GPU revenue for China, which again underscores that the key growth scenario is based primarily on the US, Europe and other "safe" markets.

In the medium term, the datacenter and AI business is expected to be the main driver. Partnerships with OpenAI, Oracle, DOE, large cloud providers and enterprise customers show that AMD is systematically reserving slots in future AI infrastructure. Planned deployments of tens of thousands of GPUs in Oracle AI superclusters, multi-gigawatt deployments for OpenAI, or AI supercomputers for the US Department of Energy give the company visibility of orders through 2026 and beyond. From an investor perspective, it is important that these are not one-off contracts, but long-term projects in several waves.

Long-term results

The history of the last four years shows AMD as a company that can grow in waves, but is also very sensitive to investment and product cycles. Revenues have moved from roughly $16.4 billion in 2021 to $25.8 billion in 2024, which corresponds to very solid double-digit annual growth. After a sharp jump in 2022, there was a slight revenue correction in 2023, but AMD was able to overcome this in 2024 and build on the next growth phase. It can be seen that the expanding datacenter business can offset the fluctuations in the PC and gaming segment.

Profitability has been much more volatile in recent years. Gross profit has been above $10 billion for a long time and has been rising gradually, but operating profit has undergone visible fluctuations - AMD generated an operating profit of over $3.6 billion in 2021, only $1.26 billion in 2022, and stagnated at a relatively low level of around $400 million in 2023. Only 2024 brought a more significant turnaround, with operating profit climbing to $1.9 billion, almost four times the 2023 level. This development illustrates well how challenging the transition from "classic" PC and gaming cycles to the capital- and technology-intensive AI and datacenter world has been.

Net income shows a similar story. AMD's record year in 2021, when it earned over $3.1 billion and EPS exceeded $2.5, was followed by a gradual decline, with net profit falling to about $1.3 billion in 2022 and even lower to $854 million in 2023 before returning to growth in 2024, reaching $1.64 billion. Earnings per share followed a similar pattern, hovering around $1 in 2024. So the long-term trend shows that AMD has the ability to monetize technology leadership quickly, but also bears the risk of steeper profit declines when it is just flipping its portfolio or going through costly new product generation phases.

From an investor perspective, the upside is that despite these fluctuations, AMD maintains decent cost control. While operating costs have risen over the years - from roughly $4.3 billion in 2021 to more than $10.8 billion in 2024 - their growth primarily reflects the expansion of research, development, and marketing for next-generation GPUs, CPUs, and accelerators.

News

Recent months have brought a flood of strategic announcements at AMD that illustrate very well why management is talking about an "AI factory" and a new phase of growth. A key milestone is Strategic partnership with OpenAIunder which AMD is to deliver up to 6 gigawatts of GPU power for the next generation of AI infrastructure. The first gigawatt, in the form of the Instinct MI450, is scheduled to be deployed in the second half of 2026, a long-term contract that firmly anchors AMD at the very center of the generative AI ecosystem.

Equally important is the shift in the cloud. Oracle Cloud Infrastructure plans to be the first to offer a public AI supercluster based on the "Helios" rack design with MI450 GPUs, EPYC "Venice" CPUs and Pensando networking, with an initial deployment of 50k GPUs starting in Q3 2026. Alongside this, other large AI clusters are emerging - such as the Lux AI and Discovery supercomputer project for the US Department of Energy, or large deployments of MI355X in Cisco and G42 clusters in the UAE. These projects are emerging in parallel with the expansion of cloud partners such as AWS, Oracle, IBM and DigitalOcean, which are expanding their offerings of instances based on EPYC processors and Instinct GPUs.

On the "classic" product side, AMD is not slacking off in the PC and workstation space either. The new Ryzen Threadripper 9000WX and PRO 9000X deliver extreme multi-core performance for makers and professionals and are designed to strengthen AMD's position in the most powerful part of the desktop and workstation market. The gaming segment is supported by FSR 4 technology, which extends support across dozens of games and helps lift framerate and visual quality without the need for massive investment in new hardware. The embedded business, in turn, benefits from the portfolio expansion with EPYC Embedded 4005 and Ryzen Embedded 9000, which target industrial, edge and security applications with an emphasis on performance per watt and long life cycles.

Shareholding structure

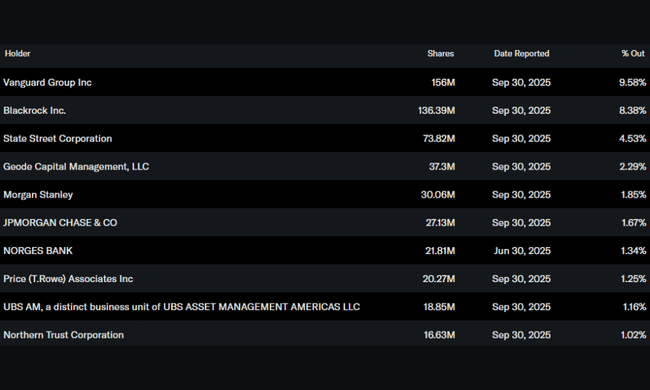

AMD's ownership structure matches the profile of a mature technology blue chip company. Within the company, only about 0.45% of the shares are held by insiders, so decision-making is not controlled by a single dominant founder or a narrow group of managers. The rest of the free float is clearly in the hands of institutional investors - who hold around 70% of the stock, signaling the strong confidence of large funds and index players in AMD's long-term story.

Major shareholders include Vanguard with roughly 9.6%, BlackRock with over 8% and State Street with over 4.5%. They are complemented by Geode Capital and other large asset managers.

Don't overlook: AMD and OpenAI partnership could shake up chip market

Analysts' expectations

The market views AMD's current results primarily through the prism of the AI supercycle. After a record third quarter and an ambitious Q4 outlook, analysts generally expect the datacenter and AI business to remain the main driver of double-digit revenue growth in 2026. The combination of strong growth in servers, gradual monetization of large AI contracts, and a return to normalcy after export constraints creates room for further profitability expansion - especially if gross margins can be maintained around current levels and pricing discipline is not lost.

At the same time, however, the consensus is that AMD is no longer a "cheap bet" on AI. Valuation is well above the long-term average for the semiconductor sector, and the stock price incorporates much of the optimism about future AI contracts, the ROCm ecosystem, and the ability to compete with established players in GPUs. As such, analyst commentary often focuses on the sensitivity of the story to a potential slowdown in AI infrastructure investment, the evolution of export constraints, and whether AMD can maintain the pace of innovation for MI4xx generations and beyond. For investors, this means that AMD remains an attractive growth story - but also a story that may be much more volatile in the future than traditional "defensive" technology titles.