Qualcomm closed 2025 with one of the most complex narratives in its recent history. On one side stands a record-breaking performance of the QCT division, powered by a rebound in flagship mobile demand, accelerating automotive wins and a rapidly expanding footprint in edge AI. On the other stands a sharp GAAP profit distortion caused by the latest U.S. tax rules—a one-time shock that rattled headline numbers without reflecting any real weakness in operations.

Looking past that accounting noise, the company’s trajectory is unmistakably shifting. Qualcomm is stepping out of the long shadow of smartphones and leaning into a diversified compute portfolio that spans connected vehicles, industrial automation, IoT devices and early forays into AI-centric data infrastructure. Q4 2025 marks not an end, but a beginning—the first tangible chapter in Qualcomm’s move toward becoming a broad-based provider of intelligent computing systems.

How was the last quarter?

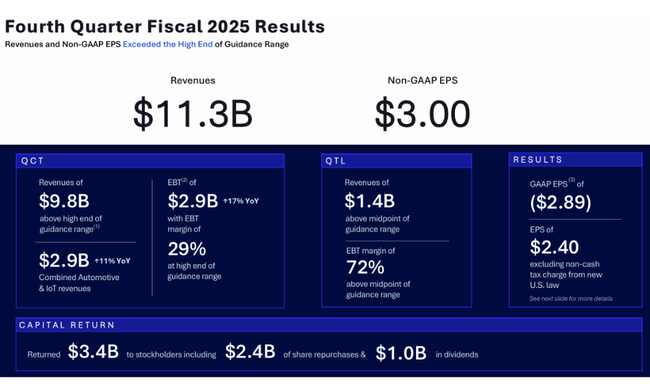

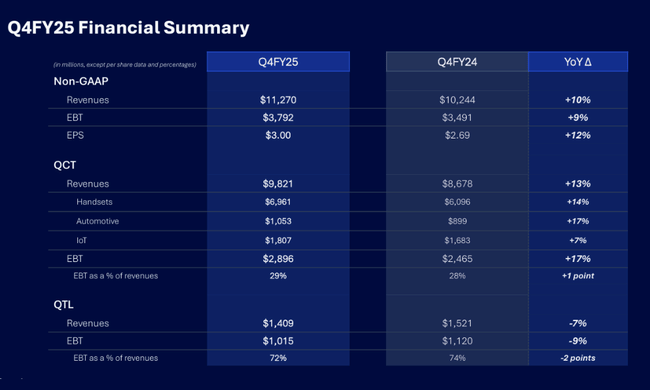

In terms of revenue and operational metrics, Qualcomm $QCOM delivered one of the strongest numbers in recent years. Revenue grew 10% year-over-year to $11.27 billion, with by far the biggest contributor coming from the QCT. Its revenue was up 13%, driven by improving demand in high-end phones, a fast-growing automotive business and solid IoT performance. Gross margin remained stable at 52%, confirming Qualcomm's ability to monetize the increased technological complexity of its platforms.

However, GAAP financial performance was significantly impacted by the new U.S. tax legislation, which forced the company to establish an accounting provision of $5.7 billion. This provision has no impact on cash flow, however, it caused a reported GAAP net loss of USD -3.1 billion. Meanwhile, non-GAAP results tell a very different story - adjusted earnings grew 7%, non-GAAP EPS reached $3.00, and operating profit excluding non-recurring items grew at double-digit rates in most segments.

Handsets were up 14% year-over-year, a significant improvement after a prolonged stagnation. Automotive added 17%, and in particular its annual momentum confirms its transition into a strategically key segment. IoT, up 7%, completes the mosaic of steady, broad-based growth across QCT. QTL's licensing division is down 7% but maintains extremely high margins, making it a stable source of free cash flow even in less favourable periods.

Overall, the fourth quarter confirmed that Qualcomm is entering a new phase of the technology cycle where it no longer relies on a single growth engine, but builds performance on multiple segment pillars with high resilience to market cyclicality.

CEO commentary

CEO Cristiano Amon Rates 2025 as a breakthrough year:

Record QCT results confirm that Qualcomm stands on a much broader foundation today than ever before. Automotive and IoT are growing double digits, demand for our AI platforms is accelerating, and we are entering segments that will form the computing backbone of the next decade.

Amon also highlighted that Qualcomm has a fully integrated technology stack for autonomous driving, opening the door to a fast-growing market that until now has been dominated by Nvidia. The company also hinted at further steps toward energy-efficient computing solutions for data centers - an area where it can offer an alternative to the GPU-centric model thanks to low power consumption and architectural optimizations.

Outlook

For the first quarter of fiscal year 2026, Qualcomm expects:

- Revenue of $11.8-12.6 billion

- QCT $10.3-10.9 billion

- Non-GAAP EPS of USD 3.30-3.50

The outlook is based on four stable trends:

- Return to premium smartphones

- accurately predictable automotive growth thanks to extensive design wins

- Strengthening positions in edge AI and industrial systems

- normalisation of the licensing business

The firm also communicated that it now expects an effective tax rate of around 13-14%, which is crucial for predictability of results.

Long-term results

Qualcomm's long-term results show a company that has been able to restart growth and return to strong profitability after the covid boom and subsequent semiconductor market correction. Revenues in 2025 reached $44.3 billion, returning to the record levels of 2022. It is also the second consecutive year of double-digit revenue growth, despite structural changes in the mobile market. The development confirmed that QCT's key segments - mobile chipsets, automotive and IoT - are starting to generate more stable and diversified revenue than in the past, when Qualcomm depended primarily on a cyclical smartphone economy.

Gross margins have been able to stay high during this growth thanks to a better product mix and higher demand for premium platforms. While manufacturing costs grew at a faster pace than sales, the company still maintained gross profit above $24.5 billion, a near return to pre-correction levels in 2022. However, the structure of operating profitability changed significantly: while the company struggled with revenue declines and cost growth spikes in 2023, 2024 and 2025 brought a clear turnaround. Operating expenses grew only modestly and operating profit jumped more than 22 percent to $12.35 billion, nearly double the 2023 figure.

The picture is also remarkable in terms of operating metrics. Both EBIT and EBITDA have grown at double-digit rates for two consecutive years, showing that Qualcomm can scale its new growth cycle more efficiently. EBITDA of $14.9 billion in 2025 is still below 2022 levels, but the gap is closing rapidly and the pace of recovery shows that the margin pressure from 2022-2023 is gradually fading. In addition, the company has been consistently reducing share count through buybacks, which is boosting per-share metrics - while 2025 GAAP EPS has fallen sharply, this decline is primarily driven by a single accounting item.

This is because 2025 net income is significantly impacted by an extraordinary tax burden that distorts year-over-year comparisons. While before the tax legislation intervention the net profit trend would have continued to grow, the resulting figures show a 45 percent drop. Adjusted for the tax effect, however, Qualcomm's long-term trajectory remains positive: the company has stabilized after the turbulent years of 2022-2023, has resumed growth in all key segments, and is once again approaching its historical performance. Thus, it is more important for investors to track the structural strength of the results than the optical decline in net income, which does not fundamentally reflect the reality of the development.

News

The year 2025 brought several key milestones:

- Automotive: launch of a complete platform Snapdragon Ride Flex and the first commercial implementation of a fully integrated driving stack.

- AI & Edge: Expansion of AI architectures into robotics, industrial automation and edge systems.

- Data Centers: Qualcomm outlined directions for further expansion - low-power inference, specialized accelerators, and collaboration with partners in autonomic systems.

- Capital Discipline: US$12.6 billion returned to shareholders during the year in dividends and buybacks.

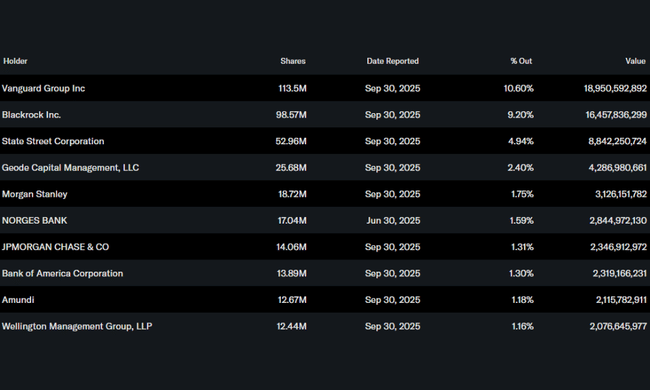

Shareholder structure

Dominance of institutional investors provides stability:

- Institutions hold 81.82% of shares

- Largest positions:

- Vanguard - 10,60 %,

- BlackRock - 9,20 %,

- State Street - 4,94 %,

- Geode - 2,40 %.

Analysts' expectations

According to the latest analysis Morgan Stanley analysts affirm rating Overweight and target price 210 USD. The report highlights three strategic pillars: an expanding automotive market, stabilizing licensing, and significant potential in edge AI.