Devon Energy delivered a far stronger third quarter than the market anticipated, stepping into a period of commodity volatility with performance that outpaced nearly all of its U.S. shale peers. Production climbed to the top end of guidance, supported by efficient development in the Delaware Basin and an aggressive focus on lowering well costs. Instead of the cautious, defensive quarter analysts expected, Devon posted results that signal a company regaining momentum at the operational core of its portfolio.

Even more notable is the company’s improving capital discipline. With spending coming in well below plan and operating costs trending lower for a third consecutive quarter, Devon generated substantial free cash flow that strengthened the balance sheet and enabled continued shareholder returns. In an environment where many producers struggle to balance reinvestment with cash generation, Devon is positioning itself as one of the most operationally consistent and financially resilient operators in the Permian.

How was the last quarter?

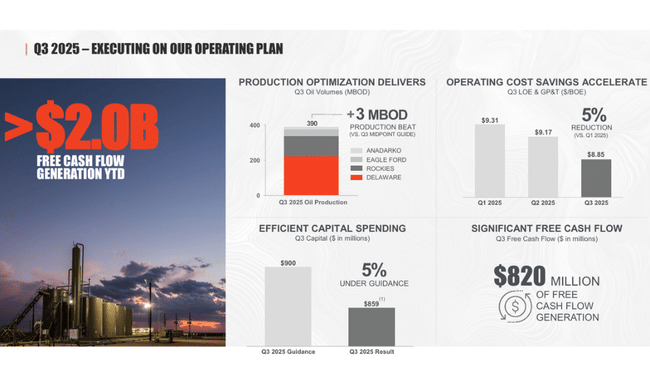

Devon Energy $DVN delivered results in Q3 2025 that exceeded its own expectations in almost all key parameters. Production reached 853,000 barrels of oil equivalent per day, breaking the upper guidance limit, and oil production itself climbed to 390,000 barrels per day. This shift was not the result of a one-time effect, but a combination of improved performance in multiple regions, particularly in the Rockies and Eagle Ford, where new drilling exceeded expectations and increased overall production efficiency.

Financial results were also strong. Revenues from oil, gas and NGL sales were $2.8 billion, with improved oil price realization able to partially offset weaker gas prices. Operating cash flow increased to $1.7 billion, representing a nine percent increase over the previous quarter. But even more significant was the growth in free cash flow, which climbed to $820 million. This is one of the most important metrics for investors, as it determines the company's ability to pay dividends, make buybacks and reduce debt.

In addition, Devon was able to maintain capital expenditures at $859 million, about five percent less than planned. This result is a testament to more efficient cost management, better service acquisition pricing and optimized drilling cycles. At the same time, the company was able to reduce unit costs of production, with total operating expenses falling to $11.41 per barrel of oil equivalent. Lease operating expenses along with transportation and processing costs were $8.85 per BOE, three percent below the company's estimates.

At the earnings level, the company reported net income of $687 million ($1.09 per share), while core, adjusted earnings were $656 million. The stability of the results is supported by balance sheet strength - Devon holds $1.3 billion in cash, has no revolving credit facility, and has reduced its net debt to EBITDAX ratio to a very conservative 0.9x through continued deleveraging.

CEO commentary

Clay Gaspar Called the third quarter "the best this year", not only due to strong production or lower costs, but also due to noticeable progress on the corporate program Business Optimization. The program is expected to deliver $1 billion in cumulative savings by 2026, and more than 60 percent of the goal has already been met. Gaspar emphasized that the next phase of optimization will build on digitizing processes, deploying advanced data analytics and faster operational decision-making.

The CEO also pointed to the fact that thanks to high capital discipline and technological innovation, the company has been able to increase production without the need for dramatic cost increases. Going forward, he expects steady production and a decline in capital in 2026, a unique position compared to the competition in the Permian, where many producers are reporting rising CAPEX due to mining inflation.

Outlook

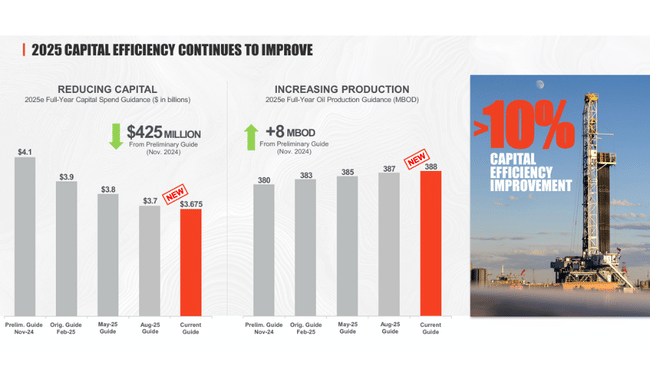

Devon expects fourth quarter production between 828-844k BOE/d, with oil production expected to be 383-388k barrels. This represents a slight reduction from Q3, but still at a very robust level consistent with a long-term strategy of stable production without excessive CAPEX increases.

Capex will be between $890-950 million, reflecting higher drilling activity before year-end. For 2026, the company projects CAPEX in the range of $3.5-3.7 billion, roughly $100 million lower than 2025, while maintaining production in the range of around 835-855 thousand BOE per day. This outlook is particularly attractive to return-oriented investors as it implies higher future free cash flow.

Long-term results

Looking at the last four years, there are significant cyclical swings characteristic of the oil and gas sector, but also stabilizing elements that Devon has gradually built up. Revenues have stalled at $15.6 billion in 2024, a modest 2.8 percent growth after the significant 2023 decline caused by weaker commodity prices. Thus, in contrast to an extremely strong 2022, Devon has gradually found a balance between production, price and cost structure.

More significant changes can be seen in the cost base. Production costs in 2024 reached $11.3 billion, up 13.6 percent from the previous year. However, the growth partly reflects higher activity, changes in the drilling portfolio and higher service inflation at Permian. Gross profit fell to $4.27 billion, a 20 percent decline. The decline in operating margin is noticeable - operating profit of $3.77 billion is more than 21 per cent lower than in 2023.

Looking even further out, however, to 2021-2022, the huge volatility caused by geopolitical shocks and the rise in oil prices following the Russian invasion stands out. 2022 was an extremely strong year, so it is logical that the 2023 and 2024 results look weaker. However, the company was able to remain profitable despite lower sales, thanks to efficient capital management and a conservative approach to debt.

Devon shows a significant decline in net profit to $2.89 billion in 2024, a nearly 23 percent drop from 2023. However, comparing the results to the period prior to 2022 shows that the firm's overall profitability has improved over the long term, and the current level of results represents a new stable base that the firm is looking to continue to build on through cost optimization and maintaining production volumes.

News

- Achieving 60% of the one billion dollar Business Optimization target

- Closing the acquisition of the remaining interests in Cotton Draw Midstream

-Strengthened position in Permian through the purchase of 60 net locations

- Continued share-buyback program, 13% of all shares repurchased to date

Shareholding structure

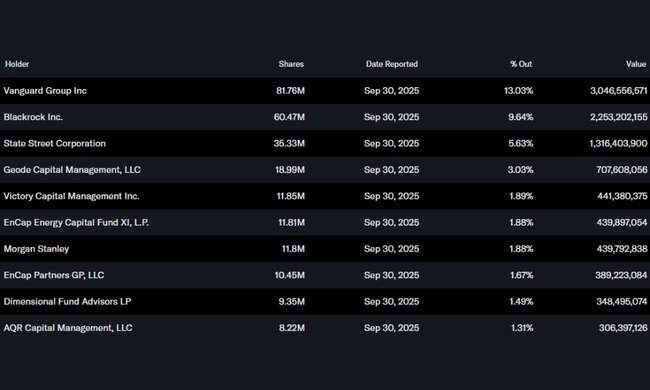

Devon Energy's ownership structure fits the profile of a large US mining company and clearly shows the dominance of institutional investors. They hold approximately 80 per cent of all freely traded shares, which is above the industry average. The largest shareholder is the Vanguard Group with more than 13 percent - a significant and long-term holding that is often seen as a stabilizing element. It is followed by BlackRock, State Street and Geode Capital, which together control another ten percent of the company.

Insider ownership remains low, around 0.8 percent, which is common in the energy sector. Thus, the shareholder structure indicates strong institutional support, high liquidity, and that any significant changes in sentiment by large funds can have a rapid impact on the share price.

Analysts' expectations

According to the latest analyst consensus published by MarketScreener and Reuters Estimates there is a positive sentiment towards Devon Energy. Analysts now expect steady free cash flow growth in 2026 due to a decline in CAPEX and stabilization of oil prices in the $75-85 range.

Specifically, analysts at JPMorgan (analyst Arun Jayaram) have affirmed the rating of Overweight with a price target of 67 USD, citing a combination of robust cash flow, continued deleveraging and the benefits of the optimization program. Jayaram highlights that Devon is emerging as one of the best managed producers within Permian in terms of capital discipline and ability to generate above-average margins even in an environment of pressure on gas prices.